Redwire (RDW) is one of several space stocks catching a powerful bid as investors pile into the sector ahead of the expected SpaceX initial public offering (IPO). The enthusiasm has lifted names across the industry, but Redwire stands out for its combination of operating momentum, contract wins, and a stock chart that has already gone nearly vertical.

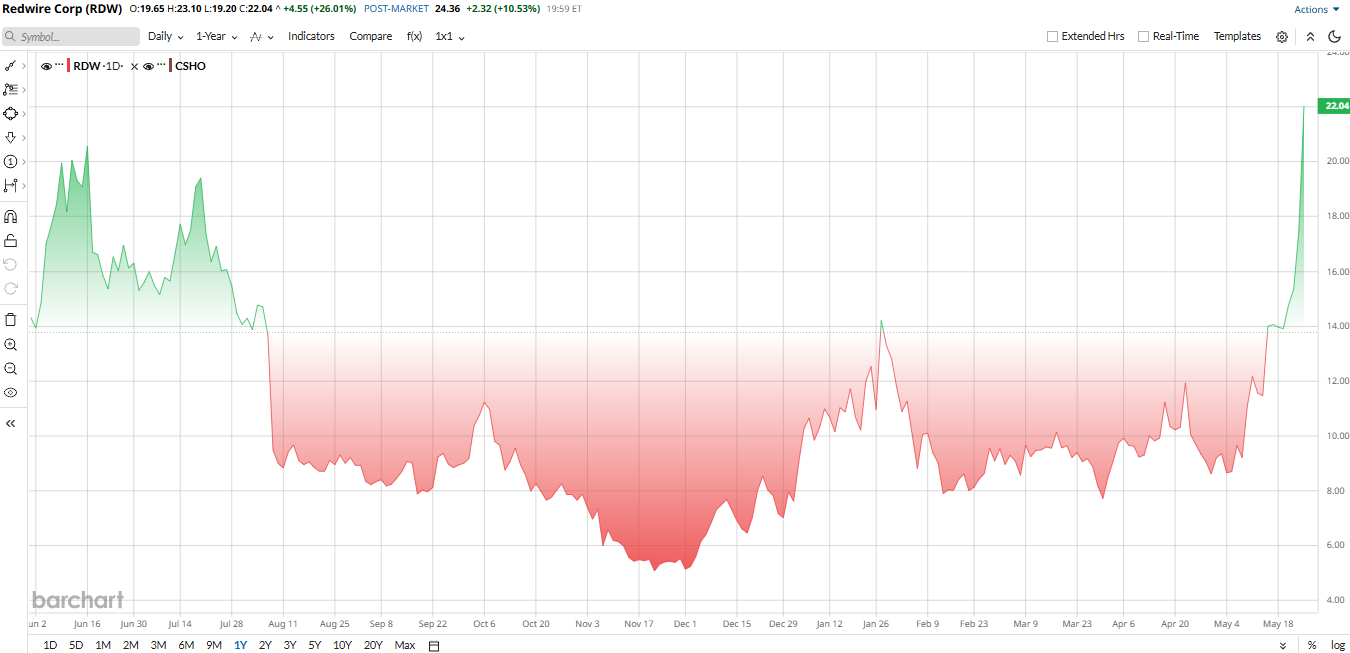

Over the past 12 months, RDW stock has climbed about 59%, and in 2026 alone, it has surged roughly 220% year-to-date (YTD). As of this writing, the stock trades around the $24 mark, well above its 50-day moving average near $11.50 and its 200-day moving average near $9. That kind of move shows both broad sector excitement and growing confidence that Redwire can convert its backlog into real growth.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

The latest wave of buying is also tied back to the SpaceX IPO narrative. SpaceX is reportedly targeting a valuation as high as $1.75 trillion, which has helped fuel a broader rerating across the space sector.

On May 26, Redwire shares jumped 26%, hitting fresh highs alongside names like Rocket Lab (RKLB) and Momentus (MNTS). It looks like investors are not just betting on one company — they're betting on the whole space ecosystem.

www.barchart.com

www.barchart.com A Rich Valuation for a High-Growth Story

Redwire now has a market capitalization of roughly $4.97 billion and an enterprise value near $5.04 billion. That is a sizable valuation for a company that is still unprofitable, especially when compared with the broader aerospace and defense group.

RDW stock trades at a price-to-sales (P/S) ratio of 13.7 times, which is a hefty premium. For investors, that means the market is already assigning a strong growth premium to future revenue gains and margin improvement. The setup can work if execution stays strong, but it also leaves the stock vulnerable if growth slows or contracts slip.

