Billionaire hedge fund veteran Dan Loeb once waved the Microsoft Corporation (MSFT) flag louder than most institutional investors on Wall Street. During Q3 2025, the Third Point founder doubled down on Microsoft, turning the stock into the Fund’s third largest holding at 6.9% of the portfolio, an unequivocal bet on the tech giant's artificial intelligence (AI) ambitions.

Yet, the confidence vanished in one fell swoop during Q1 2026 after Third Point completely dumped its 925,000 share Microsoft position, ending an investment the firm had carried since late 2022. Loeb pulled the plug as he steered capital away from mega-cap technology names toward event-driven investing, activism, and private credit opportunities that he described as “massive.”

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

MSFT stock did not do Loeb any favors this year either. Its shares stumbled badly in 2026, falling 14.18% year-to-date (YTD) as investors wrestled with swelling AI infrastructure costs that still have not produced matching revenue growth. Slower Azure expansion added fuel to the fire while concerns around heavy customer concentration in Microsoft’s cloud backlog kept nerves on edge.

Even so, Loeb’s exit appears tied more to portfolio reshuffling than any collapse in Microsoft’s long-term muscle. Wall Street still treats the company as one of technology’s biggest heavyweights despite the recent bruising.

About Microsoft Stock

Headquartered in Redmond, Washington, Microsoft commands one of the biggest technology ecosystems on the planet, covering cloud computing, workplace software, AI, gaming, search, and professional networking.

Carrying a market cap $3.11 trillion, the company operates powerhouse businesses that include Windows, Azure, Microsoft 365, Xbox, LinkedIn, GitHub, and Copilot while helping consumers and enterprises communicate, build software, work digitally, and access entertainment around the globe.

Even at that scale, the stock has had a rough stretch. It shed nearly 7.81% over the last 52 weeks and dropped another 2.26% in just the last month alone, as worries about AI spending, slowing cloud momentum, and stretched valuations kept piling on.

www.barchart.com

www.barchart.com Nevertheless, MSFT stock is currently trading at 24.98 times forward adjusted earnings and 9.44 times sales. Both figures sit above the industry benchmark but actually come in at a discount relative to the stock's own five-year average multiple, which softens the blow a little.

On the income front, the company has raised dividends for 21 consecutive years and now pays an annual dividend of $3.64 per share, giving investors a dividend yield of 0.87%. Its latest dividend payment of $0.91 is scheduled to be paid on June 11 to shareholders of record as of May 21.

Microsoft Surpasses Q3 Earnings

On April 29, Microsoft posted its Q3 FY2026 results which cleared the bar Wall Street had set. Revenue climbed 18.3% year-over-year (YOY) to $82.89 billion, beating analyst estimates of $81.39 billion. EPS rose 23.4% from the year-ago value to $4.27, topping the $4.06 Street’s forecast.

Microsoft called it a record third quarter, and the numbers back that up. Microsoft Cloud crossed $54 billion in revenue, up 29% YOY. The company’s AI business also flexed serious muscle as its annual revenue run rate surged beyond $37 billion with blistering 123% YOY growth.

The blockbuster numbers still came with a price tag. Gross margin slipped to 68% as Microsoft poured cash into AI infrastructure while heavier AI product usage also squeezed margins. Efficiency gains across Azure and Microsoft 365 Commercial cloud softened part of the blow.

Capital expenditures together with finance leases reached a staggering $31.9 billion during the quarter. Coming to balance sheet, cash and cash equivalents amounted to $32.1 billion on March 31, up from $30.2 billion on June 30, 2025.

Looking ahead, management expects Q4 FY2026 revenue between $86.7 billion and $87.8 billion, reflecting growth between 13% and 15%. The company also plans to push capital spending above $40 billion as it races to bring additional capacity online.

Moreover, Microsoft expects capital expenditures for CY2026 to reach roughly $190 billion as soaring memory costs tighten the screws. The figure includes nearly $25 billion tied directly to higher component pricing.

On the other hand, analysts expect Q4 FY2026 EPS to rise 15.3% YOY to $4.21. Full year FY2026 bottom line could jump 22.9% to $16.76 while the following fiscal year may deliver another 15% climb to $19.28.

What Do Analysts Expect for Microsoft Stock?

