Raymond James recently reshuffled several ratings across the U.S. airline sector ahead of second-quarter earnings. JetBlue Airways (JBLU) landed on the wrong side of that review after the firm downgraded the stock to “Underperform” from “Market Perform.”

Analyst Savanthi Syth struck a cautious tone while explaining the move. Syth acknowledged that JetBlue and Frontier (ULCC) remain “the biggest beneficiaries” of Spirit Airlines' recent demise. Even so, the analyst also pointed out that JBLU stock faces a ceiling because of the company's convertible debt, which carries a conversion price of approximately $6.12.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Raymond James also believes JetBlue should not face liquidity concerns during 2026 unless another major macroeconomic shock rocks the industry. Even so, the firm argued that “the more prudent course of action would be to address the capital structure via a Chapter 11 restructuring.”

This view did not appear out of thin air. JetBlue has spent six consecutive years in the red. The airline also carries roughly $8.5 billion in debt, while founder David Neeleman has warned that the total could approach $9 billion if 2026 losses reach the worst-case scenario. Firms have already downgraded JetBlue's credit rating to CCC+, indicating that pressure continues to mount.

The latest surge in fuel prices only adds more weight to an already overloaded balance sheet. Although JetBlue finished Q1 2026 with $2.4 billion in liquidity, the road leading into 2027 remains full of debt maturities, while a meaningful turnaround still looks difficult to achieve.

Neeleman's warning in April that JetBlue could enter bankruptcy this year only reinforced how serious the situation has become. The liquidity cushion still buys valuable time, but the airline now carries the highest risk profile across the industry.

About JetBlue Stock

Based in Long Island City, New York, JetBlue operates scheduled passenger air transportation services with a modern fleet that includes Airbus (EADSY) A220, A320, and A321 aircraft. Carrying a market capitalization of roughly $2.1 billion, the company also operates airport lounges and sells vacation packages, giving its travel business more than one string to its bow.

JBLU stock has rewarded investors despite challenges surrounding the business. The stock has climbed 29% during the past 52 weeks and advanced 23% year-to-date (YTD). The momentum has remained strong in the short term as well, with shares rising 17% over the past month.

From a valuation standpoint, the stock trades at just 0.25 times sales. The valuation remains well below both the industry average and the company's own five-year average, suggesting JBLU changes hands at a discount.

www.barchart.com

www.barchart.com A Closer Look at JetBlue’s Q1 Earnings

JetBlue reported mixed Q1 fiscal 2026 results on April 28 as healthy revenue growth could not keep mounting costs and deeper losses from stealing the spotlight. Total operating revenue rose 4.7% year-over-year (YOY) to $2.2 billion, matching Wall Street's estimates, while adjusted loss per share came in at $0.87, falling short of the expected $0.72 loss per share.

The airline squeezed more revenue per seat despite flying fewer flights. Revenue per available seat mile (RASM) increased 6.5% YOY, while system capacity measured by available seat miles declined 1.7%, landing comfortably within management's guided range.

Expenses, however, refused to play ball. Cost per available seat mile (CASM) climbed 8.3% YOY, while CASM excluding fuel increased 6.6%. Management attributed roughly four percentage points of that increase to operational disruptions during the quarter. Fuel prices also tightened the screws as the average cost per gallon surged 15.2% YOY to $2.96 from $2.57.

Profitability weakened further. Operating loss widened more than 28% YOY to $224 million, dragging operating margin to -10% from -8.2% in the prior year. Net loss also expanded to $319 million, widening 53% YOY.

Looking ahead, JetBlue expects Q2 2026 capacity growth between 1.5% and 4.5%. Management also forecast RASM growth of 7% to 11% and CASM excluding fuel growth of 3% to 5%. The airline expects fuel prices between $4.13 and $4.28 per gallon during the quarter. JetBlue plans to trim second-half 2026 capacity by two to three points versus earlier plans, concentrating those reductions during off-peak travel periods while continuing to advance its JetForward transformation initiatives.

