Automotive electrification, rising semiconductor content per vehicle, and AI-driven infrastructure spending continue to reshape the semiconductor landscape. These factors are creating significant opportunities for both Vishay Intertechnology VSH and ON Semiconductor ON.

Vishay is benefiting from accelerating momentum under its “Vishay 3.0” transformation strategy, which is helping the company capture market share across automotive electronics, industrial semiconductors, and AI-related power applications.

ON Semiconductor remains a major player in EV power systems, silicon carbide solutions, and AI data center power management. While both stocks have surged in 2026, with VSH gaining 313.5% compared with ON's 119.3%, Vishay's strong execution suggests it offers a more compelling upside opportunity for the remainder of 2026.

Looking ahead, both companies appear well positioned to benefit from favorable secular trends in EV adoption, industrial automation, and AI infrastructure spending. However, their growth narratives differ meaningfully.

Vishay is entering a broad-based recovery cycle with accelerating order momentum, expanding capacity, and increasing share gains across multiple end markets. ON Semiconductor, while benefiting from improving cyclical recovery and AI power demand, remains somewhat more dependent on the successful execution of its restructuring and portfolio optimization strategy.

YTD Price Chart VSH vs ON

Image Source: Zacks Investment Research

Case for VSH

Vishay’s strongest advantage lies in the successful execution of its aggressive Vishay 3.0 transformation strategy, which is fundamentally changing the company’s growth profile. In the first quarter of 2026, revenues increased 17.3% year over year to $839 million, exceeding guidance and reflecting strong growth across all end markets, channels, and geographies. Management emphasized that increased consumption, higher inventory replenishment, and market share gains were driving stronger volume growth. The company's total book-to-bill improved to an impressive 1.34, with backlog rising 21% to $1.6 billion.

Automotive remains one of Vishay’s most promising growth engines. Automotive revenues rose 2.7% sequentially, driven by accelerated hybrid and EV production programs and rising semiconductor content per vehicle.

Management highlighted that Vishay is now the top resistor supplier to multiple OEMs launching new EV platforms and expects these programs to scale through at least 2028. Industrial demand also remains exceptionally strong, with AI infrastructure projects in North America driving demand for power transmission, power supplies, smart grid solutions, and next-generation 800-volt power management systems for data centers.

The company is also aggressively investing in silicon carbide products and expanding manufacturing capacity through its new 12-inch German fab. Risks linger around elevated capital expenditure and near-term negative free cash flow, but operational momentum remains exceptionally strong.

AXT currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

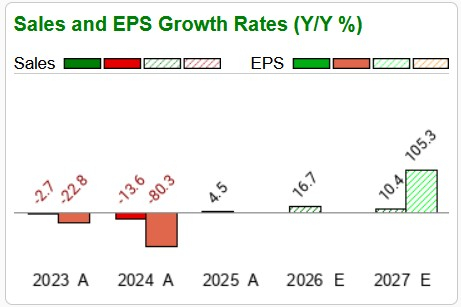

VSH’s Sales & EPS Estimate

Image Source: Zacks Investment Research

Case for ON

ON Semiconductor continues to execute its long-term strategy centered around EV power systems, silicon carbide, industrial automation, and rapidly expanding AI data center opportunities. First-quarter revenues improved 5% year over year to $1.51 billion, while gross margin improved for the third consecutive quarter to 38.5%. These gains reflect benefits from portfolio optimization and manufacturing restructuring initiatives. Management emphasized that the company has likely exited the cyclical trough and expects stronger growth in the second half.

The company remains particularly well positioned within EV power systems, where demand for silicon carbide content continues to expand rapidly. ON disclosed that its silicon carbide solutions now hold roughly 55% share of new EV models introduced at the 2026 Beijing Auto Show.

ON’s China automotive revenues grew despite a 6% decline in broader passenger vehicle demand. AI data center revenues grew more than 30% sequentially during the first quarter, with management expecting AI-related revenues to double in 2026.

Additional strength is emerging from gallium nitride products, industrial automation, robotics sensing systems, and power solutions supporting hyperscaler infrastructure. However, ON remains exposed to cyclical automotive recovery risk, inventory normalization, and the need to successfully execute its ongoing portfolio rationalization initiatives.

ON Semiconductor currently carries a Zacks Rank #2 (Buy).

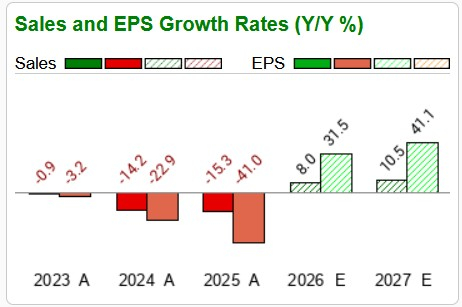

ON’s Sales & EPS Estimate

Image Source: Zacks Investment Research

Valuation Comparison

VSH trades at a forward P/E of 52.79X, significantly above the broader sector average of 23.82X and far above its own five-year median valuation of 12.63X. While the premium valuation reflects substantial optimism, investors appear increasingly rewarding Vishay’s accelerating market share gains, improving margins, and growing exposure to higher-value automotive and industrial semiconductor markets.

VSH’s P/E F12M Chart

Image Source: Zacks Investment Research

ON trades at a forward earnings of 32.06X, above both the semiconductor sector average of 23.82X and its own five-year median valuation of 16.68X. While valuation remains elevated, it appears more reasonable than Vishay’s premium multiple, reflecting a more balanced investor outlook tied to steady execution rather than explosive growth expectations.

ON’s P/E F12M Chart

Image Source: Zacks Investment Research

Conclusion

Both Vishay and ON Semiconductor are positioned to benefit from powerful long-term semiconductor growth drivers, particularly in automotive electrification, industrial automation, and AI infrastructure. ON remains a high-quality semiconductor leader with strong silicon carbide leadership, with growing hyperscaler exposure, and improving profitability.

However, Vishay currently offers the more attractive investment opportunity. Its accelerating market share gains, broad-based end-market recovery, aggressive capacity expansion strategy, improving operational execution, and rapidly strengthening automotive and industrial demand create a more powerful growth narrative. Despite premium valuation levels, Vishay’s stronger momentum, and expanding competitive position make it the more compelling auto semiconductor stock to own currently.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Vishay Intertechnology, Inc. (VSH): Free Stock Analysis Report

ON Semiconductor Corporation (ON): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).