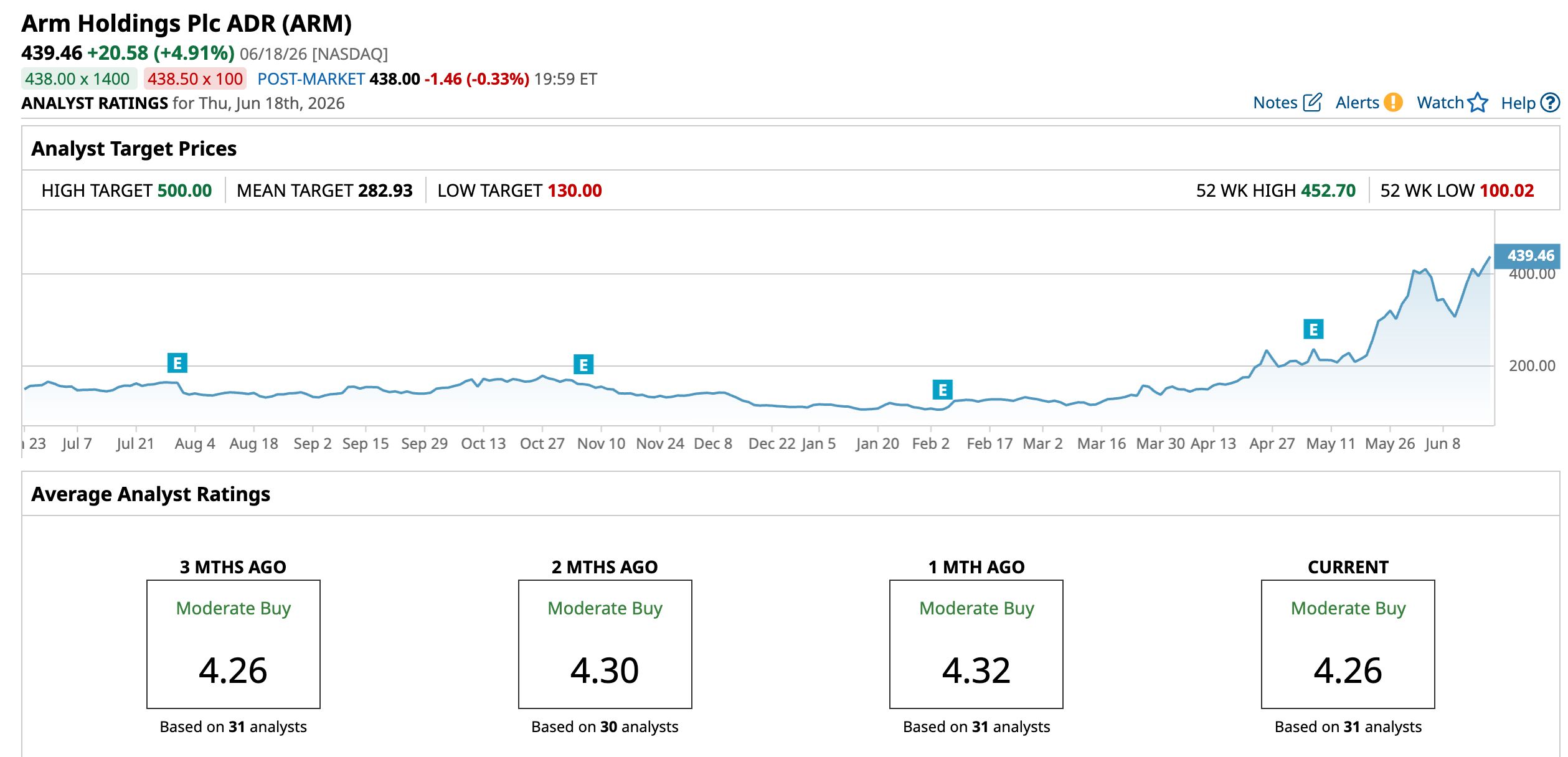

Recently, analysts at Bernstein SocGen Group raised the price target on chip IP licensing firm Arm Holdings Plc (ARM) from $300 to a Street-high of $500, representing a 66.7% increase. Bernstein analysts maintained a bullish “Outperform” rating on the stock. The reason for this rise was the company’s prospects in the agentic AI market. The analyst pointed out that ARM's architecture is well-suited for agentic AI due to its power efficiency.

