Nvidia (NVDA) stock is undervalued despite the company leading the artificial intelligence (AI) hardware boom with its GPUs. While NVDA stock looks cheap, surging demand for its AI chips, next-generation product launches, and new growth opportunities indicate notable upside potential over the next 12 months.

For investors looking to capitalize on the AI megatrend, Nvidia still looks compelling near the current levels and offers an attractive entry point. As AI continues to drive the broader market and investor capital remains concentrated in a handful of industry leaders, Nvidia is one of the top companies positioned to deliver solid growth.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.com Nvidia’s AI Engine Keeps Roaring

Nvidia remains a leader in AI infrastructure. Moreover, its recent quarterly financial results show that demand for AI infrastructure remains exceptionally strong, with hyperscale cloud providers and developers of advanced AI models aggressively increasing their capital expenditures, and Nvidia capturing a significant share of that spending.

For instance, Nvidia generated $82 billion in revenue in the first quarter of fiscal 2027, representing an 85% year-over-year (YoY) increase. Notably, its growth rate accelerated in Q1, and Nvidia added $13.5 billion in sequential revenue, exceeding the total quarterly revenue of its peers.

Nvidia’s growth is supported by solid ongoing strength in the data center segment, which generated $75 billion in revenue, up 92% YoY and 21% sequentially. Management attributed much of the momentum to strong adoption of its Blackwell architecture. Within the segment, Nvidia’s computing revenue was $60 billion, while networking revenue surged to $15 billion, nearly tripling from the prior year.

The rapid growth in networking is important for investment purposes. It highlights Nvidia’s success in capturing a larger share of AI infrastructure spending. By offering integrated solutions that combine processors, networking technologies, software, and system architecture, Nvidia is strengthening its competitive position while increasing its addressable market.

Another emerging growth driver is Nvidia’s expansion into CPUs. As the AI industry moves beyond model training and toward inference workloads and autonomous AI agents, demand for high-performance CPUs is expected to rise. Nvidia estimates the CPU market opportunity at roughly $200 billion and expects its CPU products to generate approximately $20 billion in revenue this year, while further diversifying revenue streams and strengthening Nvidia’s position in AI data centers.

The strategic benefits of CPU adoption extend beyond direct revenue growth. Integrated CPU and GPU platforms deepen Nvidia’s presence within customer infrastructure, increase switching costs, and make its ecosystem more difficult to replace. This creates opportunities for Nvidia to monetize multiple layers of AI deployment, spanning model training, inference, networking, and future agentic AI applications.

NVDA Stock Still Offers 46% Upside Potential

Nvidia continues to dominate the AI infrastructure market, and its next-generation Blackwell and Rubin platforms will enable it to sustain solid growth momentum. Management estimates that Blackwell and Rubin-related products could generate up to $1 trillion in revenue between 2025 and 2027. If adoption of Nvidia's expanding CPU portfolio accelerates alongside this roadmap, the company's revenue opportunity could grow even larger than current expectations.

Adding to NVDA’s appeal is its compelling valuation relative to its solid earnings growth potential. The stock trades at 25.4 times forward earnings, while analysts forecast earnings growth of more than 88% in fiscal 2027, followed by another 34% increase in fiscal 2028.

