Last week, SNDL Inc. SNDL reported mixed first-quarter 2026 results, with earnings meeting expectations but sales missing the mark.

The Canada-based cannabis company reported a loss of 3 cents per share, improving from a loss of 4 cents in the year-ago quarter. Sales declined more than 4% year over year to nearly $143 million (~C$196 million).

While quarterly results offer only a snapshot of performance, investors tend to focus more closely on broader business fundamentals and growth prospects. Let’s take a closer look at SNDL’s fundamentals to better understand how to approach the stock following its latest earnings report.

SNDL’s Cannabis Business Faces Mounting Pressure

SNDL operates through four reportable segments: Liquor Retail, Cannabis Retail, Cannabis Operations and Investments. Its cannabis business remains a key part of the company’s long-term strategy, spanning retail operations, branded products and vertically integrated manufacturing capabilities.

However, the company’s cannabis segment showed clear signs of weakness during the first quarter of 2026. Total cannabis revenues declined nearly 4% year over year, reflecting softer market demand across Canada. The pressure was particularly visible in Cannabis Operations revenue, which fell more than 14% year over year. Management attributed the decline to weaker market demand, destocking activity across retail channels and temporary timing issues related to business-to-business orders.

The weakness extended to retail trends as well. Although revenues from the Cannabis Retail unit remained essentially flat year over year despite the contribution from the newly added Cost Cannabis stores, same-store sales declined 2.5% during the quarter. Per management commentary, mature markets like Alberta and Ontario continue to face intense competition and market saturation, creating a challenging operating environment for cannabis retailers.

Profitability within the cannabis business also deteriorated. SNDL’s overall gross margin contracted 70 basis points year over year to 27%, primarily due to margin pressure within the Cannabis Operations segment. Lower production volumes, inventory adjustments and launch-related inefficiencies tied to the Jeeter ramp-up weighed on profitability during the quarter.

While SNDL continues expanding internationally and recently secured exclusive Canadian rights to the Jeeter brand, the latest quarter suggests the company is still grappling with slowing demand and persistent pricing pressure in Canada’s highly competitive cannabis market.

Stiff Competition in the Cannabis Space

SNDL competes in an overcrowded cannabis market against larger operators such as Aurora Cannabis ACB and Tilray Brands TLRY.

What further differentiates the competitive landscape is geographic diversification. Aurora has increasingly focused on higher-margin international medical cannabis markets, particularly in Europe, while Tilray continues expanding its global cannabis footprint alongside its U.S.-focused beverage and wellness exposure. This broader international presence provides additional growth avenues and reduces reliance on any single market.

In contrast, SNDL remains heavily dependent on Canada and has no direct U.S. cannabis operations. Although the company has been expanding international cannabis sales and partnerships, its business remains largely tied to the Canadian market, where pricing pressure, market saturation and intense retail competition continue to weigh on performance.

As competition intensifies and growth moderates across Canada’s cannabis industry, SNDL’s relatively limited geographic diversification may continue to pressure investor sentiment toward the stock.

SNDL Stock Performance & Valuation

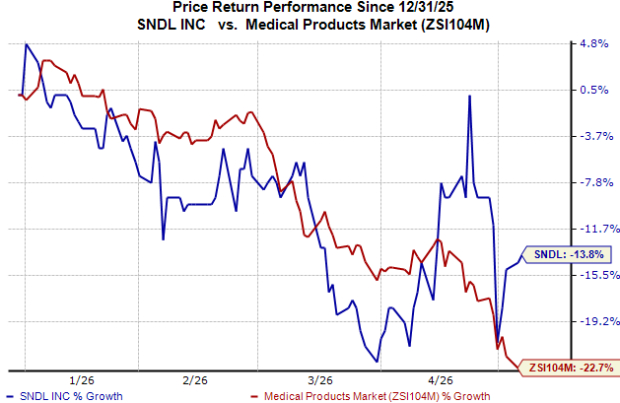

Shares of SNDL have lost 14% year to date compared to the industry’s 23% decline, as seen in the chart below.

Image Source: Zacks Investment Research

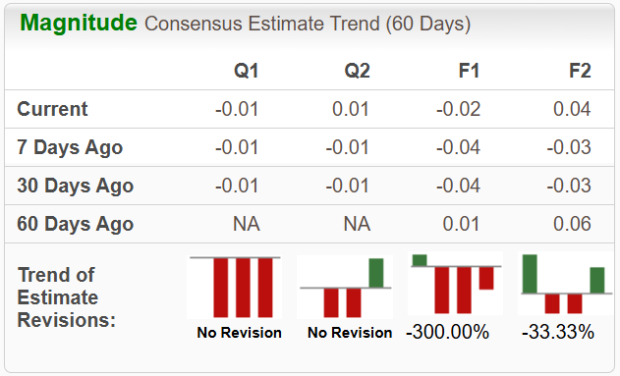

Bottom-line estimates for 2026 and 2027 have been mixed in the past 7 days.

Image Source: Zacks Investment Research

How to Play SNDL Stock?

While SNDL continues to maintain cost discipline and expand its international cannabis operations, its heavy exposure to the Canadian market remains a key overhang. Persistent pricing pressure and intense competition in an increasingly saturated cannabis market continue to weigh on margins and delay a return to consistent profitability. Although recent developments surrounding potential marijuana rescheduling in the United States have improved broader cannabis sector sentiment, SNDL’s limited direct exposure to this market may restrict its ability to benefit meaningfully relative to peers with established American operations.

Downward revisions in earnings estimates for the near term further reflect cautious analyst sentiment toward the stock. SNDL currently carries a Zacks Rank #5 (Strong Sell), suggesting limited upside potential and elevated risk for investors at present.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Tilray Brands, Inc. (TLRY): Free Stock Analysis Report

Aurora Cannabis Inc. (ACB): Free Stock Analysis Report

SNDL Inc. (SNDL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).