Berkshire Hathaway (BRK.B) made some interesting changes to its portfolio of publicly traded securities in Q1 2026. Among others, the company added new stakes in Macy’s (M) and Delta Airlines (DAL) in the quarter. The addition of Delta was particularly intriguing as Warren Buffett had previously sold stakes in all four leading U.S. airline companies in 2020, and admitted to making a “mistake” in buying them.

The 13F filing, which was the first since Greg Abel took over as CEO, showed that the conglomerate dumped several smaller holdings, reducing the total number of positions from 42 to 29. Domino’s Pizza (DPZ) was among the stocks that Berkshire axed in the quarter. The company bought the stake in Q3 2024 and, based on the pizza giant’s price action over the period, exited the position at a significant loss.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

In my previous article, I had noted that DPZ stock’s risk-reward looked unattractive. I wasn’t sold on the stock’s outlook when Berkshire first disclosed its position either. Domino’s hit a multi-year low this week, but recovered slightly from those levels. In this article, we’ll explore whether Domino’s Pizza stock is a sell or has the crash made it attractive instead. Let’s begin by looking at its dividend policy.

www.barchart.com

www.barchart.comDomino’s Pizza Has a Fat Dividend Yield

Domino’s Pizza has a dividend yield of around 2.6%, which is over twice that of its average S&P 500 Index ($SPX) counterpart. Moreover, the payouts have increased at an annualized rate of nearly 20% over the last 10 years, including a 15% increase for this year. The company generates healthy free cash flows, and the payout ratio is below 45%, which looks quite conservative. Along with dividends, Domino’s has been spending cash on share repurchases and deleveraging its balance sheet.

However, these dividends haven’t helped mask the almost 40% decline in DPZ stock over the last two years. Domino’s is among those stocks where investors should expect the bulk of the returns from capital appreciation, with the dividends being only the proverbial cherry on the top.

DPZ Stock Forecast

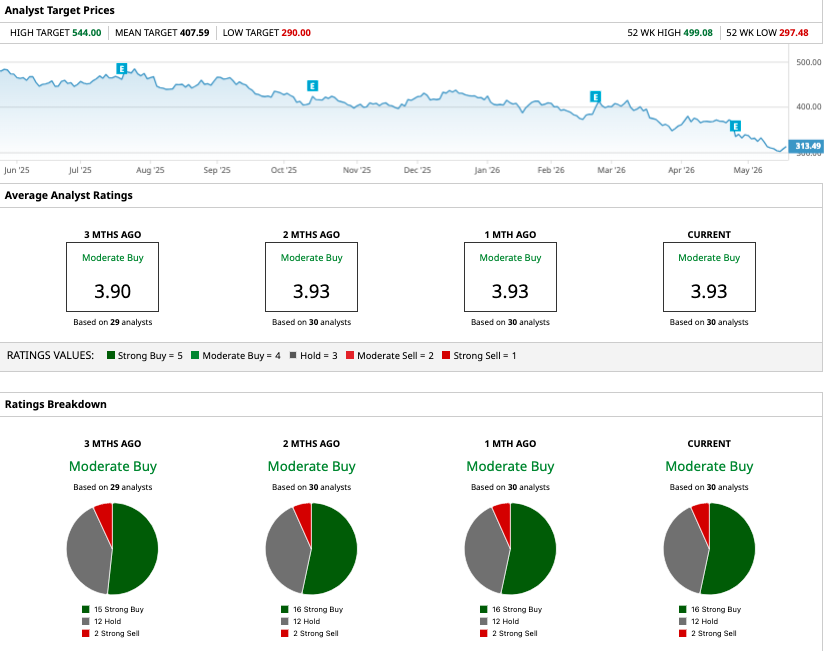

DPZ has a consensus rating of “Moderate Buy” from the 29 analysts polled by Barchart. While its overall rating hasn’t changed, brokerages have been gradually lowering their target price. In particular, sell-side analysts went on an overdrive in cutting DPZ’s target price following its Q1 2026 earnings last month.

Among others, RBC and Wells Fargo lowered the stock’s target price from $400 to $350, while Goldman Sachs lowered its by a similar quantum to $430. Some of the deepest cuts came from NorthCoast Research and Evercore ISI, which cut their target prices from $525 to $445 and $510 to $400, respectively. Domino’s has a mean target price of $407.59, which is 30% higher than current price levels.

Notably, Domino’s missed both top and bottom line estimates in the March quarter. Specifically, its U.S. same-store sales grew 0.9% year-over-year in the quarter, which was less than half of what the Street expected. The company also lowered its 2026 U.S. same-store sales forecast from 3% growth to low-single-digit growth.

Meanwhile, DPZ’s woes are not about missing estimates in a quarter, and some of the challenges are deep rooted. Pizza has lost out to other cuisines, and pizza restaurants, which were once second in sales in the U.S., dropped to sixth in 2024. Pizza chains have lost some of their moat with the advent of delivery apps like Uber Eats (UBER) and DoorDash (DASH), which let smaller restaurants also offer deliveries to customers.

There is also a pizza price war in the U.S., and Domino’s key U.S. competitors, namely Pizza Hut (YUM) and Papa John's (PZZA), have been offering promotions to match its pricing. U.S. consumer sentiment has also been weak, thanks to higher gas prices that are putting pressure on disposable incomes.

www.barchart.com

www.barchart.comShould You Buy Domino’s Pizza Stock?

Meanwhile, it's not all gloom and doom for Domino's. U.S. store closures by its competitors would help Domino’s increase its same-store sales and, by extension, its market share. Also, as the situation in the Middle East stabilizes and oil prices pull back from the current levels, disposable incomes could rise, helping buoy sales for restaurants.

I believe DPZ’s risk-reward has started to look attractive here, as the forward price-to-earnings (P/E) multiple of under 16x seems to bake in most of the pessimism. The stock seems to have bottomed out at these levels, and downside looks limited, unless of course we see a broader market meltdown.

On the date of publication, Mohit Oberoi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Berkshire Hathaway Gave Up on This Underperforming Dividend Stock, But It May Be Time for You to Buy the Dip Arm Surges on New $300 Price Target: ARM Stock Is at the ‘Center of the Renaissance’ in CPUs Massive Layoffs at Meta Platforms Are Now Underway. What That Means for META Stock. Stifel Just Raised Its Price Target on Palo Alto Networks. Here's Why.