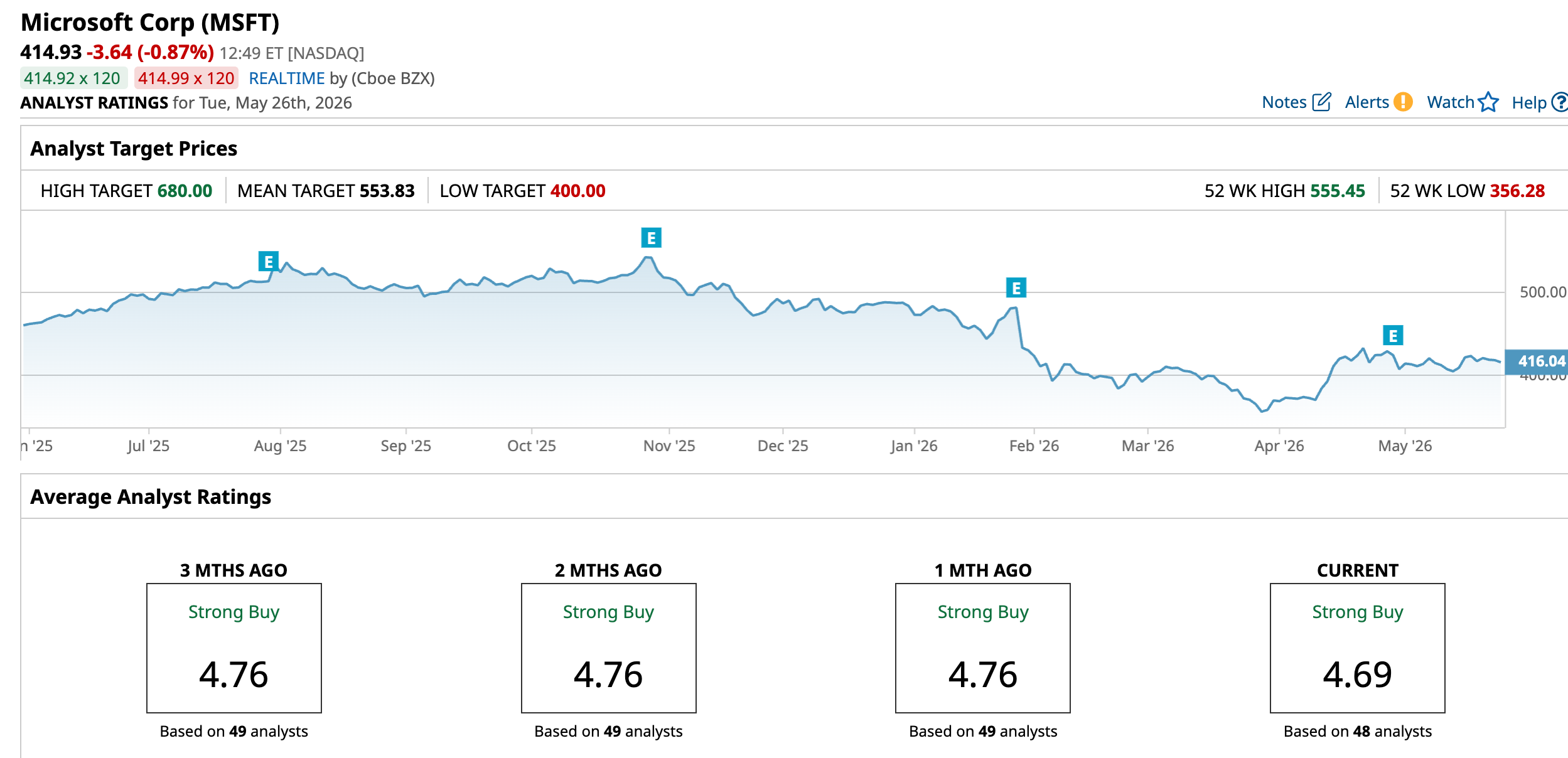

Wall Street still appears firmly in Microsoft’s corner. Wedbush Securities lifted its MSFT price target to $575 while maintaining an “Outperform” rating.

