DuPont de Nemours, Inc. DD reported adjusted earnings of 55 cents per share for the first quarter of 2026, up 52.8% year over year. The figure topped the Zacks Consensus Estimate of 48 cents by 14.6%.

Net sales of $1,681 million were up 4.3% from the year-ago quarter and beat the consensus estimate of $1,664.9 million by 1%. Organic sales increased 2%, reflecting strength in healthcare and aerospace end markets.

Profitability strengthened meaningfully in the reported quarter through organic growth, favorable mix, productivity gains and lower interest expense. DuPont’s materials and solutions portfolio benefited from execution gains, even as certain end markets remained uneven during the quarter.

DuPont de Nemours, Inc. Price, Consensus and EPS Surprise

DuPont de Nemours, Inc. price-consensus-eps-surprise-chart | DuPont de Nemours, Inc. Quote

DD’s Segment Highlights

Healthcare & Water Technologies posted net sales of $806 million, up 6% year over year, reflecting 3% organic growth and a 3% currency benefit. Within the segment, Healthcare Technologies delivered high-single-digit organic growth on broad-based demand led by medical packaging and biopharma, while Water Technologies declined in low to mid-single digits organically as strength in industrial water and microelectronics markets was more than offset by Middle East logistics disruptions.

Diversified Industrials generated net sales of $875 million, up 3% year over year, driven by a 3% currency tailwind, while organic sales were about flat. Building Technologies was down low single digits organically due to continued weakness in construction markets, while Industrial Technologies rose low-single digits organically on strength in aerospace and automotive, partly offset by declines in printing and packaging.

DD’s Financials

DuPont ended the quarter with cash and cash equivalents of $710 million. The balance sheet reflected long-term debt of $3,132 million, providing a snapshot of the company’s capital structure following recent portfolio actions.

Cash provided by operating activities from continuing operations was $232 million in the quarter, underscoring improved cash generation versus the year-ago period.

DuPont announced a $275 million accelerated share repurchase plan, reinforcing its emphasis on capital deployment alongside operational execution.

DuPont’s Outlook

For the second quarter of 2026, DuPont expects net sales of about $1.8 billion and operating EBITDA of about $430 million. Adjusted earnings are projected at approximately 59 cents per share, with guidance assuming about 3% organic sales growth year over year and currency as a slight tailwind.

Management raised its full-year 2026 outlook following the first-quarter outperformance and the interest income benefit tied to the Aramids transaction. The company now expects net sales of $7.155-$7.215 billion, operating EBITDA of $1.730-$1.760 billion and adjusted earnings of $2.35-$2.40 per share for 2026.

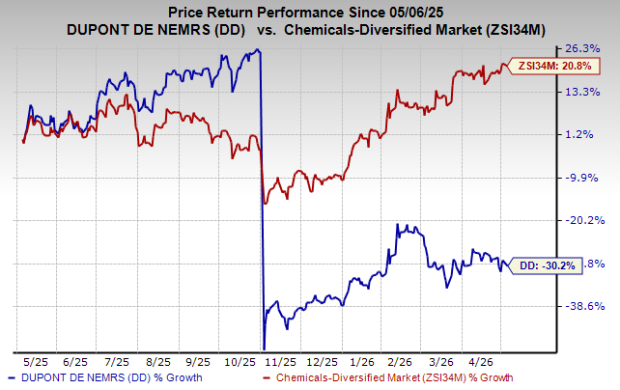

DD’s Price Performance

DuPont’s shares have lost 30.2% in a year against a 20.8% gain in the industry.

Image Source: Zacks Investment Research

DD’s Zacks Rank & Stocks to Consider

DD currently carries a Zacks Rank #3 (Hold).

Some better-ranked stocks in the basic materials space are CF Industries Holdings, Inc. CF, Compass Minerals International, Inc. CMP and Aris Mining Corporation ARIS.

CF Industries is slated to report first-quarter 2026 results on May 6. The Zacks Consensus Estimate for earnings is pegged at $2.35 per share, indicating 27.03% year-over-year growth. CF sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Compass Mineral is slated to report second-quarter fiscal 2026 results on May 6. The consensus estimate for CMP’s earnings per share is pegged at 66 cents. CMP presently carries a Zacks Rank #1.

Aris is scheduled to report first-quarter 2026 results on May 6. The Zacks Consensus Estimate for ARIS’s first-quarter earnings per share is pegged at 77 cents, indicating 381.25% year-over-year growth. ARIS carries a Zacks Rank #2 (Buy) at present.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

DuPont de Nemours, Inc. (DD): Free Stock Analysis Report

CF Industries Holdings, Inc. (CF): Free Stock Analysis Report

Compass Minerals International, Inc. (CMP): Free Stock Analysis Report

Aris Mining Corporation (ARIS): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).