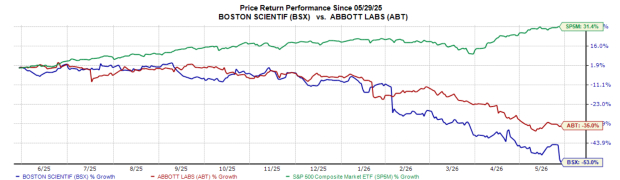

In the past year, shares of Boston Scientific BSX and Abbott Laboratories ABT have lost 53% and 35%, respectively, significantly underperforming the S&P 500’s 31.4% gain. U.S. medical stocks are facing pressure in 2026 due to restrictive regulatory changes, lower-than-expected government reimbursement rates and evolving healthcare policies.

Despite these hurdles, both Boston Scientific and Medtronic delivered robust first-quarter 2026 financial results. It is time for investors to assess whether this momentum can extend through 2026. Let’s find out.

Image Source: Zacks Investment Research

The Case for BSX

Boston Scientific reported strong sales growth of 11.6% on a reported basis, exceeding the company’s guidance of 10.5% to 12.0%. Across its key business segments, MedSurg delivered net sales growth of 7.8%, while Cardiovascular grew 13.5%. The company continued to see strong demand for its WATCHMAN left atrial appendage closure (LAAC) platform and FARAPULSE pulsed field ablation (PFA) platform, which remained key growth drivers during the quarter.

During the quarter, Boston Scientific dealt with multiple operational challenges that led management to reduce full-year guidance. In the WATCHMAN franchise, stand-alone procedure volumes weakened amid hospital capacity limitations, reimbursement changes, workflow disruptions and an increasing shift toward concomitant procedures. The company’s EP segment also experienced heightened competitive intensity, contributing to larger-than-anticipated market-share losses, especially in the U.S. market.

Within Urology, the stone business was affected by China’s volume-based procurement (VBP) program and product gaps in the core portfolio. The company also highlighted supply-chain disruptions in Endoscopy, inventory charges related to the discontinuation of the POLARx cryoablation system and discontinuation of the ACURATE platform, which mainly affected the EMEA region.

Boston Scientific also noted the impact of the Middle East conflict on its Cardiac Rhythm Management business. Overall, management acknowledged that 2026 has become a more challenging year than initially anticipated due to these operational, competitive, and macroeconomic pressures.

The Case for ABT

Abbott reported first-quarter sales growth of 7.8% on a reported basis. The quarter also marked a significant strategic milestone with its acquisition of Exact Sciences. The deal adds a high-growth business to Abbott’s portfolio, strengthening its leadership position in Diagnostics while expanding its presence in the rapidly growing cancer-diagnostics market.

Abbott also advanced several initiatives within its Medical Devices pipeline during the quarter. The company received earlier-than-expected regulatory approval and launched two new PFA catheters. It completed patient enrollment for its Catalyst left atrial appendage device trial and began development activities for an implantable extravascular ICD product.

Pressure persisted within Abbott’s Core Laboratory Diagnostics business because of China’s volume-based procurement (VBP) program and ongoing COVID-related disruptions. Although the Chinese market has started to stabilize, pricing compression and volume pressure linked to VBP continue to weigh on the business.

Abbott implemented strategic pricing actions in late 2025 to improve competitiveness and support volume recovery within the Nutrition business. Per the latest update, the business is still in an early recovery phase and requires further execution and new product launches to return to stronger growth. Within the Diabetes Care segment, continuous glucose monitoring (CGM) growth was affected by delays in the renewal process for an international tender, as well as challenging year-over-year comparisons tied to inventory restocking activity in the prior-year period.

Abbott identified macroeconomic and geopolitical uncertainty as ongoing risk factors. The company is monitoring potential impacts from the Middle East conflict, including pressure on freight availability, shipping logistics, oil and resin costs, and broader supply-chain disruptions. Although the direct financial impact remained limited during the first quarter, Abbott noted operational challenges related to ensuring timely product deliveries into affected regions.

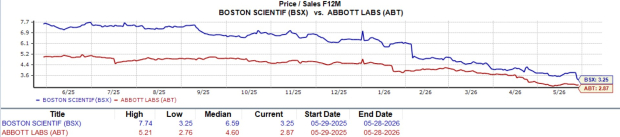

Valuation: BSX vs. ABT

Boston Scientific currently trades at a forward, one-year, price-to-sales (P/S) of 3.25X, lower than its median. Abbott’s 2.87X P/S also sits below its median. Abbott trades cheaper than Boston Scientific.

Image Source: Zacks Investment Research

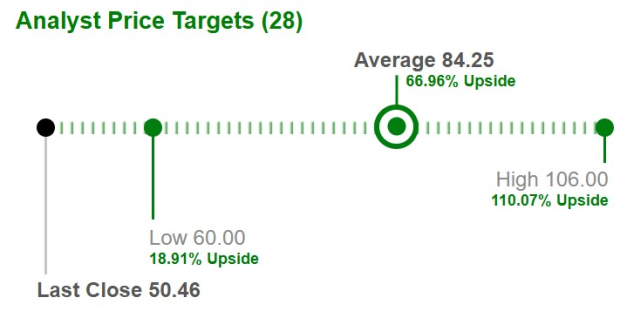

Short Term Price Target Favors BSX Over ABT

BSX: Based on short-term price targets offered by 28 analysts, the average price target of $84.25 represents an increase of 66.96% from the last closing price.

Image Source: Zacks Investment Research

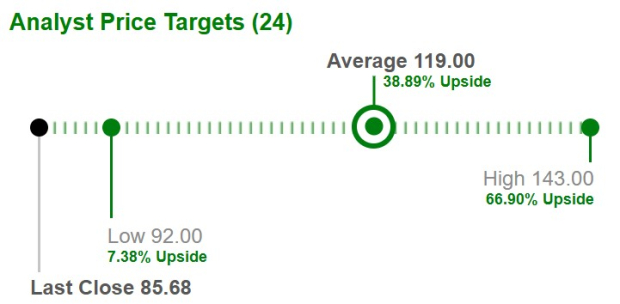

ABT: Based on short-term price targets offered by 24 analysts, the average price target of $ 119.00 represents an increase of 38.89% from the last closing price.

Image Source: Zacks Investment Research

End Note

Boston Scientific delivered strong quarterly growth, supported by robust demand for its WATCHMAN and FARAPULSE platforms. However, the company faced several headwinds during the quarter, prompting management to lower its full-year outlook.

Abbott also reported solid first-quarter growth, driven by the acquisition of Exact Sciences and continued progress across its Medical Devices pipeline. Despite these positives, the company continued to face pressure from ongoing macroeconomic and geopolitical uncertainties, including supply-chain and logistics risks linked to the Middle East conflict.

Both BSX and ABT currently carry a Zacks Rank #4 (Sell), suggesting that existing shareholders may want to consider reducing or exiting their positions. However, based on valuation and one-year stock-price performance, ABT appears better positioned than BSX at current levels.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Abbott Laboratories (ABT): Free Stock Analysis Report

Boston Scientific Corporation (BSX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).