Opendoor Technologies OPEN is pursuing profitability under its Opendoor 2.0 framework in a housing market still constrained by elevated mortgage rates, affordability pressure and high listings. During the first quarter of 2026, the company reiterated its expectation of reaching adjusted EBITDA profitability on a 12-month go-forward basis beginning in the second quarter and adjusted net income profitability by the end of 2026.

The profitability target is supported by improving operating metrics under Opendoor 2.0. OPEN entered into more than 5,000 signed acquisition contracts in the first quarter, its strongest quarterly contract volume since 2022. Resale contribution margin has improved every month since September 2025, while homes on the market for more than 120 days declined to 10% from 51% two quarters earlier.

The second-quarter outlook provides an important checkpoint for the profitability case. OPEN expects revenues to grow approximately 25% sequentially, with contribution margin in the middle of its 5-7% target range. The company also expects adjusted EBITDA to be around breakeven, plus or minus a few million dollars, keeping near-term execution central to the profitability outlook.

The company’s model remains sensitive to holding periods, pricing accuracy and home-price exposure. A fresher inventory base and faster resale cadence can lower carrying costs, reduce market risk and support stronger unit economics in a weak transaction environment.

OPEN’s ability to generate EBITDA progress in a weak housing market will likely depend on whether Opendoor 2.0 can sustain higher contract conversion, faster resale velocity and fresher inventory as volumes scale. These factors can support contribution margin and operating leverage, making disciplined growth central to the company’s path through a difficult housing market.

Opendoor’s Competitor Landscape

Zillow Group, Inc. ZG provides a relevant benchmark for OPEN because it is using product integration and platform depth to support growth despite a weak housing backdrop without taking direct inventory risk. Zillow is expanding its integrated housing experience across search, touring, financing, agent collaboration and closing. Its recent and upcoming initiatives include the broader rollout of AI Mode, Zillow Pro, Preview listings and continued expansion of Zillow Home Loans’ affordability tools. These efforts are aimed at improving buyer engagement, agent productivity and transaction conversion as broader housing activity remains pressured.

Offerpad Solutions Inc. OPAD provides a closer operating comparison because it remains exposed to home-selling execution, capital deployment and transaction conversion. To navigate the weak market, Offerpad is expanding its multi-solution platform across Cash Offer, Cash Offer Marketplace, Brokerage Services and Renovate. The company is also using SCOUT and HENRY to improve seller routing, acquisition precision, renovation estimates and disposition decisions. Its focus is on increasing conversion while preserving capital discipline, with management targeting roughly 1,000 transactions per quarter as the path to adjusted EBITDA breakeven.

Against this backdrop, OPEN’s positioning depends on whether Opendoor 2.0 can translate operating improvements into EBITDA progress as volumes scale. Zillow is leaning on a broader, capital-light platform to capture housing demand, while Offerpad is expanding seller-solution pathways and AI-enabled execution to improve conversion. OPEN’s differentiation will depend on how effectively it converts its larger contract funnel into profitable resale activity in a difficult housing market.

OPEN’s Stock Price Performance, Valuation & Estimates

Shares of Opendoor have skyrocketed 744.5% in the past year against the industry’s 9% decline.

OPEN One-Year Price Performance

Image Source: Zacks Investment Research

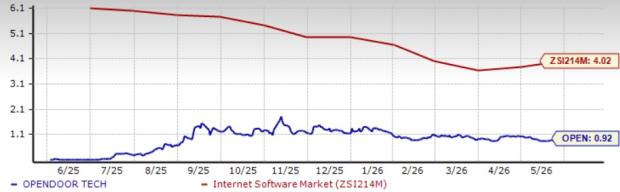

From a valuation standpoint, OPEN trades at a forward price-to-sales (P/S) multiple of 0.92, significantly below the industry’s average of 4.02.

OPEN’s P/S Ratio (Forward 12-Month) vs. Industry

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for OPEN’s 2026 earnings implies a year-over-year uptick of 61.5%. Loss per share estimates for 2026 have narrowed in the past 30 days.

EPS Trend of OPEN Stock

Image Source: Zacks Investment Research

OPEN stock currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Opendoor Technologies Inc. (OPEN): Free Stock Analysis Report

Zillow Group, Inc. (ZG): Free Stock Analysis Report

Offerpad Solutions Inc. (OPAD): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).