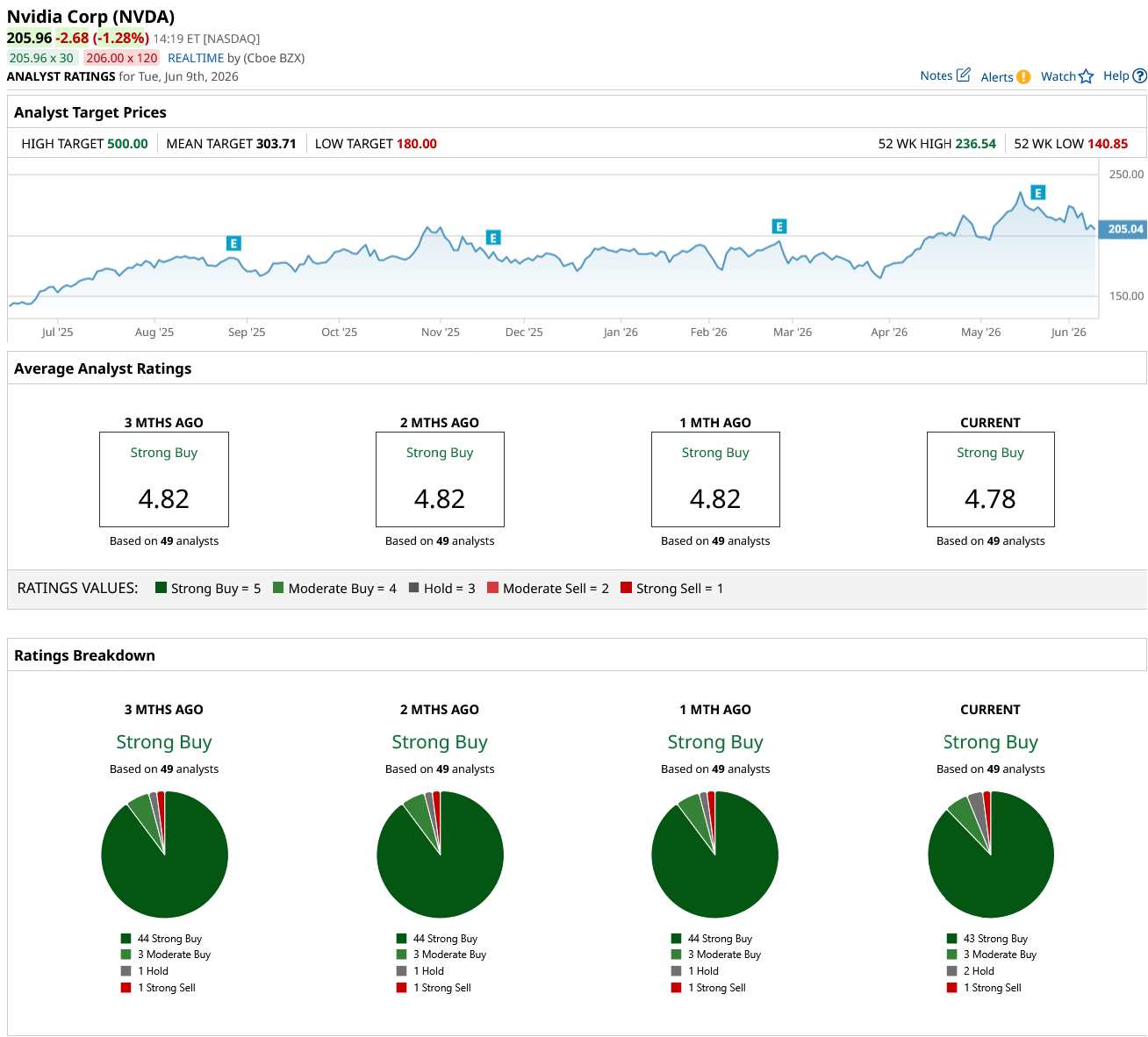

Wall Street is bullish, and Nvidia currently carries a consensus "Strong Buy" rating. Further, the average analyst price target of $303.71 implies about 46% upside from its recent closing price of $208.64. In addition, the highest price target for NVDA is $500, suggesting a potential upside of about 140%.

www.barchart.com

www.barchart.com On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Why Cathie Wood Seemingly Can’t Get Enough of Kratos Defense Stock Nvidia Stock Looks Undervalued. Why Buying Now Could Offer 46% Upside Potential. Oracle Stock Is Careening Toward Earnings with a Heavy $100 Billion Weight on Its Back Wedbush Thinks Cerebras Stock Is Ready for More Upside as CBRS Debuted at Just the Right Time