Shares of Radian Group Inc. RDN have gained 10.4% in the past year against the industry’s decline of 8.5%. With a capitalization of $4.99 billion, the average number of shares traded in the last three months was 1.4 million.

Image Source: Zacks Investment Research

RDN has underperformed a multiline insurer like CNO Financial Group, Inc. CNO, which has gained 18.3% in the past year, but outperformed others like MetLife, Inc. MET and Prudential Financial, Inc. PRU, which have lost 3.3% and 5.8%, respectively.

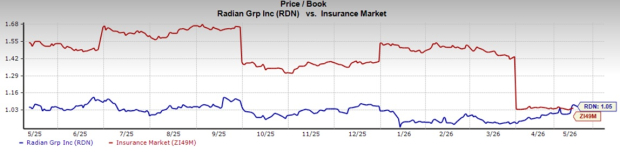

RDN Shares Are Affordable

RDN shares are trading at a price-to-book value of 1.05X, lower than the industry average of 2.57X, the Finance sector’s 4.39X, and the Zacks S&P 500 composite’s 7.1X. Its pricing, at a discount to the industry average, gives a better entry point for investors.

Image Source: Zacks Investment Research

Encouraging Projections for RDN

The Zacks Consensus Estimate for Radian Group’s 2026 revenues is pegged at $1.22 billion, implying a year-over-year improvement of 0.02%. The estimate for 2026 earnings per share (EPS) indicates a year-over-year increase of 17.5%.

The consensus estimate for 2027 EPS and revenues indicates an increase of 3.2% and 2.7%, respectively, from the corresponding 2026 estimates.

The expected long-term earnings growth is pegged at 7.7%.

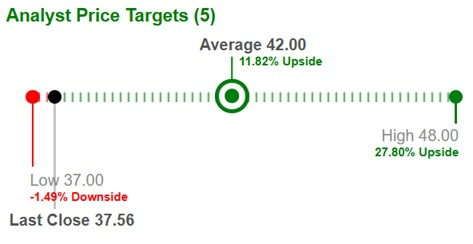

Average Target Price for RDN Suggests Upside

Based on short-term price targets offered by five analysts, the Zacks average price target is $42 per share. The average suggests a potential 11.8% upside from the last closing price.

Image Source: Zacks Investment Research

RDN’s Favorable Return on Capital

Return on invested capital in the trailing 12 months was 7%, better than the industry average of 2.1%, reflecting RDN’s efficiency in utilizing funds to generate income.

Key Points to Note for RDN

Radian Group’s mortgage insurance portfolio is expected to create a strong foundation for future earnings, supported by its proprietary analytics capabilities and RADAR Rates platform. However, persistence rates witnessed a modest decline due to higher refinancing activity.

Management expects in-force premium yields to remain steady, supported by favorable industry pricing conditions and a large share of low-interest-rate loans in force. In addition, RDN has been witnessing a declining pattern of claim filings. We expect paid claims to decline further, thus strengthening the balance sheet and improving its financial profile.

Radian Group completed its strategic acquisition of Inigo in February 2026. With this acquisition, Radian Group will expand from a leading U.S. private mortgage insurer into a global, diversified, multi-line specialty insurer, tremendously increasing its product expertise and capabilities while optimising the deployment of the excess capital.

Radian Group projects mid-teens percentage growth in EPS and approximately a 200-basis point increase in return on equity in the first full year after the transaction closes in early 2026. RDN expects the deal to double its total annual revenues, providing flexibility to deploy capital across multiple insurance lines through various business cycles.

Radian Group has also agreed to divest its Mortgage Conduit, Title and Real Estate Services businesses. With this divestiture, the insurer intends to simplify its operations and focus on the new insurance venture, a global multi-line specialty insurance business.

Radian Group maintains a solid balance sheet with sufficient liquidity and strong cash flows. A strong capital position helps Radian Group deploy capital via share repurchases and dividend hikes that enhance shareholders’ value.

Conclusion

Improving mortgage insurance portfolio, declining claims, a solid capital position and effective capital deployment should continue to favor mortgage insurers over the long term.

The company’s current dividend yield of 2.7% betters the industry average of 0.7%, making it an attractive pick for yield-seeking investors. Its solid growth projections as well as attractive valuations are other positives. Coupled with impressive dividend history and favorable ROIC, the time appears right for potential investors to bet on this Zacks Rank #2 (Buy) insurer. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

CNO Financial Group, Inc. (CNO): Free Stock Analysis Report

MetLife, Inc. (MET): Free Stock Analysis Report

Prudential Financial, Inc. (PRU): Free Stock Analysis Report

Radian Group Inc. (RDN): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).