With a market cap of $152.2 billion, ConocoPhillips (COP) is one of the world’s largest independent exploration and production (E&P) energy companies, headquartered in Houston, Texas. ConocoPhillips focuses primarily on upstream operations, exploring for, developing, and producing crude oil, natural gas, LNG, and bitumen globally. The company operates across major energy-producing regions, including the U.S., Canada, Norway, Qatar, Australia, and Malaysia.

Shares of the E&P titan have outperformed the broader market over the past 52 weeks. COP stock has risen 40.8% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 28.5%. Moreover, shares of the company are up 31.7% on a YTD basis, outpacing SPX's 6% gain.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Looking closer, shares of COP have lagged behind the State Street Energy Select Sector SPDR ETF's (XLE) 47.7% increase over the past 52 weeks and 33% rise in 2026.

www.barchart.com

www.barchart.com On Apr. 30, ConocoPhillips announced its FY2026 first-quarter results, and its shares dipped 1.9% as lower commodity prices and softer production weighed on profits. Sales and other operating revenues for the quarter totaled $15.76 billion, down 4.6% year over year, reflecting weaker realized commodity prices and reduced output. Average realized prices fell about 6% year over year to $50.36 per barrel of oil equivalent, primarily due to lower natural gas prices in the Permian Basin. On the bright side, its adjusted earnings came in at $2.32 billion, or $1.89 per share, comfortably ahead of Wall Street expectations of around $1.68 per share.

Shareholder returns remained a major highlight. ConocoPhillips returned nearly $2 billion to investors during the quarter through dividends and share repurchases and declared a second-quarter ordinary dividend of $0.84 per share.

For the fiscal year ending in December 2026, analysts expect ConocoPhillips' adjusted EPS to climb 54.2% year over year to $9.50. However, the company's earnings surprise history is mixed. It beat the consensus estimates in three of the last four quarters, while missing on one occasion.

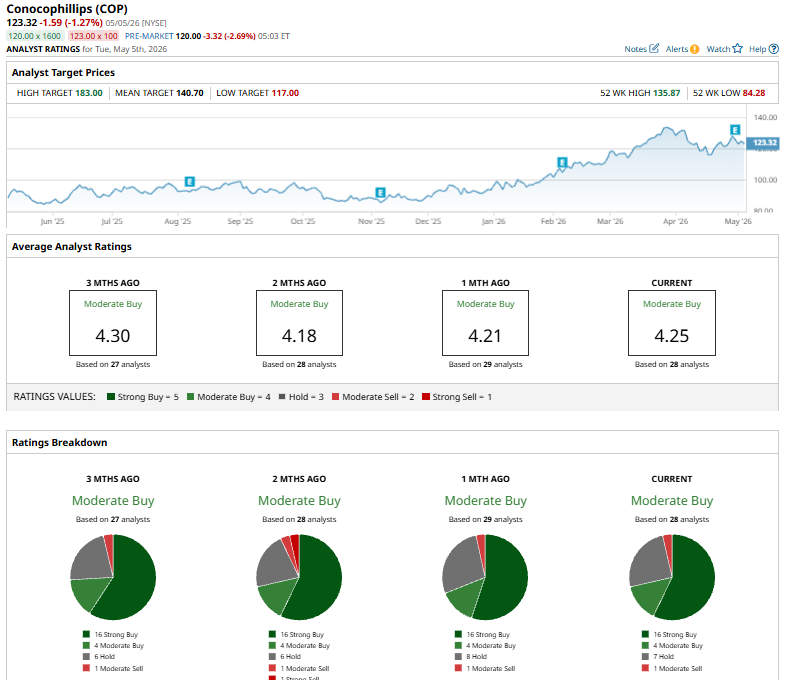

Among the 28 analysts covering the stock, the consensus rating is a “Moderate Buy.” That’s based on 16 “Strong Buy” ratings, four “Moderate Buy,” seven “Holds,” and one “Moderate Sell.”

www.barchart.com

www.barchart.com On May 1, Barclays analyst Betty Jiang reiterated an “Overweight” rating on ConocoPhillips and raised the firm’s price target to $136 from $128, signaling increased confidence in the energy giant’s earnings outlook and long-term growth potential.

The mean price target of $140.70 represents a 14.1% premium to COP’s current price levels. The Street-high price target of $183 suggests a 48.4% potential upside.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Positioning for a Big Move: SBUX Long Straddle Trade Idea Nasdaq Futures Rally on Upbeat AMD Earnings and U.S.-Iran Peace Deal Optimism As American Water Works Hikes Its Dividend, Consider Buying AWK Stock in May Pinterest Stock Skyrockets on Better-Than-Expected Earnings. Here's Why It's Not Too Late to Buy