Nvidia (NVDA) has had a parabolic rally over the last three years as it was the early winner from the artificial intelligence (AI) pivot, with its chips acting as the basic building block for the massive data centers that Big Tech companies are building. The stock has risen nearly sevenfold over the last three years. In terms of absolute dollar value, it has created more wealth for investors in that timeframe than any other company in history.

Nvidia’s rally shook up the Big Tech pecking order, and it not only pipped Apple (AAPL) to become the world’s most valuable company but became the first company to command a market cap of $4 trillion and subsequently $5 trillion. However, Nvidia has failed to decisively move past the $5 trillion market cap, a level it first hit in October 2025. The stock is up just 6.42% this year, which actually trails the Nasdaq Composite Index ($NASX). On the other hand, Alphabet (GOOG) (GOOGL) – which was the best-performing Magnificent 7 stock last year – has looked strong in 2026 also. The stock is up 22.44% for the year and commands a market cap of $4.66 trillion, which is a tad shy of Nvidia.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Nvidia Is Facing Competition from Amazon and Alphabet

While Nvidia remains the leader in the AI chip market, it faces significant competition, particularly from the very companies that are among its largest customers. For instance, Amazon’s (AMZN) Trainium chips have been selling like hot cakes, and the e-commerce giant has said that if its chip business were a standalone company, its annual revenues would be $50 billion.

While Alphabet hasn’t provided standalone numbers for its tensor processing unit (TPU) and graphics processing units (GPUs), during the Q1 2026 earnings call, it said that its chip order backlog is part of the $462 billion cloud backlog, which incidentally doubled in the quarter. CEO Sundar Pichai noted the “massive interest” in its GPUs and TPUs and said that it would “begin to deliver TPUs to a select group of customers in their own data centers.” It expects some revenues from these deals later this year, but the bulk of the revenues from the current deals will flow in 2027.

While hyperscalers have been touting their relationship with Nvidia, they have also been simultaneously working on custom chips. Along with using these chips, which invariably cost less than Nvidia's, companies like Alphabet and Amazon are increasingly looking to third-party customers.

Nvidia’s Growth Story Might Not Be Over Yet

Meanwhile, while Nvidia might not witness the kind of rally that it has seen over the last three years, the growth engine is far from over. Tech giants are doubling down on AI capex and will continue to spend on Nvidia chips alongside their custom in-house silicon.

Dependence upon hyperscalers has been a risk for Nvidia. The company has been looking to diversify its customer base to non-hyperscaler commercial users as well as governments building sovereign AI. During the fiscal Q4 2026 earnings call, the company highlighted the growth in sovereign AI and said that the business tripled to over $30 billion in the fiscal year.

The AI growth story looks far from over, and the total addressable market for chips is set to move higher as companies scale up their physical AI initiatives. For context, Nvidia generated $6 billion in revenue from physical AI in the last fiscal year, a number that looks set to move significantly higher over the coming years. Here again, while the likes of Tesla (TSLA) are working on their own chips, there would be a lot of room for Nvidia’s chips, too.

Resumption of exports to China could be another opportunity for Nvidia, but there is considerable uncertainty over its prospects in that country, which was once its second-biggest market after the U.S.

Should You Buy Nvidia Stock?

www.barchart.com

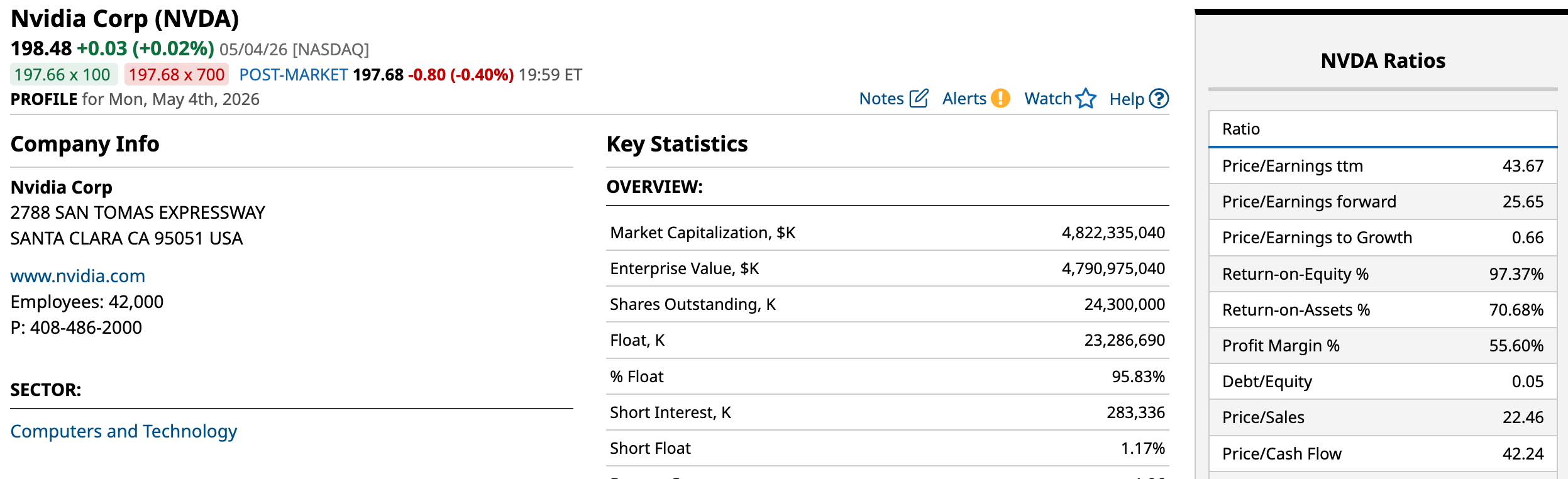

www.barchart.comNvidia trades at a forward price-to-earnings (P/E) multiple of 25.65 times, which I find reasonable despite concerns about the sustainability of its growth and fat margins beyond 2027. Overall, while Nvidia might no longer be the hot AI name it was, a laurel that seems to currently sit with Alphabet, the stock still has room to run higher, albeit not to the extent that we saw over the last three years.

www.barchart.com

www.barchart.com www.barchart.com

www.barchart.com On the date of publication, Mohit Oberoi had a position in: NVDA , TSLA , AMZN , GOOG . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Nvidia Stock’s Growth Story May Not Be Over Yet Expected Returns Investing In Amazon Are Not High - Shorting AMZN Puts Is a Better Play Reddit Stock Is an Earnings Season Winner. Investors Thank Advertising Revenue for That. DDOG Earnings Play Has a HUGE Return Potential