For much of the past two years, Bitcoin (BTCUSD) seemed unstoppable. Every dip found buyers, spot ETFs opened the door for institutional money, and crypto bulls talked openly about a new era of mainstream adoption. But lately, that story has hit a rough patch.

Bitcoin has tumbled 27.26% so far this year, sliding below the $60,000 level and suffering one of its sharpest corrections in recent memory. Several forces have converged at once. Institutional investors have been pulling money from spot Bitcoin ETFs for weeks, removing a key source of demand that helped fuel the cryptocurrency’s historic rally. Confidence also took a hit after Strategy (MSTR), Michael Saylor’s company and one of Bitcoin’s most vocal corporate supporters, sold a portion of its holdings, unsettling a market already showing signs of fatigue.

Join 200K+ Subscribers: Find out why the midday Barchart Brief newsletter is a must-read for thousands daily.

Meanwhile, regulatory uncertainty continues to hang over the sector as lawmakers struggle to advance the CLARITY Act, leaving investors with few answers about the future rules of the game. Adding in a massive derivatives wipeout that erased roughly $1.8 billion in crypto positions in a single day, the selling pressure quickly snowballed. At the same time, investors chasing the next big growth story have increasingly shifted capital toward artificial intelligence (AI) and technology stocks, leaving crypto fighting for attention.

That backdrop is starting to worry Wall Street’s Coinbase Global (COIN) watchers. Baird recently turned more cautious on Coinbase, naming the stock a ‘Bearish Fresh Pick’ and cutting its price target. The brokerage firm believes softer crypto trading activity could translate into weaker-than-expected Q2 results, while Coinbase’s premium valuation leaves little room for disappointment. With trading volumes cooling, regulatory clarity still elusive, investor enthusiasm fading, and COIN stock slipping, some analysts are wondering whether Coinbase can justify its lofty multiple if the crypto slowdown persists.

About Coinbase Global Stock

Founded in 2012, Coinbase has grown from a simple cryptocurrency trading platform into one of the most influential companies in digital finance. With a market capitalization of $40.2 billion, the company serves millions of retail and institutional customers worldwide. Beyond buying and selling crypto, Coinbase has been expanding into stablecoin payments, crypto-backed cards, subscriptions, derivatives, and blockchain infrastructure, positioning itself as a key player in the next chapter of the digital asset economy.

But if there’s one thing investors have learned about Coinbase, it’s that the stock tends to move with the mood of the crypto market. When Bitcoin is flying, Coinbase often looks unstoppable. When crypto sentiment turns sour, the stock can fall just as quickly.

That pattern has been on full display over the past year. Earlier in the summer, as Bitcoin rallied and enthusiasm returned to digital assets, Coinbase’s shares surged to a high of $444.64 in July. Investors piled in, betting that higher crypto prices would translate into stronger trading activity and fatter profits. For a while, that thesis worked.

