Global cyberattacks reached a record average of 1,968 per week in 2025, up 70% from 2023, according to Check Point Software’s 2026 Cyber Security Report. At the same time, Anthropic’s Claude Mythos model has shown it can find and exploit software vulnerabilities that had gone undetected, adding to concerns across the industry. That is pushing companies to spend more on cybersecurity, and Gartner expects AI cybersecurity spending alone to rise to more than $51 billion in 2026, up from about $26 billion in 2025.

Palo Alto Networks (PANW) is right in the middle of that trend. The stock had already jumped more than 70% in less than two months, climbing from below $150 at the end of March to around $260 and hitting record highs. The move has been driven by the launch of its Idira identity security platform, rising confidence from analysts, and growing demand for tools that can help companies deal with AI-related threats. Now Wedbush has gone even further, setting a new Street-high $325 price target on Palo Alto Networks and calling it one of the clearest winners from the AI demand wave.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

With the stock already up more than 70% and analyst targets still moving higher, does Palo Alto Networks still have more room to run, or has the market already priced in most of the good news?

A Look at the Numbers

Palo Alto is one of the biggest cybersecurity companies focused mainly on helping businesses protect their networks, cloud systems, and security operations.

The stock is up 37.26% over the past 52 weeks and has gained 39.94% so far this year, showing that investors have stayed bullish on the name.

www.barchart.com

www.barchart.comEven so, the stock is not cheap. Palo Alto Networks trades at a forward price-to-earnings of 120.12 times, well above the sector average of 33.34 times, which shows the market is expecting strong growth.

In fiscal Q2 2026, revenue rose 15% year-over-year (YOY) to $2.6 billion. Next-generation security ARR climbed 33% to $6.3 billion, showing strong demand for its newer products. Remaining performance obligations rose 23% to $16.0 billion, which gives the company solid revenue visibility going forward. Earnings also improved, with GAAP net income at $432 million, or $0.61 per share, and non-GAAP net income at $732 million, or $1.03 per share.

For the current quarter, Palo Alto Networks expects revenue of up to $2.945 billion, which would mean as much as 29% YOY growth. For full-year 2026, it expects revenue of about $11.28 billion to $11.31 billion, along with a non-GAAP operating margin of 28.5% to 29.0% and an adjusted free cash flow margin of 37%.

What Is Driving Growth?

Palo Alto Networks’ new Idira platform is designed to secure every kind of identity inside a company, including people, machines, and AI agents. That matters because identity has become a major weak spot for businesses. In the past year alone, nine out of 10 organizations faced an identity-related breach.

The problem is getting bigger as machines and AI identities now outnumber human ones by 109 to one, while 61% of privileged access requests are still handled through standing access. Idira is meant to fix that by giving companies better visibility and tighter control over who or what gets access.

In addition, Palo Alto Networks is moving deeper into AI security through its planned acquisition of Portkey. The latter gives companies a central system to manage and secure AI agents as they operate across enterprise networks. These agents can make decisions and access sensitive systems on their own, so having a control layer in place is becoming more important. Palo Alto Networks plans to use Portkey as the AI gateway for Prisma AIRS.

The company has completed its acquisition of Koi, which adds protection at the device level. As more businesses use AI coding tools and other autonomous software, endpoint risks are rising too. By bringing Koi into Prisma AIRS and Cortex XDR, Palo Alto Networks is adding tools to spot and fix risks tied to AI software and agent activity on endpoints.

Wall Street’s View Ahead

Ahead of Palo Alto Networks’ upcoming earnings release on June 2 after the market close, analysts expect the company to report $0.43 per share for the quarter ending April 2026, unchanged from the same period a year earlier. Estimates for the following quarter ending July 2026 rise to $0.55, pointing to 30.95% growth from $0.42 last year. For the full fiscal year 2026, the consensus stands at $2.14 per share, representing a 30.49% increase from $1.64 in the prior year.

Mizuho raised its price target on Palo Alto Networks to $265 from $200 and kept its “Outperform” rating, pointing to healthy subscription and product revenue trends. The firm highlighted strength in Prisma SASE, XSIAM, and Prisma Browser, and said Q3 remaining performance obligation growth could come in above management’s 32% to 33% YOY outlook.

