Powell Industries, Inc. POWL missed earnings and revenue estimates in the first quarter of 2026 and remains mired in headwinds from high operating costs and expenses.

In fiscal 2025 (ended September 2025), Powell’s cost of sales increased 5.5% year over year to $779.9 million. The cost of sales, as a percentage of revenues, was 70.6% for the period. Selling, general and administrative expenses also rose 12.4% in the same period. The rise was attributable to an increase in raw material costs and higher compensation costs and expenses.

The trend continued in the first six months of fiscal 2026 (ended March 2026), with cost of sales rising 3% year over year, and selling, general and administrative expenses increasing 17.9%. The rise in operating expenses weighed on the company’s margins and profitability.

In second-quarter fiscal 2026, the company’s gross profit margin contracted 30 basis points (bps) to 29.6%, while the operating margin declined 170 bps to 19.4%. It’s worth noting that material costs represented 45% of the company’s revenues in fiscal 2025, 47% in fiscal 2024 and 49% in fiscal 2023.

POWL has also experienced supply-chain disruptions in the utility and commercial sectors in recent quarters that resulted in delays and increased costs. Despite moderation, the persistence of supply-chain issues is likely to continue impacting its margins and profitability in the quarters ahead.

Peers’ Margin Performance

Among its major peers, EnerSys ENS is facing cost pressure. In fiscal 2026 (ended March 2026), the company’s cost of sales increased 5.2% year over year, while its operating expenses rose 2%. EnerSys’ gross margin declined 100 bps to 29.2% in the year.

Franklin Electric Co, Inc.’s FELE cost of sales rose 11.7% year over year in first-quarter 2026. The company’s SG&A expenses also increased 2.8% year over year. Franklin Electric’s gross margin declined 10 bps to 9.6% in the quarter.

POWL’s Price Performance, Valuation and Estimates

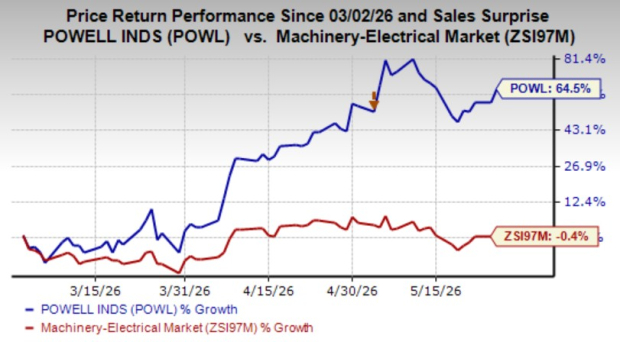

Shares of Powell have surged 64.5% in the past three months against the industry’s decline of 0.4%.

Image Source: Zacks Investment Research

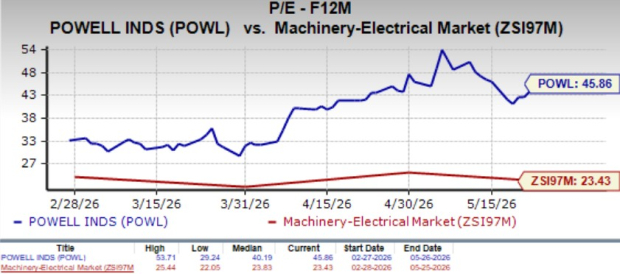

From a valuation standpoint, POWL is trading at a forward price-to-earnings ratio of 45.86X, above the industry’s average of 23.43X. Powell carries a Value Score of F.

Image Source: Zacks Investment Research

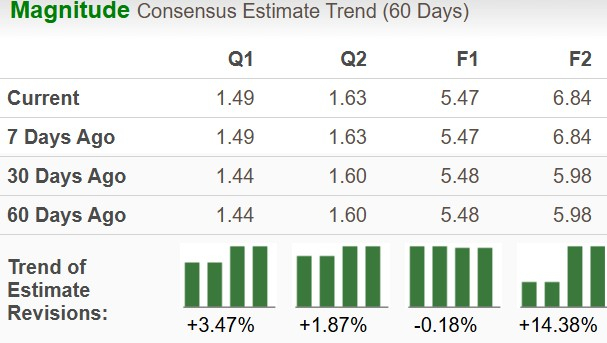

The Zacks Consensus Estimate for POWL’s fiscal 2026 (ending September 2026) earnings has inched down 0.2% over the past 60 days.

Image Source: Zacks Investment Research

The company currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Franklin Electric Co., Inc. (FELE): Free Stock Analysis Report

Enersys (ENS): Free Stock Analysis Report

Powell Industries, Inc. (POWL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).