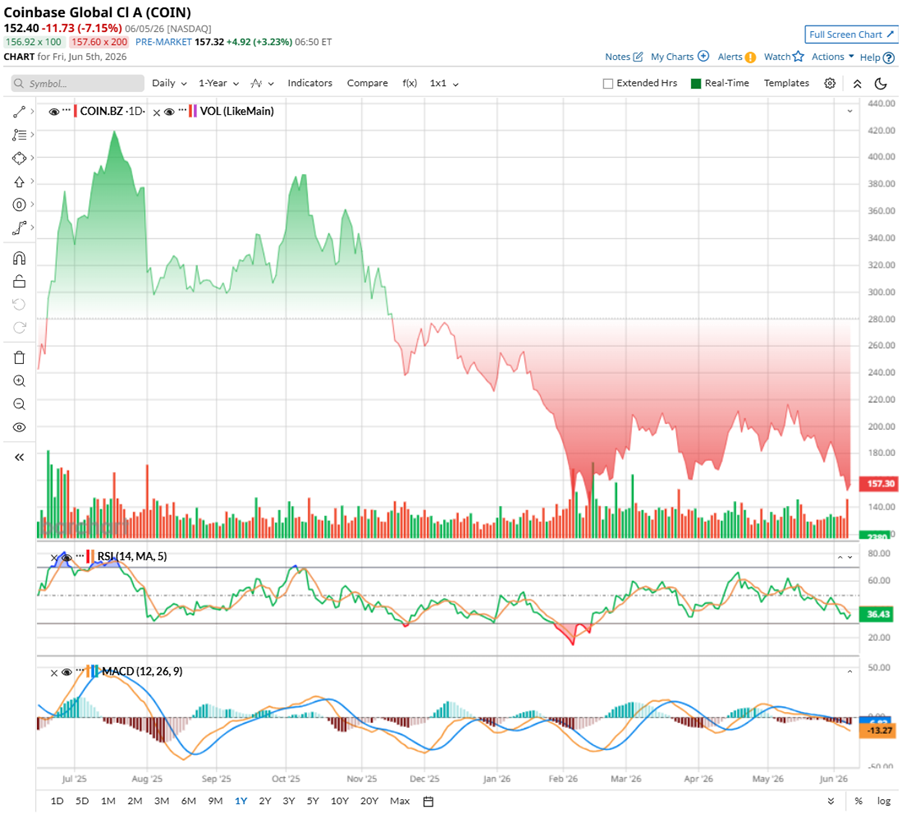

Then the market’s mood shifted. BTC lost momentum, trading volumes cooled, and concerns about regulation and investor demand crept back into the conversation. As crypto prices retreated, COIN followed. Shares of the cryptocurrency exchange operator have now surrendered much of their earlier gains and sit roughly 65.7% below the peak.

The recent selling has been particularly intense, with shares falling 41% over the past six months and another 18% in the last three months alone. Over the past month, the stock has dropped 19.6%, including a sharp 11.5% decline in just the last five trading sessions.

The latest leg lower came after Baird turned more cautious on the company, warning that softer trading activity could weigh on upcoming results and trimming its price target on COIN stock.

The technical picture is not offering much comfort either. Selling volume has picked up during the latest decline, suggesting investors have been heading for the exits rather than stepping in to buy the dip. The 14-day RSI has retreated to 39.18, after hovering near the overbought territory in April, signaling that momentum has cooled considerably.

Meanwhile, the MACD line has also moved into negative territory, and the line now sits below the signal line, with the histogram remaining negative since early May – signs that bearish sentiment continues to dominate the stock’s near-term trend.

www.barchart.com

www.barchart.com Despite the recent selloff, COIN is not exactly trading at bargain-bin levels. Investors are still assigning a hefty premium to the stock, with COIN priced at roughly 125 times forward adjusted earnings, well above both sector average and its own historical median. Its 6.52 times price-to-sales multiple also remains richer than most industry peers, though it sits slightly below the company’s own five-year average. In other words, the market is still pricing in plenty of future growth, even as questions around crypto demand continue to swirl.

Coinbase Reports Mixed Q1 Results

Coinbase’s first-quarter numbers, released on May 7, were a mixed bag. On the surface, the numbers looked disappointing. Revenue came in at $1.4 billion, down 31% year-over-year (YOY) and below Wall Street’s expectations as the crypto market cooled. Trading activity slowed across the industry, with transaction revenue declining 40% annually and falling 23% sequentially to $756 million. Consumer transaction revenue decreased to $567 million, while institutional transaction revenue dropped to $136 million. Spot trading volumes on the platform slid 35% as Bitcoin and Ethereum (ETHUSD) pulled back during the quarter. The company also posted an adjusted net loss of $45.6 million.

But digging deeper reveals a more nuanced story. Coinbase generated $303 million in adjusted EBITDA, extending its streak of positive adjusted EBITDA quarters to 13 in a row. More importantly, the weakness appeared tied to a softer crypto market rather than a loss of competitive position. Total crypto market cap and industry trading volumes both fell over 20% during Q1, yet Coinbase actually captured a record 8.6% share of crypto trading volume, marking its 12th straight quarter of net native asset inflows.

