Cognyte Software Ltd. CGNT continues to deliver profitable growth despite operating in an environment marked by foreign exchange volatility and rising hardware costs. While these cost pressures affected operating expenses and cash flow in the first quarter of fiscal 2027, management highlighted that proactive cost management and operational discipline helped preserve margins and supported its full-year outlook.

The company reported a solid start to fiscal 2027, with double-digit revenue growth and significantly improved profitability. Management attributed this performance to sustained demand for its investigative analytics solutions, stronger-than-expected subscription adoption and effective management of macroeconomic challenges, including foreign exchange movements and increasing hardware-related costs. Gross margin remained strong, while profitability expanded faster than revenue, reflecting the leverage in Cognyte's business model.

Cost headwinds, however, remained visible during the first quarter. Non-GAAP operating expenses increased to $66.2 million, with management stating that most of the year-over-year increase resulted from the continued weakness of the U.S. dollar against the Israeli shekel. At the same time, higher hardware costs prompted the company to build inventory to support anticipated customer demand, increasing inventory levels by approximately $3 million during the quarter.

These factors, along with the growing mix of subscription sales, influenced cash generation. Cognyte reported negative operating cash flow of $4.7 million and negative free cash flow of $6.1 million in the first quarter. Management highlighted that subscription arrangements change the timing of cash collections, while foreign exchange dynamics and inventory investments also weighed on quarterly cash flow.

Even with these pressures, Cognyte maintained its fiscal 2027 guidance. The company continues to expect non-GAAP operating income of approximately $56 million, representing more than 50% year-over-year growth, and adjusted EBITDA of around $68 million, reflecting about 40% year-over-year growth at the midpoint of its revenue guidance, supported by proactive measures to mitigate the adverse impact of foreign exchange headwinds. Management also reaffirmed that it remains on track to achieve its fiscal 2028 adjusted EBITDA target on a constant currency basis, while updating the target to approximately 20% to reflect exchange rate changes.

Taking a Look at Cognyte’s Competitors

Palantir’s PLTR AI strategy, driven by Foundry, Gotham and AIP platforms, targets government and commercial sectors, enabling real-time insights and operational efficiency. Notable defense projects, like Open DAGIR and AIP boot camps for commercial clients, boost customer acquisition. However, intense competition from tech giants and declining cost flexibility as the company scales are headwinds.

For full-year 2026, revenue guidance was raised to between $7.650 billion and $7.662 billion, marking a significant increase from prior projections. The company also expects U.S. commercial revenue to exceed $3.224 billion and projects adjusted free cash flow in the range of $4.2 billion to $4.4 billion.

L3Harris Technologies LHX is grappling with geopolitical and trade uncertainties, including evolving sanctions, tariffs and supply chain disruptions that could increase costs, delay defense programs and pressure fixed-price contracts. At the same time, persistent labor shortages and an aging aerospace-defense workforce may constrain production capacity, potentially affecting delivery timelines and future operating performance.

For 2026, LHX expects to generate $23-23.5 billion in revenues. L3Harris anticipates earnings to be in the range of $11.40-$11.60 per share compared with the prior range of $11.30-$11.50. It expects adjusted free cash flow to be around $3 billion.

CGNT Price Performance, Valuation & Estimates

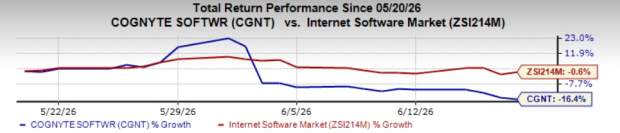

Shares of Cognyte have lost 16.4% in the past month compared with the Internet-Software industry’s decline of 0.6%.

Image Source: Zacks Investment Research

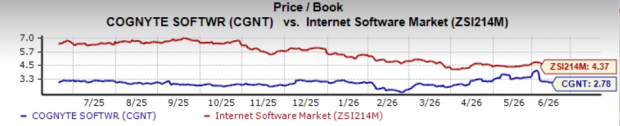

Regarding the price/book ratio, CGNT is trading at 2.78, lower than the sector’s multiple of 4.37.

Image Source: Zacks Investment Research

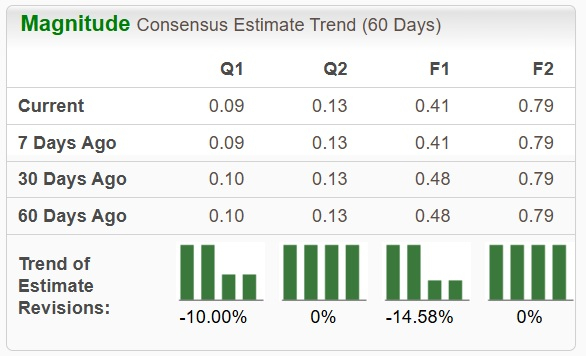

The Zacks Consensus Estimate for CGNT’s earnings for fiscal 2027 has been significantly revised downward over the past 60 days.

Image Source: Zacks Investment Research

CGNT currently carries a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Cognyte Software Ltd. (CGNT): Free Stock Analysis Report

L3Harris Technologies Inc (LHX): Free Stock Analysis Report

Palantir Technologies Inc. (PLTR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).