Salesforce (CRM) just picked up a new $72 million contract from the U.S. Air Force, and on the surface, that sounds like good news for a company trying to prove that its AI push has real traction. But the stock market is still asking a bigger question: Is Salesforce becoming a better business, or is it simply getting cheaper while investors wait for growth to reaccelerate?

That is the tension around a lot of software names right now. Investors still like the AI story, but they have become more selective. They want real revenue, not just a good narrative. Investors want proof that enterprise software vendors can turn new tools into steady recurring sales.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Salesforce sits right in the middle of that debate. It is a giant in customer relationship software. It also wants to be seen as an AI platform company. The new Air Force deal helps that pitch, but it does not erase the questions hanging over CRM stock.

Why Has Salesforce's Stock Performance Been Weak?

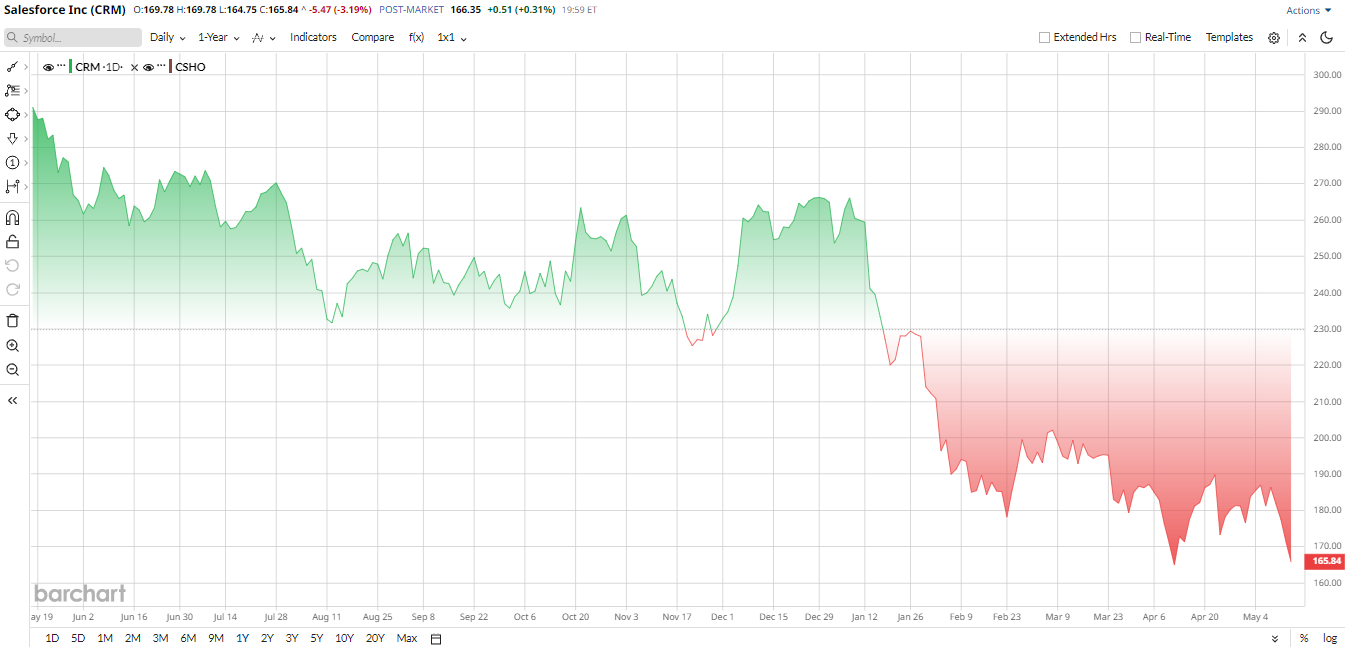

Salesforce has had a rough stretch. Shares are down 34% in 2026 and about 40% over the past 12 months. Shares are also sitting near the low end of the 52-week range.

A lot of that weakness comes from the market’s fear that AI could change the software world faster than investors expected. Salesforce is still growing, but some traders worry that adoption of its newer AI products will take time. Others have also focused on the slower pace of growth in the broader Software-as-a-Service (SaaS) space.

Even so, CRM stock has not fallen because the business is broken. It has fallen because expectations were high, and the market now wants more proof.

