Atlanta, Georgia-based Corpay, Inc. (CPAY) is a business-to-business (B2B) payment solutions company that specializes in helping corporations track, manage, and optimize their non-payroll expenses. Valued at a market cap of $23.6 billion, the company offers a comprehensive ecosystem of smart corporate payment tools designed to automate accounts payable workflows, minimize transaction friction, and eliminate manual processing errors.

Companies valued at $10 billion or more are typically classified as “large-cap stocks,” and CPAY fits the label perfectly, with its market cap exceeding this threshold, underscoring its size, influence, and dominance within the software - infrastructure industry. The company’s primary competitive strength lies in its proprietary, multi-rail global payment network and high-scale infrastructure, which enables it to operate as one of the largest non-bank commercial card issuers and B2B payment processors in North America.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

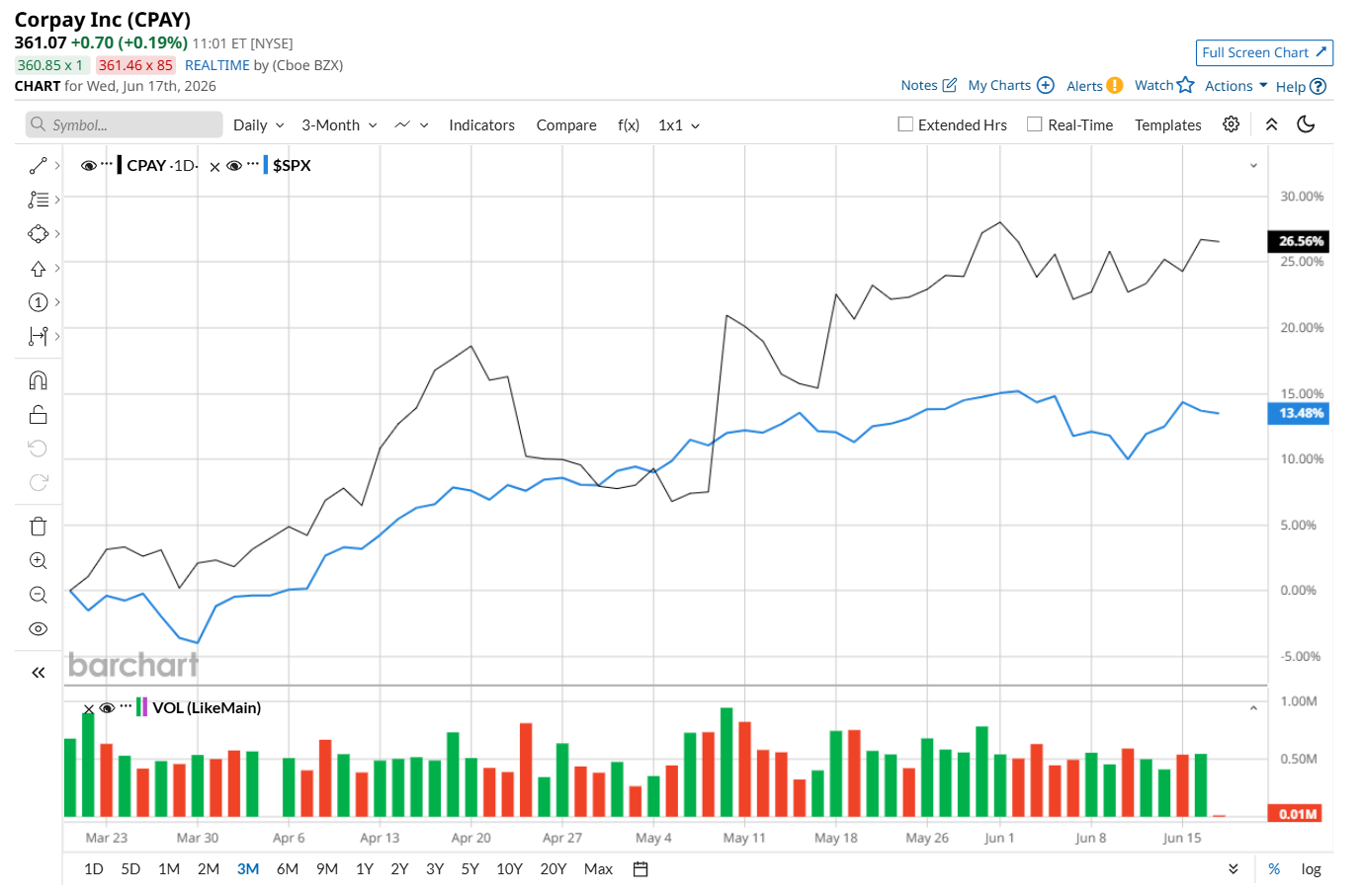

The company is currently trading 1.9% below its 52-week high of $367.43 reached recently on Jun. 1. Shares of CPAY have soared 16.2% over the past three months, considerably outperforming the S&P 500 Index’s ($SPX) 11.8% uptick during the same time frame.

www.barchart.com

www.barchart.com Moreover, on a YTD basis, shares of CPAY are up 19.8%, compared to SPX’s 9.7% rise. However, in the longer term, CPAY has gained 8.4% over the past 52 weeks, lagging SPX's 25.6% return over the same time period.

To confirm its recent bullish trend, CPAY has been trading above its 200-day and 50-day moving averages since early May.

www.barchart.com

www.barchart.com Shares of CPAY surged 12.5% after the company reported strong first-quarter 2026 results on May 7. Revenue increased 25% year-over-year to $1.26 billion, driven by robust organic revenue growth, marking the fourth consecutive quarter of double-digit organic expansion. Its adjusted EPS rose 29% from the year-ago quarter to $5.80, reflecting the company's continued earnings momentum. The positive sentiment was reinforced by management’s decision to raise its full-year 2026 outlook. Corpay now expects revenue of $5.25 billion to $5.33 billion and adjusted EPS of $26.30 to $27.10.

CPAY has also outpaced its rival, Global Payments Inc. (GPN), which dropped 8.7% over the past 52 weeks and 10.3% on a YTD basis.

Given CPAY’s recent outperformance, analysts remain moderately optimistic about its prospects. The stock has a consensus rating of “Moderate Buy” from the 16 analysts covering it, and the mean price target of $394.14 suggests a 9.1% premium to its current price levels.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Stantec Stock Just Hit a 52-Week Low — But Analysts Say It’s a Buy Why Citi Keeps Pounding the Table on Texas Instruments Stock AI Agents Are Changing Cybersecurity Forever. Zscaler Is Positioning Itself to Win Big. RTX Stock Has Carved Out a New Price Floor and Is Headed Higher. The Chart Says More Gains Are Likely in Store.