On the other hand, Wall Street expects the company's Q2 2026 loss per share to widen 350% YOY to $0.72. Analysts also project full-year fiscal 2026 loss per share to increase by 54% to $2.53 before rebounding 93% YOY to a loss of $0.18 in fiscal 2027.

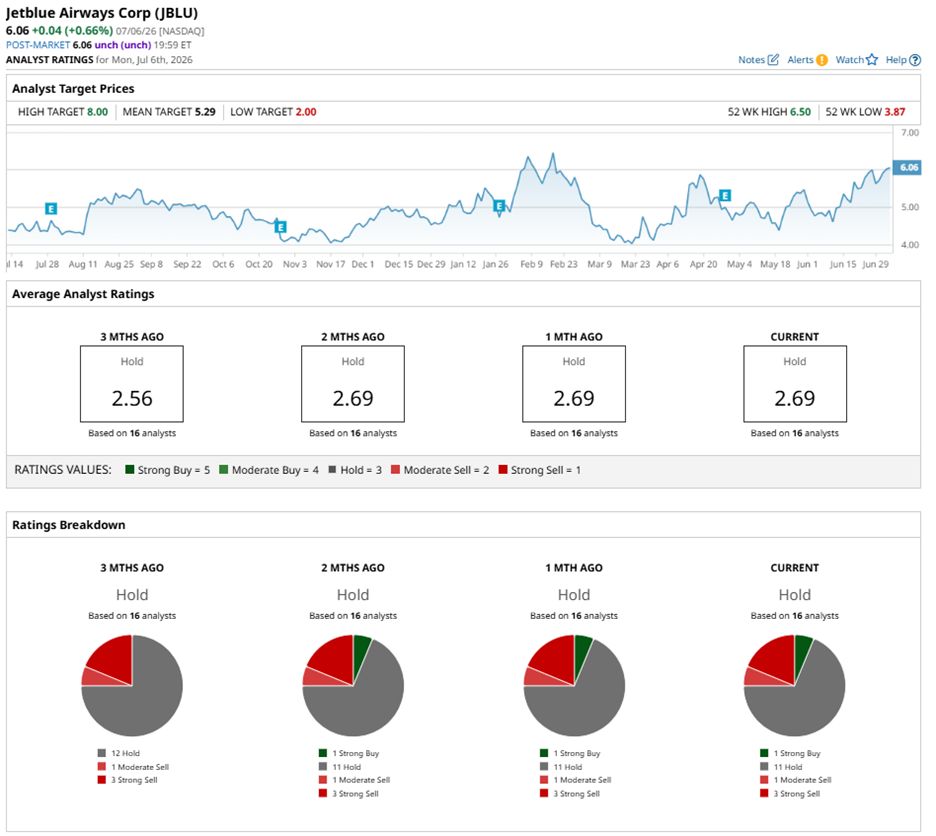

What Do Analysts Expect for JetBlue Stock?

Goldman Sachs analyst Catherine O'Brien recently raised her JBLU stock price target to $4.50 from $3.50 while keeping a “Sell” rating. The firm lifted its estimates for the airline sector after stronger revenue trends and lower fuel prices brightened the outlook. Demand has held up remarkably well since the start of the year, even after airlines rolled out significant fare increases in March to offset higher fuel costs.

Wall Street, however, continues to take a measured approach toward JetBlue. Analysts currently have an overall “Hold” rating on JBLU stock. Among the 16 analysts with coverage, one analyst recommends a “Strong Buy,” 10 maintain a “Hold” rating, one has a “Moderate Sell” rating, and four recommend a “Strong Sell.”

JBLU stock already trades above its average price target of $5.45 per share. Meanwhile, the high target of $8 implies potential upside of 43% from current levels.

www.barchart.com

www.barchart.com On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Bank of America Says AI Will Drag Down Adobe Stock Why Chapter 11 Might Be the Best Move for JetBlue Stock in 2026 IBM’s Quantum Breakthrough Sends Massive Clean Energy Signal DeepSeek Just Dealt Nvidia Stock a Potentially Major Blow