A common criticism of Dell Technologies (DELL) is that it is just a low-margin hardware assembler riding the AI wave. The company’s low to mid single-digit margins weren’t attractive for investors, and the general fear is that if the company relies on the same business again after helping build the AI infrastructure, it could give back all the AI gains. This fear isn’t justified in my view as the company’s business has transformed considerably. Looking at it from the lens of a law-margin business isn’t justified anymore, as the cash generation part of the business has massively changed for good.

Dell has a negative cash conversion cycle of 32 days. This means it collects cash from customers 32 days before it has to pay its vendors. Using this advantage, Dell set itself up perfectly for the AI infrastructure demand. For example, when DRAM prices surged, Dell repriced its entire server book and thousands of PC quotes in January. No other hardware vendor was able to move at this speed at such a scale. When combined with the negative cash conversion cycle and the supply chain advantage of their direct model, it gave Dell an operational moat that others like Hewlett Packard (HPE) and Lenovo (LNVGY) haven’t been able to replicate in their businesses. This is why looking at margins alone is a mistake. As an example, HPE is a margin leader at 13.4% EBITDA margin, while DELL only has 10.5%. However, where HPE earns almost zero return on capital, DELL does a great job with a return on capital of between 20% and 25%. This capital return is where investors need to look, rather than the margins.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

The inference and agentic AI wave then adds another dimension to how one should look at the business. Dell’s customer base isn’t just concentrated in hyperscalers. It has a diversified set of customers, which means it will be needed to deploy distributed inference systems when the time comes. Enterprises, government departments, and neoclouds will all provide business to Dell in that scenario. The $43 billion backlog and this future potential, where the management has already guided to an almost 100% YoY revenue growth, provide a better picture of where the company is headed. Yes, the stock is already up considerably this year, but the rally is only getting started because the market isn’t looking at Dell the right way.

About Dell Technologies Stock

Dell Technologies operates as a developer, designer, manufacturer, marketer, and seller of a wide range of technology products, solutions, and services. It operates in the Client Solutions Group (CSG) and Infrastructure Solutions Group (ISG) segments. The Infrastructure Solutions Group provides storage, servers, and networking solutions, while the Client Solutions Group offers laptops, PCs, desktops, and related accessories and services.

The stock delivered exceptional returns, more than tripling over the past year. This strong performance was largely driven by the sharp rally that started in early 2026 and gained momentum in the following months, especially in May. In comparison, the S&P 500 returned around 28% during the same period. Supported by its recent surge, the stock also outperformed the broader market on a year-to-date basis.

www.barchart.com

www.barchart.comOn all valuation metrics, DELL stock is expensive. Here again, even a forward-looking approach requires further investigation. The earnings growth of around 30% over the next two years justifies a forward P/E of 27x, though it leaves little room for a misstep owing to the market’s perception of Dell’s margins. The forward EV/EBITDA is 14x, which compresses sharply once earnings deliver. We saw this with Micron and SanDisk in the recent past, where the market waited some time before re-rating the stocks. Dell could be at a similar juncture right now.

Dell Technologies Posts Incredible Earnings Growth

The company released its first-quarter fiscal 2027 earnings report on May 29, immediately causing the stock price to surge nearly 40%. Revenue for the quarter came in at $43.8 billion while diluted EPS grew 214% to $4.86. The company generated $4.1 billion in operating cash flows. During the quarter, it returned $2.1 billion to shareholders through dividends and share buybacks. For segments, ISG delivered record revenue of $29 billion, and CSG revenue came in at $14.6 billion.

Going forward, the company guided second-quarter revenue in the range between $44 billion and $45 billion. Diluted non-GAAP EPS is estimated at $4.80, with a possible variation of $0.10. The company expects ISG revenue to grow about 75%, benefiting from strong demand for AI servers, while CSG revenue is projected to grow by around 20%. Full year 2027 revenue is forecasted to range from $165 billion to $169 billion.

What Analysts Are Saying About Dell Technologies Stock

Following its earnings report, analyst sentiment turned positive on Dell Technologies. On June 1, Barclays raised its price target on the stock from $168 to $550 while assigning a “Buy” rating. On the same day, Morgan Stanley upgraded Dell from “Underweight” to “Equal Weight.” The firm also raised its price target on the shares from $170 to $448. These significant upward revisions in the price targets signal growth potential.