Agentic AI has taken the AI space by storm, becoming the new Wall Street buzzword. Arm is clearly building for the agentic AI era. In this regard, the company launched its purpose-built Arm AGI CPU in the last quarter, which delivers more than 2x performance per rack compared to x86-based platforms. Ruthlessly driven, the company also expects to achieve its target of $15 billion in sales of its own chips earlier than anticipated due to stronger-than-expected demand.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

About Arm Holdings Stock

Arm Holdings plc operates as an intellectual property firm in the semiconductor sector, creating and licensing processor architectures and related tech for electronic devices. Rather than producing chips, Arm develops and licenses IP for CPUs, GPUs, NPUs, and interconnects to chipmakers and OEMs.

The company serves four main areas: Client, Infrastructure, Automotive, and IoT, covering consumer electronics, data centers, and automotive applications. Arm earns money through licensing fees and royalty payments. Its headquarters are located in Cambridge, England. The company has a market capitalization of $469.4 billion.

Arm Holdings is reaping the benefits, driven primarily by the AI boom and the company's strong financial performance. Investors have also welcomed the news of Arm becoming a partner in Meta Platform's (META) “Stargate” AI infrastructure project.

Over the past 52 weeks, Arm’s stock has gained 200.9%, and it is up 302% year-to-date (YTD). The company’s shares reached an all-time intraday high of $444.80 on June 17, as Bernstein gave its vote of confidence, but shares are down marginally 1.2% from that level.

www.barchart.com

www.barchart.com On a forward-adjusted basis, Arm Holdings has a price-to-earnings (non-GAAP) ratio of 202.35 times, which is a massive price tag and is significantly higher than the industry average of 24.13 times.

Arm Holdings Reported Solid Q4 Earnings Based on Strong AI-Driven Licensing Growth

For the fourth quarter of fiscal 2026 (quarter ended March 31), Arm’s total revenue increased by 20% year-over-year (YOY) to $1.49 billion, which is a record figure. This was based on licensing revenue increasing by 29% annually to $819 million, as the Arm platform expanded. Royalty revenues also grew in the double digits, with growth across smartphones, Edge AI, Physical AI, and Cloud AI. Moreover, data center royalties more than doubled YOY.

The company’s profitability also increased as a result of this. Its operating income grew 7% from the prior-year period to $438 million, while its EPS (on a diluted basis) increased by 45% YOY to $0.29. Arm’s annualized contract value grew by 22% compared to the year-ago period to $1.66 billion. For the first quarter of fiscal 2027, Arm’s management expects to report a $1.26 billion revenue (+/- $50 million) and an EPS of $0.40 (+/- $0.04).

Wall Street analysts are robustly optimistic about Arm’s future earnings. For the current fiscal year, EPS is projected to surge 30.2% annually to $1.12, followed by a 77.7% growth to $1.99 in the next fiscal year. Analysts also expect the company’s EPS to grow by 12.5% YOY to $0.18 for the current quarter.

What Do Analysts Think About Arm Holdings’ Stock?

This month, BofA analysts raised Arm’s stock price target from $245 to $335, reflecting the firm’s optimism about long-term opportunities in chiplet architectures and custom AI computing designs. BofA is positive on agentic AI, which could become the next catalyst for chipmakers.

In the same month, Mizuho raised the firm’s price target from $425 to $500 and maintained an “Outperform” rating, citing agentic AI tailwinds driven by expanding platform partnerships with Oracle and ByteDance. Mizuho now estimates that Arm could earn up to $15 billion in agentic AI infrastructure CPU revenue by fiscal year 2031.

As ARM’s CEO stated that the company may achieve its $15 billion AI chip revenue target ahead of schedule, Barclays and Wells Fargo analysts kept an “Overweight” on the company’s stock. Barclays lifted its price target to $360, while Wells Fargo raised it to $410.