This is where the story gets more interesting. Salesforce does not look expensive on every measure. CRM stock trades at about 17 times forward earnings, which is below the roughly 21 times median for the tech sector. CRM stock also looks inexpensive in cash flow terms. Morgan Stanley said the shares trade at about 10 times free cash flow, versus about 24 times for large software peers. That is a big gap.

So, Salesforce is not a classic deep-value name, but it is also not priced like a hypergrowth story anymore. For a company with a huge installed base, strong cash generation and a growing AI layer, that matters.

www.barchart.com

www.barchart.com The U.S. Air Force Contract Is Good News, Not a Game-Changer

The new Air Force deal is real, and it adds another federal customer to Salesforce’s portfolio. The agreement is tied to Missionforce National Security, which includes AI tools designed to help modernize personnel and other functions.

That is useful for two reasons. First, it shows the company can still win large enterprise deals. Second, it gives Salesforce another example of AI being used in a practical setting, which is exactly what investors want to see right now.

Still, $72 million is tiny compared with Salesforce’s annual revenue base. CRM stock may like the symbolism, but the contract is not the kind of event that changes the earnings picture by itself. It supports the story, but does not define it.

Salesforce's Latest Quarter Was Strong

Salesforce’s fiscal fourth-quarter report was solid. Revenue came in at $11.2 billion, up 12% from a year earlier. Subscription and support revenue reached $10.7 billion, up 13% year-over-year (YOY).

Net income climbed to $1.94 billion, up about 14%, while adjusted EPS came in around $3.81. Free cash flow rose to $14.4 billion for the full fiscal year, and cash generation remains one of the biggest reasons CRM stock still has supporters.

CEO Marc Benioff called the quarter “phenomenal” and said Salesforce is moving deeper into what he calls the Agentic Enterprise. The company also ended the year with $72 billion in remaining performance obligations, which points to a strong backlog.

For the next quarter, Salesforce guided revenue between $11.03 billion and $11.08 billion. For fiscal 2027, the firm foresees revenue of $45.8 billion to $46.2 billion. That points to growth, but not the kind of explosive growth for which the market usually pays a premium.

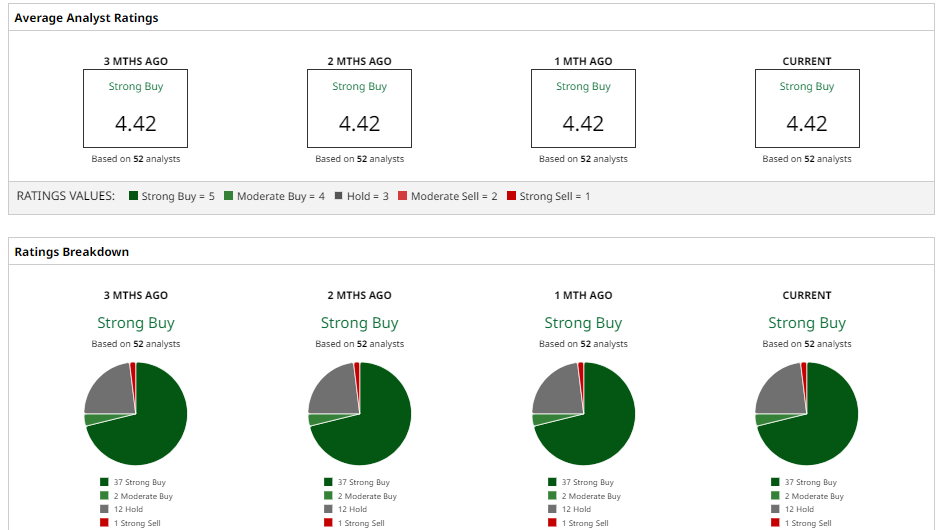

What Do Analysts Think of CRM Stock?

Wall Street is not fully on the same page with CRM stock. Morgan Stanley recently kept an “Overweight” rating and set a $287 target, while TD Cowen kept a “Buy” rating with a $250 target. Meanwhile, BMO trimmed its target to $235 from $275, and UBS cut its target to $200 from $260. Both sounded more cautious on adoption. However, JMP Securities went the other way and lifted its target to $315, saying Agentforce growth still looks promising.

Overall, the consensus is a “Strong Buy” rating for CRM stock. The average target sits at $276.18, which points to meaningful potential upside of 58% from current levels.

www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.