Barclays raised its target to $220 from $200 and kept an “Overweight” rating after seeing what it called strong organic checks going into earnings. BTIG lifted its target to $216 from $200 and maintained its “Buy” rating, backed by positive channel checks with partners and customers.

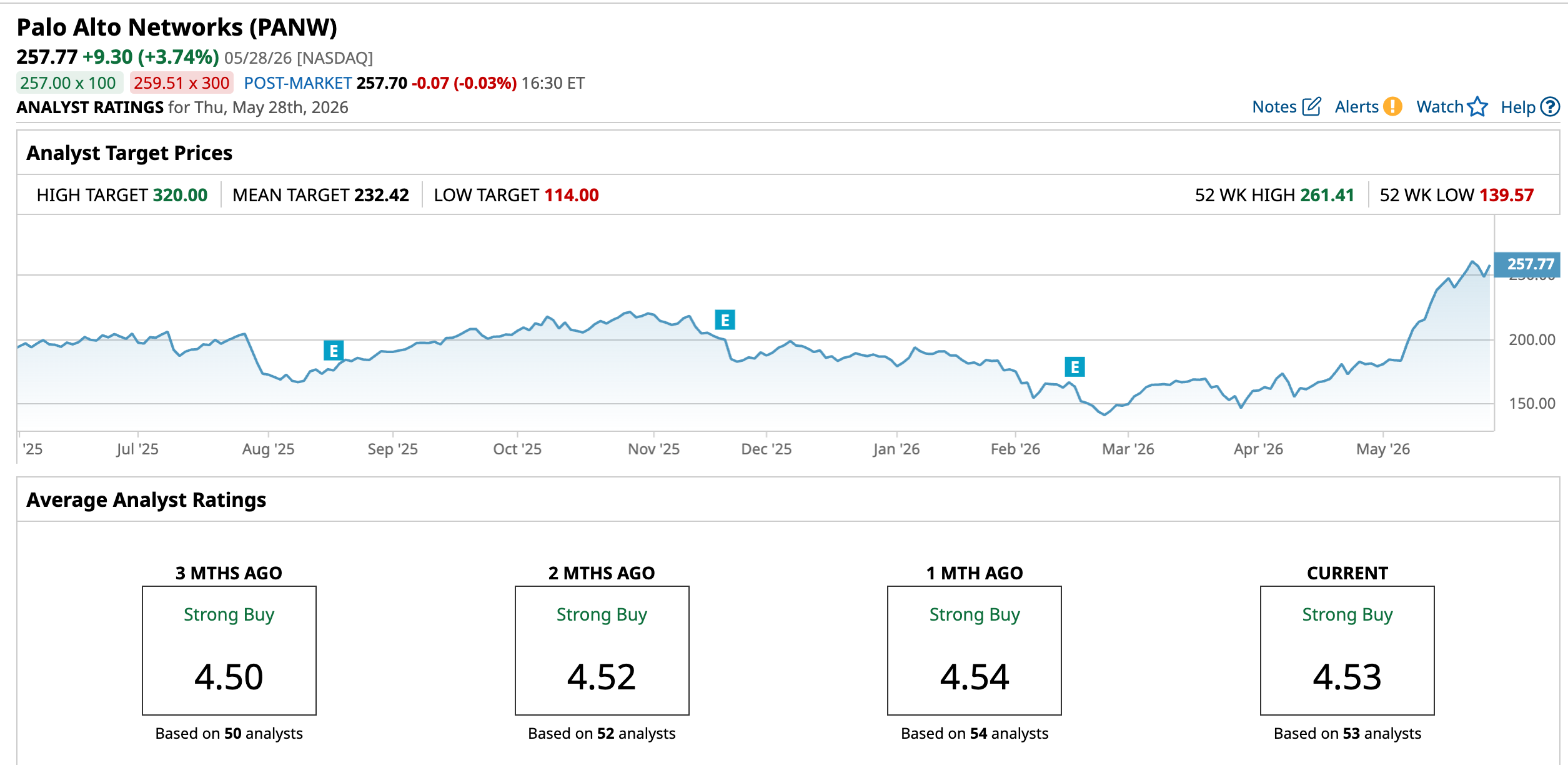

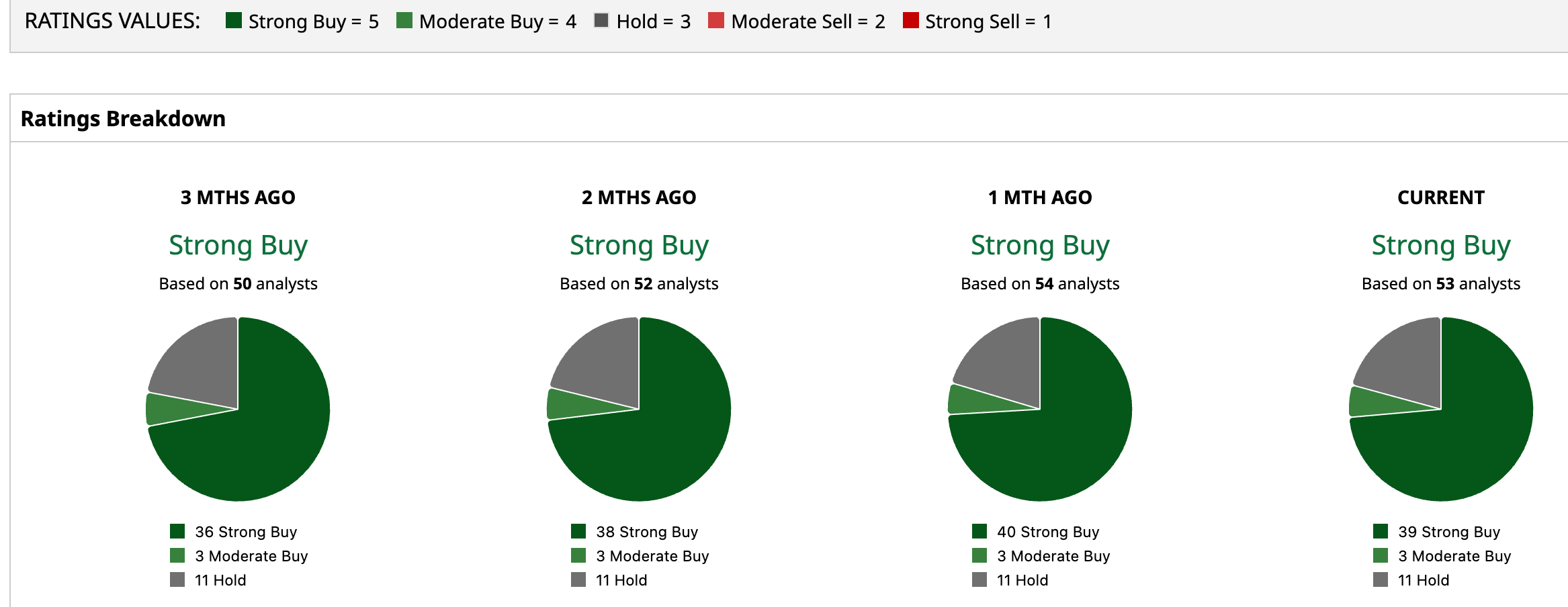

A consensus of 53 analysts surveyed rate Palo Alto Networks a “Strong Buy,” though the current price has well surpassed the mean price target of $232.42. And with the Street-high target of $320, PANW stock could realize 24.14% additional growth.

www.barchart.com

www.barchart.com www.barchart.com

www.barchart.comConclusion

Palo Alto looks like a stock where the bullish case is still intact, even after the big run. The AI-driven surge in cybersecurity demand is real, and Wedbush’s $325 target suggests the Street is starting to recalibrate higher as that demand translates into revenue, ARR, and platform adoption. While the valuation is undeniably stretched, the company’s growth trajectory and positioning in AI security make it hard to argue the story is fully priced in. From here, the most likely path appears skewed to the upside, especially if upcoming earnings confirm stronger-than-expected demand and execution.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Wedbush Just Set a New Street-High Price Target of $325 on Palo Alto Networks. What This Means for PANW Stock. Billionaire Mark Cuban Asks Why Insurance Companies Pay $2,500 for an MRI When ‘a Center Down the Street’ Only Charges $350 Dropbox Gets A New CEO. The Payoff for DBX Stock Could Take a Long Time. Micron Stock Is Trading at 42x Trailing Earnings. Analysts Say That’s Still Cheap.