Pacific Biosciences of California PACB, popularly known as PacBio, is set to report first-quarter 2026 earnings on May 7. The Zacks Consensus Estimate for sales and loss per share is pegged at $41 million and 17 cents, respectively. Loss per share estimates for PACB have remained stable at 54 cents for 2026 and 48 cents for 2027 over the past 30 days.

PACB heads into its upcoming first-quarter 2026 earnings release on the back of a solid finish to 2025, marked by steady revenue growth and improving profitability metrics. Fourth-quarter performance was driven by record consumables revenue, strong placements of Revio and Vega systems, and expanding traction in clinical applications, particularly in rare disease genomics. Continued momentum in consumables, supported by higher system utilization and a growing installed base, remained a key highlight, while disciplined cost management contributed to notable gross margin expansion.

The key question for investors now is whether this momentum carried into the first quarter, especially as the company navigates a still-muted academic funding environment and ongoing macro uncertainties. Investors are also likely to closely watch early progress around the SPRQ-Nx chemistry rollout, trends in clinical adoption and consumables pull-through, and whether strength in EMEA and clinical end markets can offset persistent weakness in capital spending.

PacBio’s close peers, Illumina ILMN and 10x Genomics TXG, are slated to announce their quarterly numbers in the upcoming weeks. (Stay up to date with all quarterly releases: See Zacks Earnings Calendar.)

Earnings Surprise History

In the last reported quarter, PACB delivered an earnings surprise of 36.84%. Its earnings beat estimates in each of the trailing four quarters, delivering an average surprise of 27.67%.

In the last reported quarter, ILMN and TXG delivered an earnings surprise of 9.52% and 31.58%, respectively.

What the Zacks Model Unveils

Our proven model does not conclusively predict an earnings beat for PacBio this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. This is not the case here, as you will see below. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

PACB has an Earnings ESP of 0.00% and a Zacks Rank #3 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Key Factors Likely to Have Driven Q1 Performance

PacBio’s consumables business is expected to have remained the primary growth driver in first-quarter 2026, supported by rising utilization across its installed base of Revio and Vega systems and continued traction in clinical applications. Management highlighted record consumables performance and strong pull-through trends exiting 2025, driven by expanding adoption in clinical and hospital settings, particularly in rare disease genomics. This trend is likely to have been carried into the first quarter, though the constrained academic funding environment may have weighed on instrument demand.

Clinical adoption is likely to have been a key focus area in the quarter. The company previously pointed to robust growth in clinical consumables, supported by increasing use of HiFi sequencing in rare disease, oncology and targeted applications like PureTarget. Strength in EMEA, where customers are transitioning from pilot programs to broader clinical deployment, is expected to have supported performance. However, investors may closely monitor whether growth trends remain steady as initial adoption ramps normalize and macro uncertainties, including funding visibility and capital spending pressures, persist.

Pacific Biosciences of California, Inc. Price and EPS Surprise

Pacific Biosciences of California, Inc. price-eps-surprise | Pacific Biosciences of California, Inc. Quote

Segmental Performance Outlook

Consumables: PacBio’s consumables business is expected to have remained the largest contributor to revenue growth in first-quarter 2026, supported by higher utilization of Revio systems and an expanding installed base of both Revio and Vega platforms. Strong demand from clinical and hospital customers, particularly in rare disease and targeted sequencing applications, is likely to have contributed to first-quarter performance. Record consumables momentum exiting 2025, along with stable pull-through trends, is expected to have provided a solid base entering the quarter. However, investors will watch whether utilization trends remain consistent as early adoption benefits begin to normalize.

Instruments (Revio & Vega): Instrument revenue is expected to have seen mixed trends in the quarter. While Vega placements likely benefited from strong pipeline activity and faster sales cycles, Revio demand may have remained under pressure due to a muted academic funding environment, particularly in the Americas. The anticipated cost advantages of new chemistry offerings and continued clinical adoption could have supported placements. Investors will closely monitor order trends and any signs of recovery in capital spending.

Service and Other: Service and other revenue is expected to have grown steadily, supported by a larger installed base and increasing service contract adoption tied to Revio systems. As more systems move into active use, recurring service revenues are likely to have provided incremental stability to the overall revenue mix.

PACB’s Geographic Trends & End Markets

Regionally, strength in EMEA is expected to have continued, driven by accelerating clinical adoption as customers transition from pilot programs to broader deployment. Asia Pacific may have seen steady growth supported by clinical use cases, while the Americas likely remained subdued due to continued funding constraints among academic customers. Investors will watch whether growth in clinical end markets was sufficient to offset persistent weakness in academic and research-driven demand.

Price Performance

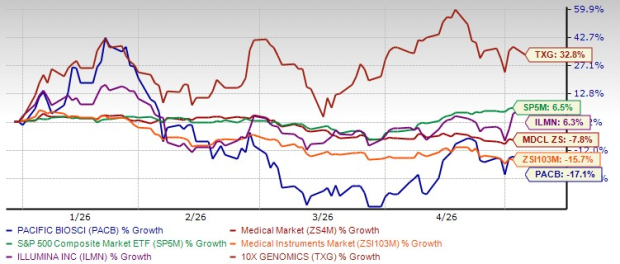

PACB’s shares have lost 17.1% so far this year compared with the industry’s 15.7% decline. The company’s shares have underperformed the S&P 500 Index’s gain of 6.5% and the Zacks Medical sector’s decrease of 7.8%.

PACB has underperformed ILMN’s and TXG’s year-to-date growth of 6.3% and 32.8%, respectively.

Image Source: Zacks Investment Research

Conclusion

PacBio has several encouraging factors supporting its longer-term growth story, including accelerating clinical adoption, strong consumables momentum and ongoing margin improvement efforts. However, with a Style Score of D, the stock reflects relatively weaker near-term characteristics. Whether the company can deliver an earnings beat in first-quarter 2026 remains uncertain, particularly given persistent headwinds from a muted academic funding environment and potential variability tied to early-stage adoption trends and product rollout timing.

While PacBio’s strategic focus on long-read sequencing, expanding clinical footprint and upcoming innovations like SPRQ-Nx position it well for future growth, near-term visibility remains somewhat limited. Existing investors may consider holding the stock, while new investors may prefer to wait for the first-quarter earnings results and updated management commentary before making fresh investment decisions.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Illumina, Inc. (ILMN): Free Stock Analysis Report

Pacific Biosciences of California, Inc. (PACB): Free Stock Analysis Report

10x Genomics (TXG): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).