Beyond trading, Coinbase continued expanding its broader crypto ecosystem. Derivatives trading volume surged 169% YOY, prediction markets scaled rapidly after their U.S. launch, and the company’s Base blockchain emerged as a major player in AI-driven on-chain activity. More than 90% of agentic transaction volume during the quarter occurred on Base, with USDC facilitating nearly all of those transactions, highlighting Coinbase's growing role in the infrastructure layer of the crypto economy.

Looking ahead, Coinbase is trying to strike a balance between growth and efficiency. Management expects second-quarter subscription and services revenue to come in between $565 million and $645 million. While spending remains substantial, the company is beginning to tighten its belt. Coinbase forecasts technology and administrative expenses of $820 million to $870 million, down from $902 million in Q1.

A major driver is a restructuring effort that will eliminate roughly 700 positions as the company leans more heavily on AI-powered automation. The move is expected to generate about $500 million in annual savings, although Coinbase will first absorb $50 million to $60 million in restructuring charges tied to the workforce reduction.

Analysts monitoring Coinbase expect the company’s EPS to be around $0.39 in Q2, with revenue anticipated to slip to about $1.35 billion. Looking ahead, adjusted EPS for fiscal 2026 is projected to be around $1.77, down 56.1% YOY. But the tide could turn quickly by the next fiscal year. Adjusted EPS is anticipated to surge 170.6% annually to $4.79 in fiscal 2027.

What Do Analysts Expect for Coinbase Stock?

Baird analyst David Koning believes COIN stock may be heading into a tougher stretch than investors currently expect. The brokerage firm recently designated COIN as a ‘Bearish Fresh Pick’ and lowered its price target to $142 from $160, arguing that slowing crypto activity could weigh on near-term results.

According to Koning, Q2 revenue could come in roughly 5% to 6% below Wall Street’s expectations as trading volumes appear to have cooled significantly. He estimates volume growth may decline 15% to 20% sequentially, noting that April and May were among the slowest months for crypto trading in recent years. While activity picked up somewhat in early June, Baird believes that the surge may have been driven largely by investors selling Bitcoin during the market downturn rather than a lasting increase in trading demand.

The brokerage firm is also concerned about COIN’s valuation. Even after the recent pullback, the stock trades at a sizable premium, and Baird warns that weaker earnings estimates, delayed crypto regulation, and growing competition from traditional financial players could put further pressure on the shares.