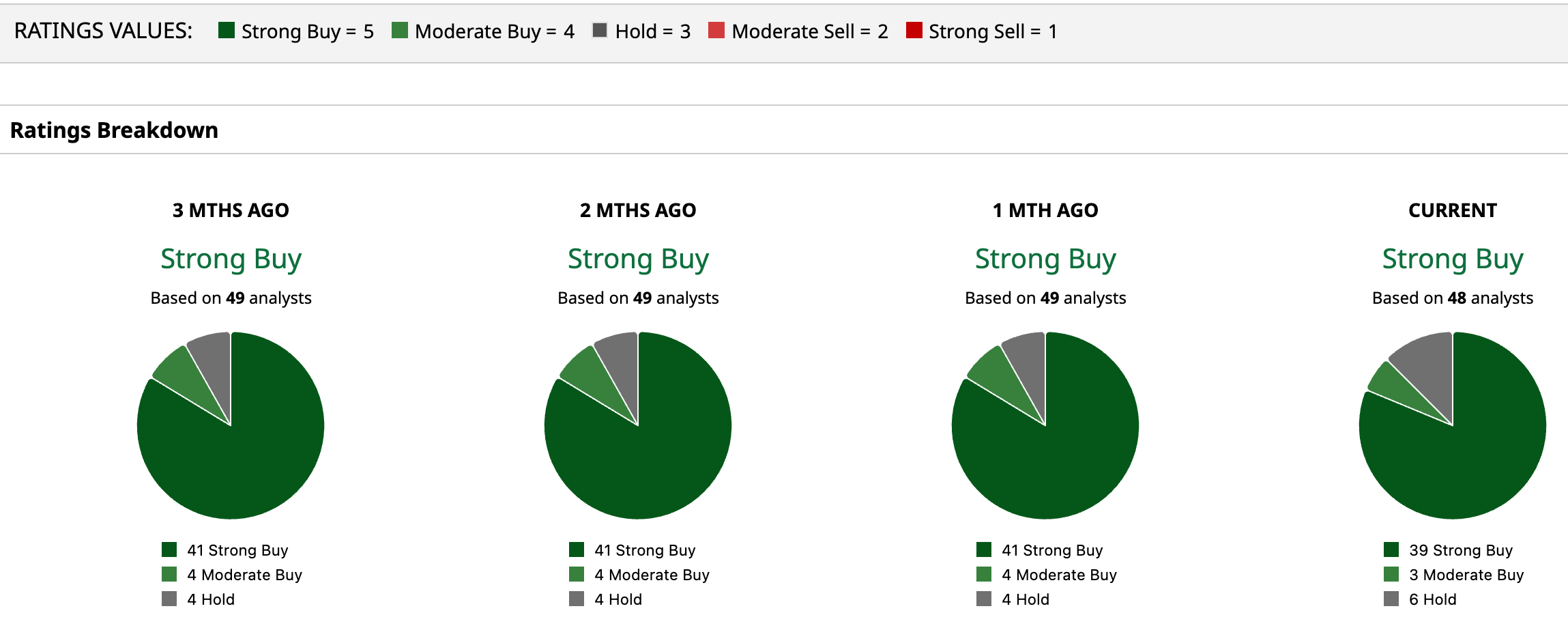

The broader Wall Street picture reads just as bullishly with the stock carrying an overall rating of “Strong Buy.” Among 48 analysts covering the stock, 39 rate the stock a “Strong Buy,” three call it a “Moderate Buy,” while six prefer to sit tight with “Hold” ratings.

MSFT’s average price target of $553.83 represents potential upside of 33.5%. Meanwhile, the Street-High target of $680 set by Ivan Feinseth from Tigress Financial Partners suggests a gain of 63.9% from current levels. Feinseth assigned the stock a “Buy” rating and believes Microsoft’s “AI driven cloud flywheel is driving accelerating high margin revenue and cash flow growth.”

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Billionaire Dan Loeb Cashed Out of Microsoft Stock. Shares Are Down 14.2% YTD. Nvidia Just Raised Its Dividend by 2,400%. NVDA Stock Is Still a Bet on Growth, Not Income. Short Sellers Aren’t Relenting Against Qualcomm. The Chipmaker Needs to Quickly Deliver on Its AI Pivot for Bulls to Win. Microsoft vs. Apple Stock: The Numbers Reveal a Clear Winner Heading Into H2 2026