Nuclear stocks are getting attention again, driven by a flurry of announcements around new reactor deals, including Brookfield Asset Management (BAM) teaming up with The Nuclear Company to roll out Westinghouse AP1000 and AP300 reactors, while Blue Energy (BUENF) works with GE Vernova (GEV) on a hybrid gas and nuclear design. At the same time, a recent Gallup poll shows record U.S. support for nuclear power, pointing to a shift where policy support and demand are starting to turn into actual projects, not just talk.

Oklo (OKLO) has been riding that momentum. Earlier this year, it secured a long-term power deal with Meta Platforms (META), which gave its small modular reactor model a real vote of confidence and pushed the stock higher. Then on June 4, 2026, Oklo said it had closed its acquisition of ARMEC, a precision manufacturing firm focused on high-tolerance nuclear components.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

The market reacted, OKLO rising 3.96% on the day of the announcement. But for a company still burning cash and without commercial revenue, does owning a manufacturing business actually speed up reactor deployment, or is this just another step that sounds good but takes time to pay off?

Inside Oklo’s Financial Picture

Oklo is an advanced nuclear company building small, fast reactors and its own fuel supply, to deliver steady, clean power from a vertically integrated setup that covers design, fuel fabrication, and recycling. Over the past 12 months, the stock is up 4.09%, but year-to-date (YTD), it’s down 21.29%.

www.barchart.com

www.barchart.comOn the balance sheet, Oklo ended the last quarter with $2.5 billion in cash and marketable securities, split between $1.6 billion in cash and $900 million in securities, helped by $1.2 billion raised through an at-the-market equity program. But the company is still losing money as it builds out. Net loss was $33.1 million, driven by a $51.2 million operating loss and $3.2 million in taxes, partly offset by $21.3 million in interest and dividend income.

Cash use tells the same story, with $17.9 million used in operating activities after adjusting for $15.6 million in stock-based compensation, and $359 million flowing into investing, mostly to buy marketable securities. Capital spending came in at $32.8 million as Oklo pushed projects across its main business lines. For 2026, management is guiding to $80 million–$100 million in operating cash burn and $350 million–$450 million in capex, underlining how much they’re still in build mode.

The Growth Case Behind ARMEC

The ARMEC acquisition is a straightforward way for Oklo to pull more of the hard engineering work inside the company. ARMEC is based in Tennessee and brings more than 20 years of experience, a roughly 40-person technical team, and hands-on skills in high-precision machining, prototyping, fabrication, inspection, and engineering.

The key benefit is the tighter loop between design and manufacturing, so Oklo can move from early test hardware to repeatable production. ARMEC is already helping with nozzle manufacturing through better drawings, inspection planning, and supplier troubleshooting, which shows up as real operational progress, not just a long-term promise.

That extra control also ties into Oklo’s fuel plans. The company was picked by the U.S. Department of Energy for advanced talks on a program to turn surplus Cold War-era plutonium into fuel for advanced reactors. If that moves ahead, it gives Oklo another potential domestic fuel source at a time when enrichment capacity is tight, and it fits with its recycling-focused approach. Working with nuclear energy company Newcleo, Oklo is pairing that strategy with plans for up to $2 billion in fuel fabrication investment.

Oklo is also trying to speed up its design cycle by leaning into AI. The company announced a Strategic Partnership Project with Battelle Energy Alliance, which runs Idaho National Laboratory, to use AI tools to accelerate advanced reactor and fuel-system design work. The National Nuclear Security Administration-backed project gives Oklo access to specialized lab expertise and facilities to support conceptual design for one of its reactor systems using AI-enabled engineering workflows, modeling, simulation, and documentation.

Under the partnership, Oklo and INL will link the Prometheus AI platform with Oklo’s own Multiphysics design and analysis stack to streamline engineering work and push forward Pluto, Oklo’s plutonium-fueled reactor that sits inside the DOE’s Reactor Pilot Program.

Analyst Sentiment and Near-Term Outlook

The next earnings release for Oklo is set for August 10, 2026. For the June 2026 quarter, analysts are looking for a loss of $0.19 per share, a touch worse than the $0.18 loss a year ago, which works out to a 5.56% year-over-year (YOY) decline. The September 2026 quarter is pegged at a $0.20 loss, unchanged from last year, while full-year 2026 is modeled at a $0.78 loss versus $0.72 in 2025, an 8.33% drop.

