New research from Goldman Sachs was headlined by an 8,000 year-end target on the S&P 500 Index ($SPX), nearly 10% higher than this year’s already strong up move. This major upgrade is driven by what analysts describe as “robust, corporate earnings power.” The mainstream narrative is simple: Corporate America is thriving, the bull market is charging ahead, and the fundamental backdrop has never looked healthier.

But if you look past the sensational headline and pop the hood on the underlying data, the reality is starkly different.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

The broader index isn’t experiencing a healthy, diversified economic advance. Instead, the entire S&P 500 has effectively mutated into an extreme, highly concentrated two-stock dependency model.

And while I have been chronicling the stock market’s increasingly narrow participation here for a while now, it is getting worse, not better. That’s what Goldman’s data tells me.

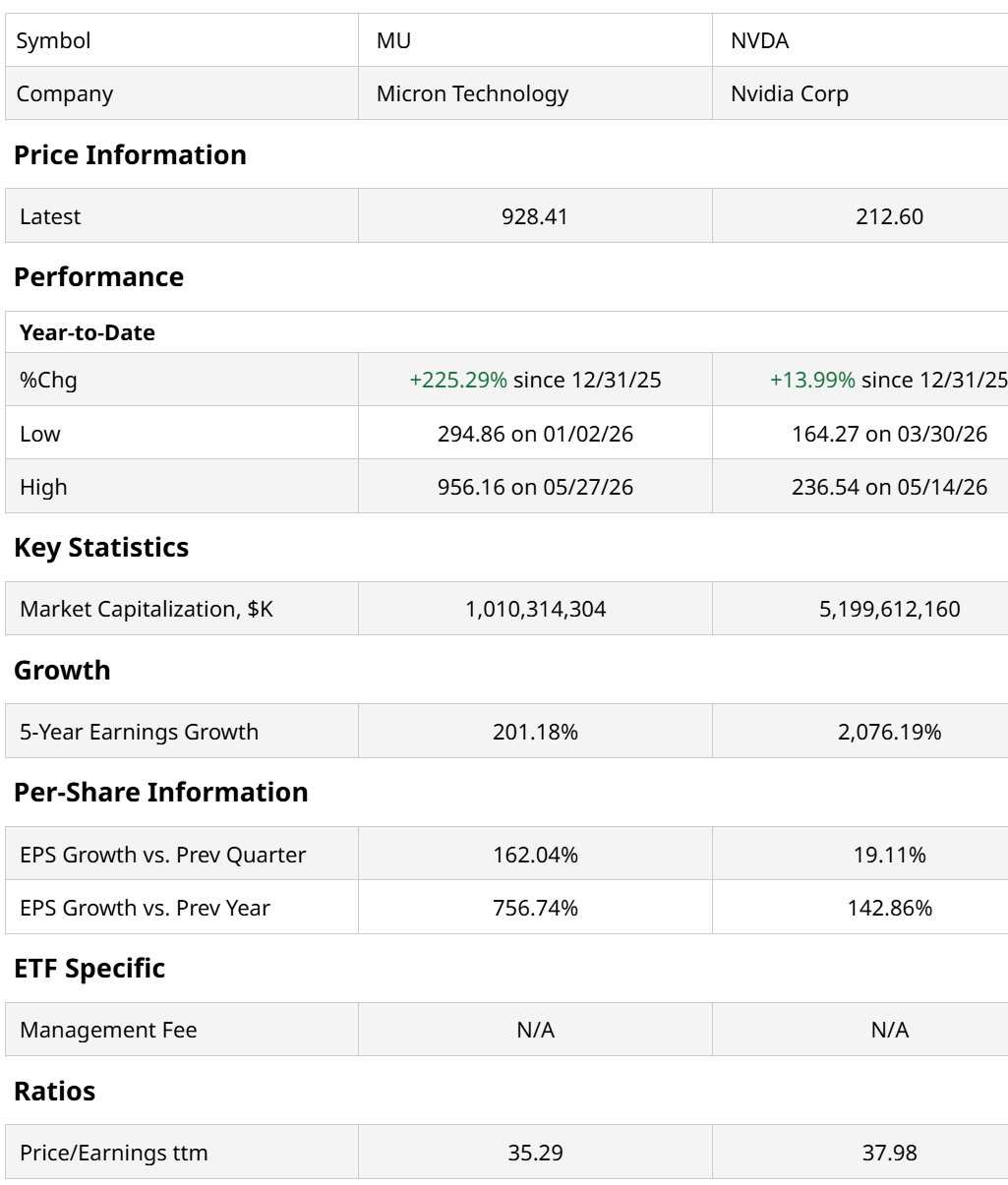

According to the firm’s own numbers, a staggering one-third of all S&P 500 earnings growth in 2026 will be driven by just two companies: Nvidia (NVDA) and Micron Technology (MU). This is so absurd!

The S&P 500 is supposed to represent a broad, diversified cross-section of the 500 largest publicly traded corporations in the United States. Yet, a single GPU designer and a single high-bandwidth memory manufacturer are projected to shoulder roughly 33% of the entire index’s bottom-line expansion this year.

Holy Earnings Duopoly, Batman!

Goldman notes that when you widen the lens to the 10 largest corporate giants — a list heavily rounded out by tech hyperscalers like Alphabet (GOOG), Broadcom (AVGO), and Meta (META), they represent an astonishing 64% of all projected S&P 500 EPS growth for 2026.

www.barchart.com

www.barchart.com This is not a story of widespread corporate prosperity. It is a story of a historic, unprecedented capital expenditure haul. A massive chunk of global liquidity is being extracted from traditional economic sectors and poured directly into a singular destination: AI data center infrastructure.

NVDA and MU are sitting at the toll booth of that funnel, capturing a disproportionate share of corporate America’s realized cash flows while the remaining hundreds of legacy companies scramble for proverbial scraps.