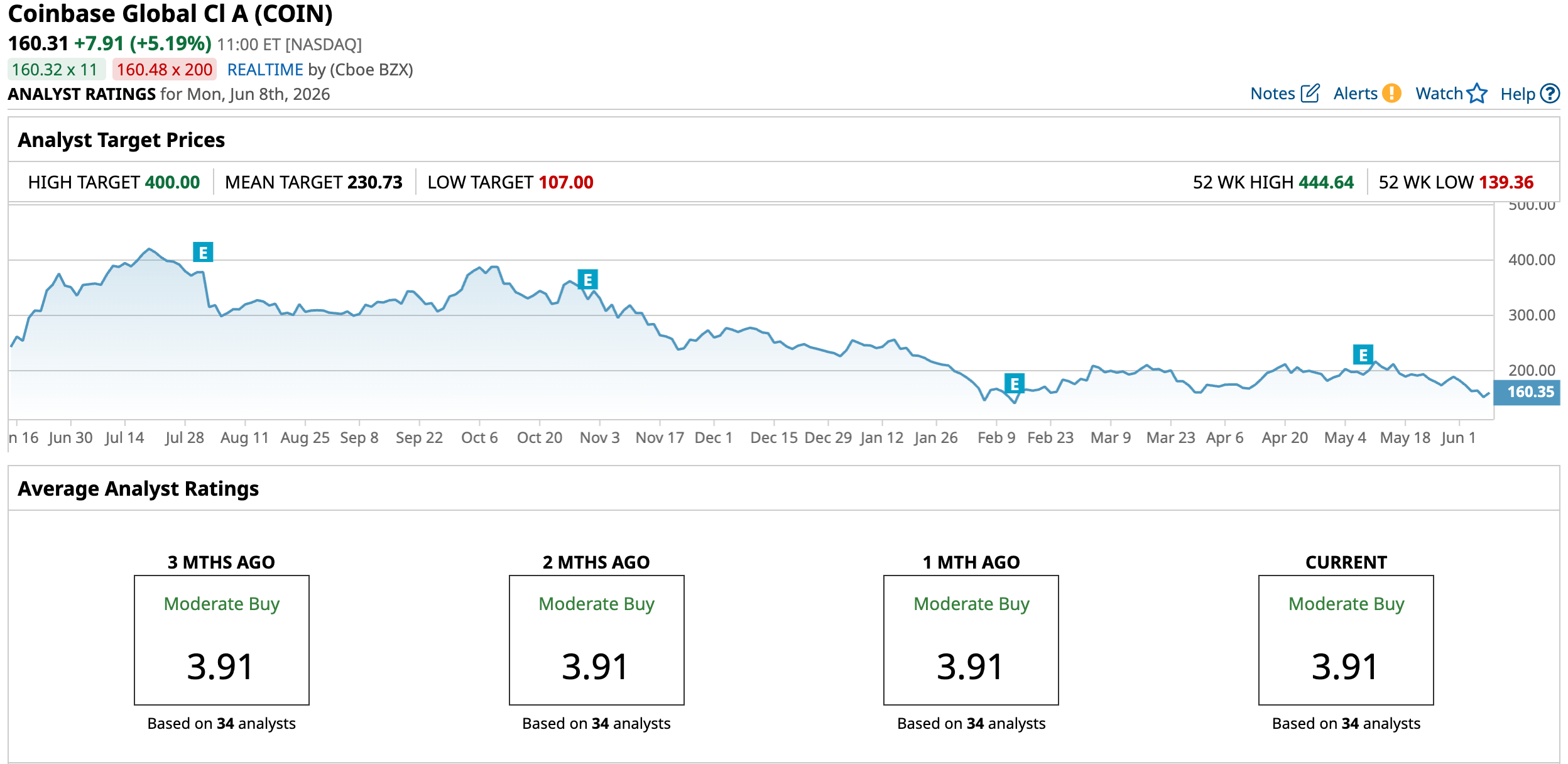

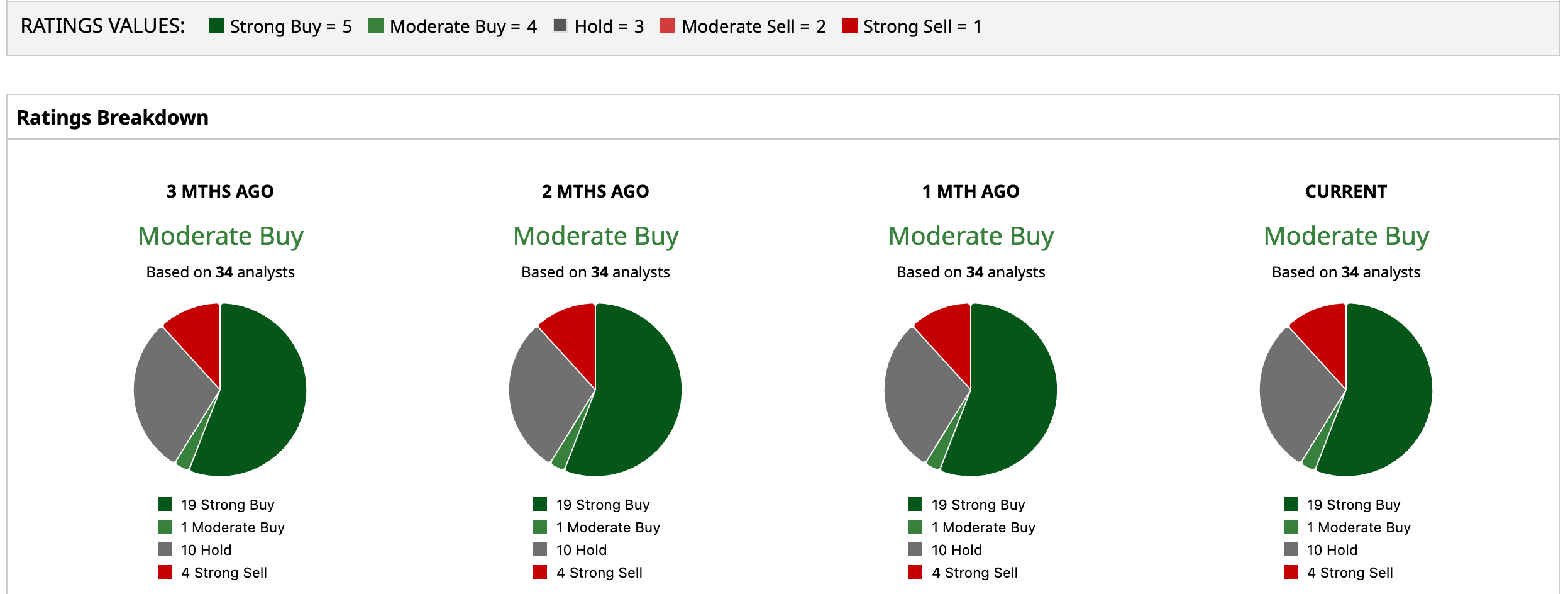

Overall, the stock has a “Moderate Buy” consensus rating. Out of 34 analysts, 19 now rate it a “Strong Buy,” one calls it a “Moderate Buy.” 10 analysts are playing it safe with a “Hold,” and the remaining four are outright bearish with a “Strong Sell” rating.

Wall Street has not completely given up on COIN. Analysts still see a path back toward the stock’s former highs, with the mean price target of $230.73 implying 43.9% upside from current levels. And for the biggest bulls on the Street, the opportunity looks even larger, with the most optimistic target of $400 now suggesting COIN could more than double, climbing roughly 149.5% from here.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com Final Thoughts on COIN Stock

So, is Wall Street right to be losing faith in Coinbase? The answer is not as straightforward as the recent selloff might suggest. The bearish case is easy to see. BTC remains under pressure, trading activity has slowed sharply, regulatory clarity is still nowhere in sight, and Coinbase continues to trade at a valuation that assumes much brighter days ahead. If crypto enthusiasm stays muted, Baird’s concerns about weaker revenue, lower earnings estimates, and multiple compression could prove justified.

But the bullish case has not disappeared. Despite the difficult market backdrop, Coinbase continues to gain trading market share, attract customer assets, and expand into businesses that are less dependent on day-to-day crypto trading. The company’s growth in derivatives, prediction markets, stablecoins, and blockchain infrastructure suggests it is building a broader financial ecosystem rather than relying solely on transaction fees.

The biggest wildcard remains Bitcoin itself. History has shown that crypto sentiment can change quickly. In fact, after a brutal week of selling, Bitcoin has already bounced back above $63,000 as a wave of short-covering swept through the market. Coinbase’s shares have responded positively in pre-market trading as well.

For now, investors appear caught between a weakening crypto cycle that could pressure results in the near term and a company that is still strengthening its competitive position for the long haul. The next few quarters will likely determine which story wins. Until then, COIN remains a stock with significant upside potential, but one that still comes with plenty of volatility and risk attached.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

As Bitcoin Prices Plunge, Wall Street Is Losing Faith in Coinbase Stock Rumble Shakes Up the Cloud Space with Massive Blackwell Commitment MSTR Stock Alert: Strategy Plummets as Bitcoin Sinks Below $60K Circle Stock Slips as Stripe, Visa, Mastercard Explore Stablecoin Platform