Applied Materials’ AMAT Applied Global Services (“AGS”) is becoming an increasingly important part of Applied Materials’ business because it turns the company’s large installed base into a recurring revenue engine. In the second quarter of fiscal 2026, AGS generated $1.665 billion of revenues, up from $1.42 billion a year earlier, while its gross margin improved to 34.7% and its operating margin rose to 29.2%.

The strategic value of AGS is that it adds resilience to Applied Materials' profit model. Unlike the more cyclical equipment business, services are tied to a growing installed base and to customer needs throughout the tool lifecycle. Management said AGS is another important growth driver because Applied Materials increases the revenue it generates “per tool” on top of a growing installed base.

AMAT expects the AGS segment to deliver a sustainable annual growth rate in the mid-teens, potentially higher this year. That makes AGS an important bridge between one-time equipment sales and long-duration customer relationships. What makes AGS especially relevant in the AI era is the company’s AI-enabled service layer. Applied Materials said that more than 35,000 chambers are connected to its AIx software capabilities, which use AI-powered monitoring, diagnostics and analytics.

This matters because Applied Materials’ broader AI and advanced-node strategy depends on execution, visibility and support after installation. Management noted that customers are giving the clearest and longest visibility it has ever seen, while demand remains strong across leading-edge logic and DRAM.

In that setting, AGS helps stabilize Applied Materials’ revenue base, deepen customer relationships and improve operating leverage as the company scales. The segment’s margin profile, recurring nature and AI-driven service enhancements make it a valuable part of Applied Materials’ long-term earnings power.

How Competitors Fare Against AMAT

Since AMAT serves its own installed base through the AGS business, there are no competitors in this segment. But in the broader product category, AMAT competes with Lam Research LRCX and ASML Holding ASML.

ASML is experiencing strong demand from DRAM and logic customers, which are ramping leading-edge nodes using ASML’s NXE:3800E EUV systems. Additionally, ASML noted that multiple DRAM customers are adopting EUV lithography, which helps in shortening cycle time and lowering costs. However, AMAT offers a broad range of WFE products that do not compete directly with ASML and LRCX, making the stock worth holding.

Lam Research secured multiple critical etch wins at a major DRAM manufacturer with its new Akara etch system, which supports 3D DRAM architectures. This was supported by LRCX’s customer investments in DDR5, LPDDR5 and high-bandwidth memory. Additionally, Lam Research’s Aether dry-resist technology was recently selected as the production tool of record for a leading DRAM customer, securing a foothold in this high-growth segment.

AMAT’s Price Performance, Valuation and Estimates

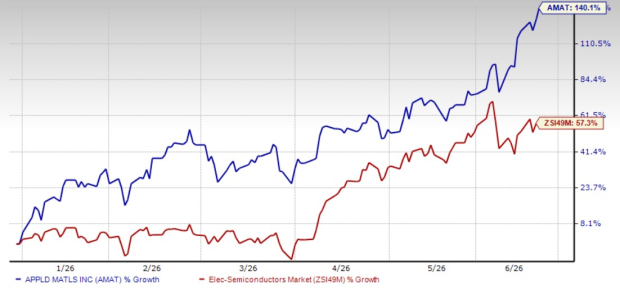

Shares of Applied Materials have surged 140.1% year to date compared with the Zacks Electronics - Semiconductors industry’s growth of 57.3%.

AMAT YTD Performance Chart

Image Source: Zacks Investment Research

From a valuation standpoint, Applied Materials trades at a forward price-to-sales ratio of 12.68X, higher than the industry’s average of 10.3X.

AMAT Forward 12-Month (P/S) Valuation Chart

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Applied Materials’ fiscal 2026 and 2027 earnings implies year-over-year growth of 28% and 32%, respectively. Estimates for fiscal 2026 have been revised upward in the past 30 days.

Image Source: Zacks Investment Research

The estimates for fiscal 2026 and 2027 have been revised upward over the past 30 days.Applied Materials currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

ASML Holding N.V. (ASML): Free Stock Analysis Report

Lam Research Corporation (LRCX): Free Stock Analysis Report

Applied Materials, Inc. (AMAT): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).