Climate change has been a major concern across the world. The demand for cleaner fuel has been mounting, signifying the global effort to gradually transition to a low-carbon economy. Hence, with fewer harmful pollutants and fewer environmental risks during transport, natural gas has already been in the spotlight.

Being a leading midstream energy company, Kinder Morgan KMI is well-positioned to benefit from the increasing demand for natural gas both in the United States and worldwide. LNG export is rising in the United States, and with KMI being responsible for transporting roughly 40% of all the gas to the liquefaction terminals, the company’s outlook seems bright.

Investors should also note that KMI, on its first-quarter 2026 earnings call, expressed expectations that U.S. natural gas demand would surge, driven by rising electricity demand from data centers. Kinder Morgan expects the demand to jump 27% to 150 billion cubic feet per day by 2031 from this year's level.

WMB & AR Also in the Spotlight

Williams WMB and Antero Resources AR are also well-poised to capitalize on rising demand for natural gas. Let’s delve deeper to find the reasons driving the two energy stocks.

WMB is a leading midstream energy player and is well-positioned to capitalize on clean energy demand. This is because, with its pipeline network spanning 33,000 miles, WMB is responsible for transporting significant volumes of natural gas produced in the United States.

Antero Resources is primarily a natural gas explorer and producer, having a solid footprint in the prolific Appalachian play. AR has sufficient premium drilling inventories in the key resource, which can aid the upstream player to keep its drilling operations for more than two decades at the current pace.

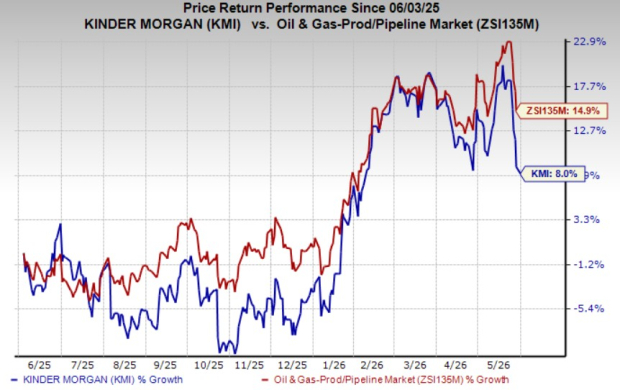

KMI’s Price Performance, Valuation & Estimates

Shares of KMI have gained 8% over the past year compared with the 14.9% improvement of the industry.

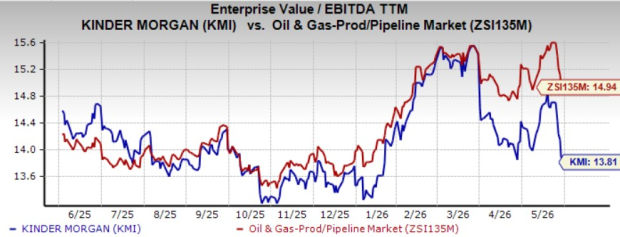

From a valuation standpoint, KMI trades at a trailing 12-month enterprise value to EBITDA of 13.81X. This is below the broader industry average of 14.94X.

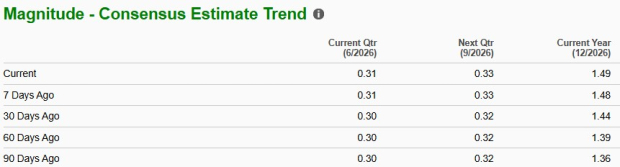

The Zacks Consensus Estimate for KMI’s 2026 earnings has seen upward revisions over the past seven days.

KMI currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Williams Companies, Inc. (The) (WMB): Free Stock Analysis Report

Kinder Morgan, Inc. (KMI): Free Stock Analysis Report

Antero Resources Corporation (AR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).