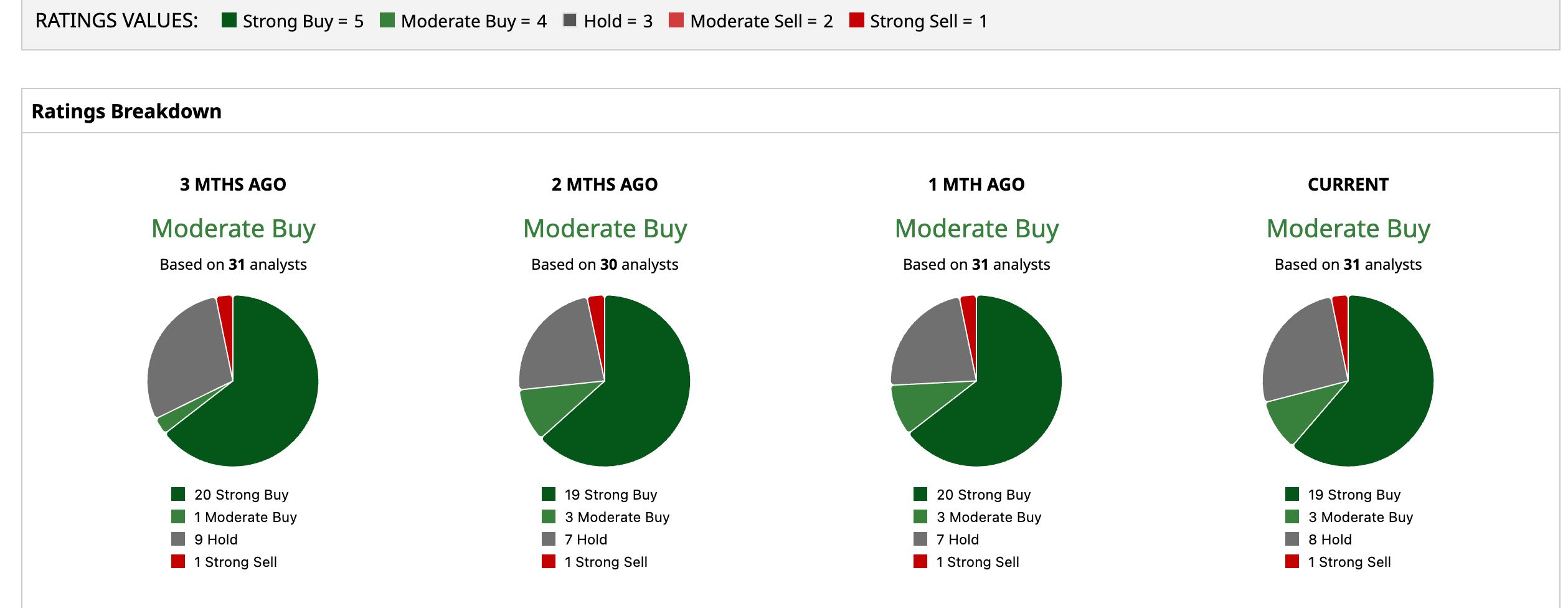

Wall Street analysts are soundly bullish on ARM’s stock, with a consensus “Moderate Buy” rating. Of the 31 analysts rating the stock, a majority of 19 analysts have given it a “Strong Buy” rating, three analysts suggested “Moderate Buy,” while eight analysts are playing it safe with a “Hold” rating, and one analyst suggested “Strong Sell.” The consensus price target of $282.93 represents a 35.62% downside from current levels. However, the Street-high price target of $500 represents 13.78% upside potential.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

From ‘Hold’ to ‘Buy’: Here Is Why Truist Just Changed Its Mind on DDOG Stock Dear Investors: Don’t Act Your Age, Act Your Risk Tolerance Rivian Is Cutting Staff Again. What That Means for RIVN Stock. SanDisk Stock Looks Wildly Overbought, But SNDK’s Chart and Fundamentals Say It Can Keep Climbing