If you pull Nvidia, Micron, and the surrounding AI infrastructure names entirely out of the equation, the S&P 500’s earnings picture looks very fragile. Goldman’s historical data reveals that when you exclude the core AI infrastructure complex, earnings expectations for the rest of the market have been essentially flatlining all year.

As I’ve pointed out here recently, the median stock in the index is quietly trading well below its own 52-week high, indicating that severe distribution is happening beneath the surface while the cap-weighted averages print record numbers. You just won’t hear about it in the daily headlines.

This smacks of a massive time bomb lurking in late 2026 and into 2027: the depreciation trap. Right now, the massive cloud computing giants are spending money like drunken sailors, booking hundreds of billions in capital expenditures to stockpile chips and build real estate for data centers.

But those hardware assets have a shelf life. That’s fact, not debate. To that end, Goldman explicitly warns that as we cross into next year, soaring depreciation expenses from these heavy infrastructure investments will begin to aggressively bite into corporate profit margins, acting as a severe mechanical drag on the index’s forward EPS. Heck, they might as well say it more like this:

Good news: we’re going to 800 on the SPY ETF. Bad news: then we’re going to 400!

When a market’s growth scoreboard is entirely dictated by just two or three players, the margin for error is effectively zero. What could break this isolated AI boom?

A single fundamental supply chain hiccup A mild slowdown in corporate AI adoption A sudden realization that the monetization of these data centers is taking longer than expected. The “ROI follow through” issue.Enjoy the momentum while the tape allows it, but recognize that a market supported by a tiny handful of pillars is top-heavy, highly fragile, and fundamentally hollow at its core.

Rob Isbitts created the ROAR Score, based on his 40+ years of technical analysis experience. ROAR helps DIY investors manage risk and create their own portfolios. For Rob’s written research, check out ETFYourself.com.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Nvidia and Micron Stocks Are Almost Exclusively Driving S&P Earnings Strength. These 3 Very Real Risks Could End It All. Hundreds of ETFs Hit 52-Week Highs This Week. Here Are 3 Worth Owning Long Term. Don’t Ignore Basic Bond Math and Jump Into TIPS: The ‘Inflation Hedge’ Story Isn’t Everything Telecom Stocks Are Surging Ahead of the SpaceX IPO. This Chart Reminds Us All Rockets Come Crashing Back to Earth Eventually.