Management’s 2026 revenue guidance of $450 million to $500 million supports the growth case, but it also shows how much of the valuation depends on continued top-line expansion. At the midpoint, that would imply roughly 42% growth from 2025. That is impressive, but it is also the kind of number the market may already be pricing in.

Q1 Showed Real Progress

Redwire’s first-quarter 2026 results gave bulls more to work with. Revenue came in at $97 million, up 58% from a year ago, helped by the Edge Autonomy acquisition, a better contract mix, and new wins across spacecraft and defense technology.

The Space segment generated $52.7 million in revenue, while Defense Tech contributed $44.3 million. That split highlights Redwire’s push to build a broader platform across both commercial and national security markets.

The company also pointed to a strong demand backdrop. CEO Peter Cannito said Redwire posted a book-to-bill ratio of 1.92 and a record backlog of $498.1 million, up 71% from a year ago. That is one of the most important figures in the story because it suggests the company has meaningful business already lined up.

The bottom line was still messy. Net loss widened to $76.5 million from $2.9 million a year earlier. More than $44 million of that loss came from non-recurring items, including a $42.5 million non-cash equity compensation charge tied to the Edge Autonomy deal. On an adjusted basis, Redwire reported a loss of $0.18 per share, missing estimates by a couple of cents.

There were some clear positives in the quarter, though. Gross margin improved to 26.6% from 14.7% a year earlier and 9.6% in Q4 2025. Free cash flow also improved by $36 million year-over-year (YOY).

Lastly, Redwire ended the quarter with $175.2 million in total liquidity, including $145.2 million in cash and equivalents and an undrawn $30 million revolver.

Analysts See Growth, But the Risk Is Real

Wall Street is not calling for profitability yet. The current analyst consensus expects Redwire to generate about $476.6 million in revenue for full-year 2026 and post an adjusted loss of $0.70 per share.

That outlook fits the current story. Analysts appear to believe Redwire can keep growing at a healthy pace, but they are also signaling that the company still has a long way to go before it becomes a consistent earnings winner.

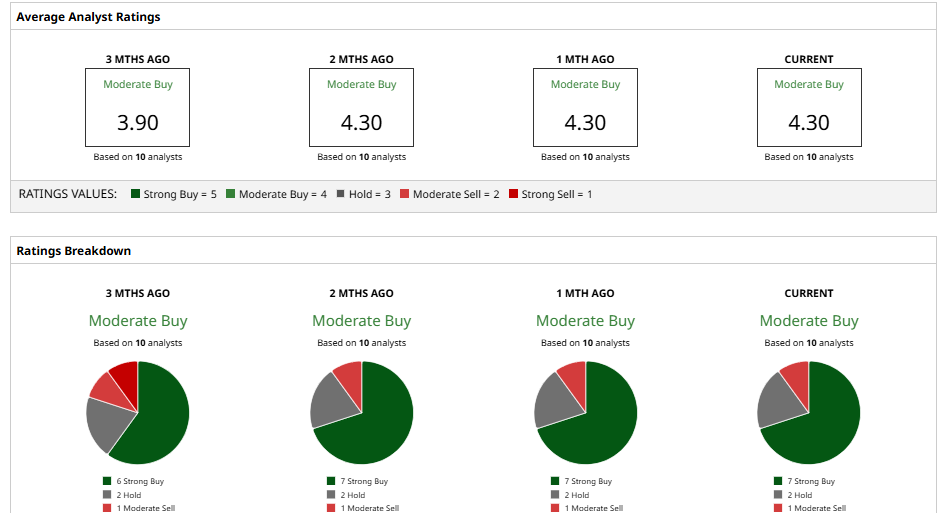

For now, the consensus from Wall Street is a “Moderate Buy” rating, but the stock is trading above its Street-high target of $22. That means RDW stock has already priced in too much, so a sharp pullback could happen if SpaceX is not able to deliver the record-breaking IPO analysts expect.

www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

A Giant Short Squeeze Could Be Brewing in Wolfspeed Stock The SpaceX IPO Is a Bet That Retail Investors Love Elon Musk So Much They’ll Fund His Money-Losing Empire You’ve Likely Never Heard of This Stock, But Data Center Demand Just Took Shares to New 52-Week Highs Starbucks’ AI Disaster and Sam Altman’s U-Turn Prove That AI Still Needs Humans