Bank of America analyst Ross Fowler recently restarted coverage with a “Buy” rating and an $80 price target, calling Oklo an “early leader” in advanced nuclear. His case leans on the full-stack model, where Oklo owns, operates, and manages its reactors under long-term contracts instead of just selling equipment. He also highlighted the binding 1.2 GWe agreement with Meta Platforms and more than 14 GWe of additional projects under non-binding letters of intent as signs that demand is building faster than many investors think.

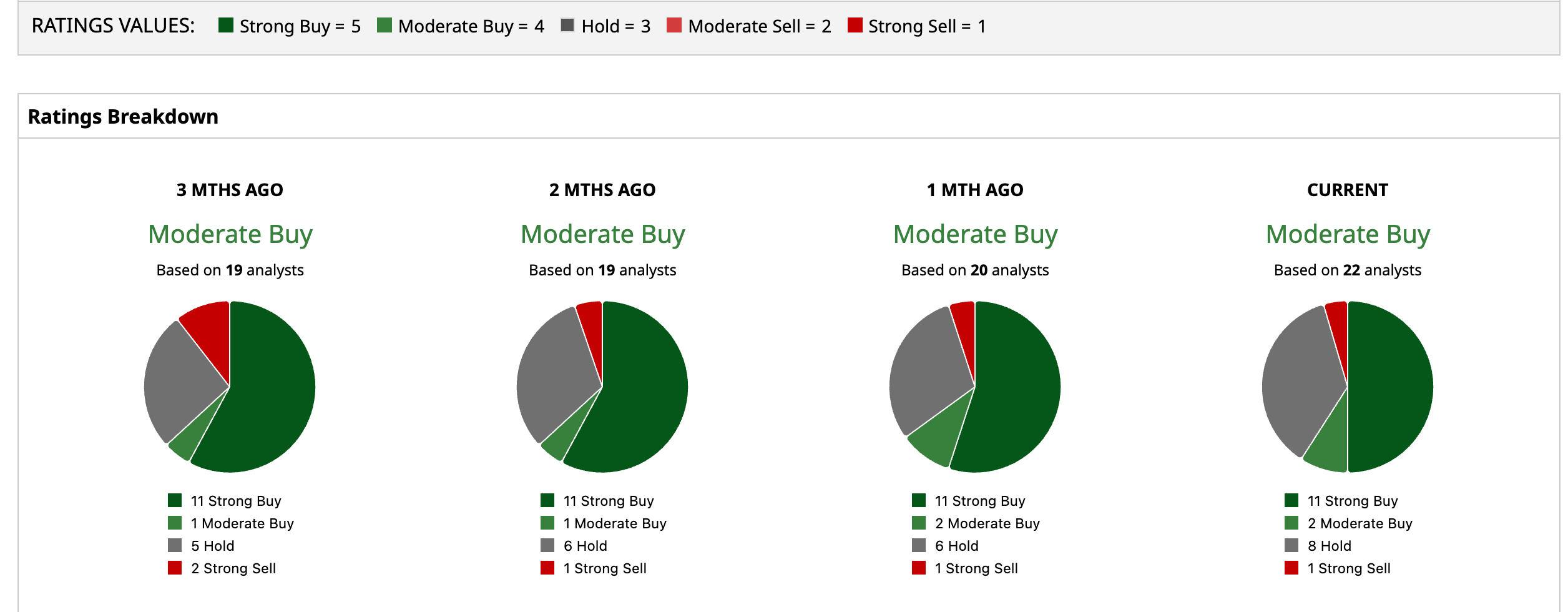

All 22 analysts covering Oklo have it rated at a consensus "Moderate Buy", with an average price target of $85.68. Off the current price levels, that points to 51.7% upside.

www.barchart.com

www.barchart.com www.barchart.com

www.barchart.comConclusion

This appears as a meaningful move for the stock, but mostly as a thesis-strengthening step rather than an immediate game changer. ARMEC gives Oklo tighter control over a critical part of reactor manufacturing, which fits neatly with its broader push to own more of the supply chain, secure fuel pathways, and move closer to deployment. That does not remove the core risks around execution, regulation, and cash burn, but it does make the story more credible. My base case is that shares are more likely to stay volatile in the near term, yet trend higher over time if Oklo keeps stacking operational milestones and avoids major delays.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Tapestry Stock Is Breaking Out: Why Shares Have at Least 10% More Upside Potential Wedbush Gives a Thumbs Up to Palantir’s AIPCon, But I Think AIPCon 2026 Was a Dud for PLTR Stock Intel Is Joining Hands With Hitachi to Bring Physical AI to Life. It Needs to Bring the INTC Stock Valuation Down, Too. Xpeng’s AI Progress Should Give XPEV Stock a Big Boost in the Long Term