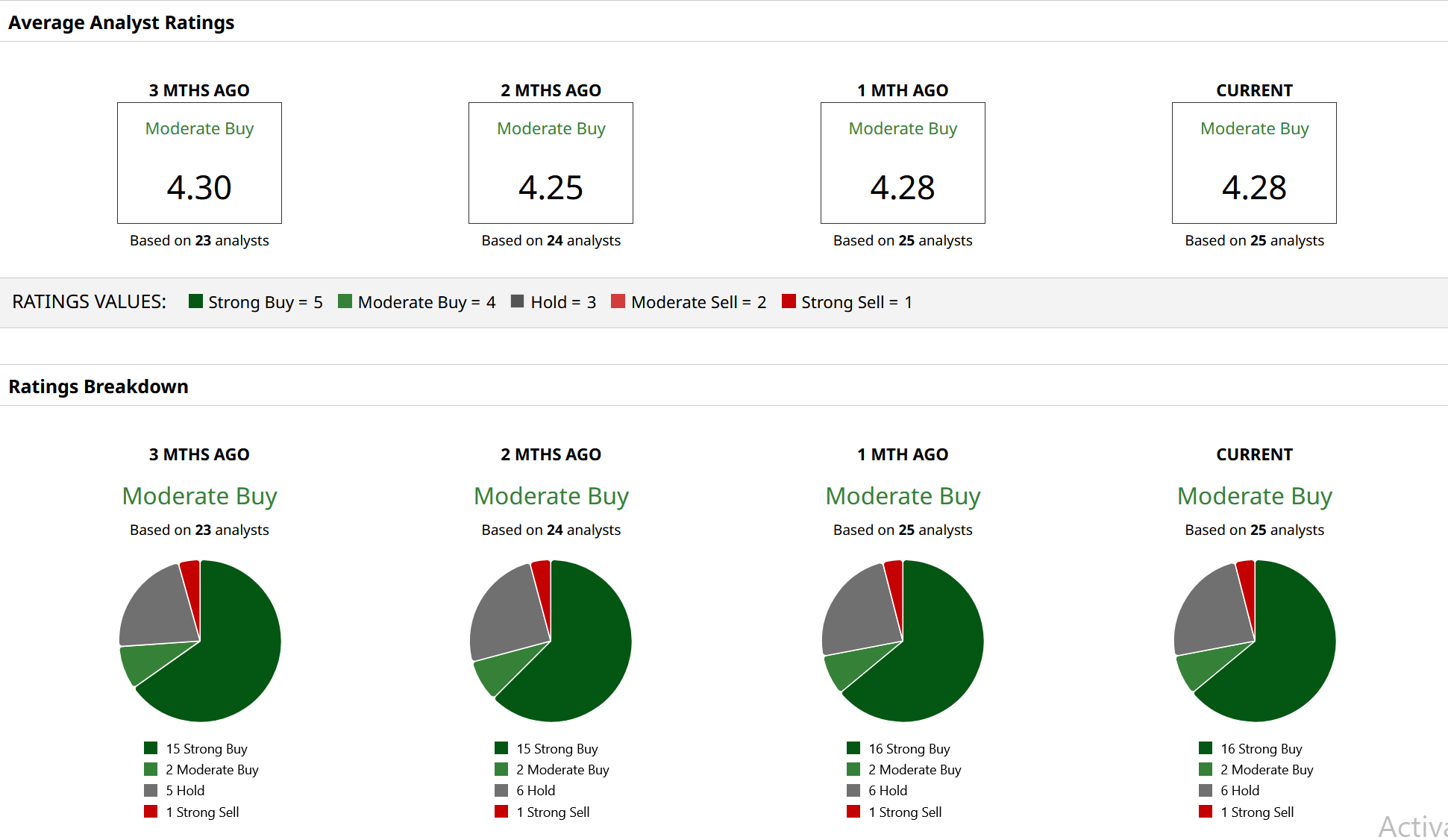

According to 25 Wall Street analysts covering the stock, it has a consensus “Moderate Buy” rating. Based on their estimates, it has an average price target of $442.71, which the stock has already reached, and a high price of $700, which is a nearly 61% upside from recent levels.

www.barchart.com

www.barchart.com On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Texas Instruments Is a Major Winner of the AI Power Bottleneck, Investors Just Aren’t Seeing It Yet Dell’s Bull Rally Will Continue. Don’t Fall Into the Trap of Thinking It’s Just a Low-Margin Hardware Assembler. A $2 Billion Reason to Buy Little-Known Gorilla Technology Stock Right Now Cadence Design Is Cementing Its Place in the 2nm AI Chip Race By Solving the Die Size Limit in Partnership With a Major Chipmaker