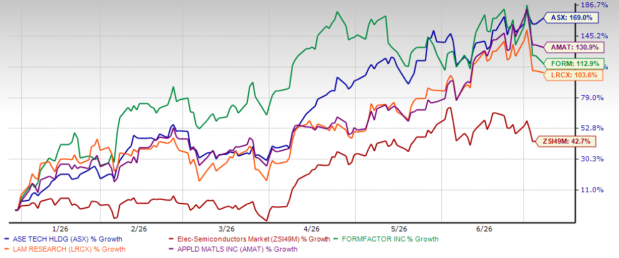

ASE Technology Holding ASX shares have rallied 169% year to date (YTD), outperforming the Zacks Electronics - Semiconductors industry's return of 42.7%. The stock also outperformed its industry peers, including FormFactor FORM, Lam Research LRCX and Applied Materials AMAT. Shares of FormFactor, Lam Research and Applied Materials have returned 112.9%, 103.6% and 130.9%, respectively, YTD.

The outperformance of ASE Technology’s shares raises the question: Does it still have room to run, or is it time for investors to consider taking profits? Let’s find out.

YTD Price Return Performance

Image Source: Zacks Investment Research

AI Packaging Demand Boosts ASX's Prospects

ASE Technology is benefiting from the growing demand for AI chip packaging. In the first quarter of 2026, ASX's Assembly, Testing and Materials (ATM) business performed better than expected, despite having fewer working days and did not see the usual seasonal slowdown. Management said AI-related products are changing the normal demand pattern, helping reduce the impact of seasonality on the business.

Advanced packaging continues to be the main growth driver. ASE reported record ATM revenues of NTD 112.4 billion in the first quarter, up 2% sequentially and 30% year over year. Higher factory utilization and a larger contribution from Leading Edge Advanced Packaging (LEAP) services were the key contributors to growth. The company said demand for AI and computing products remained strong, while growth in advanced packaging and wirebond services helped offset softer demand in some consumer markets.

ASE Technology is also increasing investments to support future growth. The company raised its 2026 capital spending plan and increased its LEAP revenue outlook by 10%. It now expects LEAP revenues to exceed $3.5 billion in 2026. Management said the additional investment will help expand capacity to meet growing customer demand and help drive further growth in the company's LEAP in the upcoming years.

The company is seeing demand not only from AI accelerator chips but also from AI-related power management, connectivity, sensors and edge devices. At the same time, it is expanding its advanced packaging technologies, including full-process packaging, CoWoS-like packaging and panel-level packaging, to support future AI applications. If AI infrastructure spending remains strong, ASE Technology is well-positioned to benefit from the growing demand for advanced semiconductor packaging.

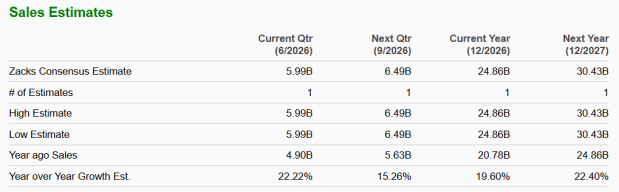

The Zacks Consensus Estimate for 2026 and 2027 indicates revenue growth of around 19.6% and 22.4%, respectively.

Image Source: Zacks Investment Research

Higher LEAP Mix Drives ASX's Margin Expansion

ASE Technology is seeing better profitability as advanced packaging becomes a larger part of its business. In the first quarter of 2026, the company's ATM gross margin increased to 26%, up 340 basis points from a year ago. Management said the improvement was mainly driven by higher factory utilization and a higher mix of LEAP services. Strong demand for AI and high-performance computing applications also supported the better margin performance.

ASE Technology is also investing to support future growth, even though these investments are creating some near-term cost pressure. The company expects depreciation expenses to increase as new LEAP production lines are installed and qualified before they begin generating meaningful revenues. Most of the new capacity is expected to contribute from the fourth quarter of 2026. Despite these higher costs, management expects ATM gross margins to improve sequentially in the second quarter of 2026 and reach the upper end of the company's structural margin range of 26% to 27%.

Looking ahead, ASE Technology expects demand for LEAP services to remain strong as the demand for advanced packaging continues to outpace available capacity, creating a favorable pricing environment for ASX. As LEAP contributes a larger share of revenue and AI demand continues to grow, ASE is well-positioned to support further margin expansion over the long term.

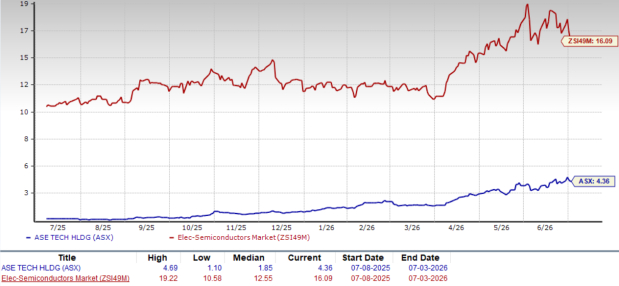

Valuation: ASX Trades Below Industry and Peers

ASX is currently trading at a lower price-to-sales (P/S) multiple, far below the Zacks Electronics – Semiconductors industry. ASX’s trailing 12-month P/S ratio sits at 4.36X, significantly lower than the Zacks industry’s trailing 12-month P/S ratio of 16.09X.

ASE TTM 12-Month P/S Ratio

Image Source: Zacks Investment Research

ASX stock also trades at a lower P/S multiple compared with other industry peers, including FormFactor, Lam Research and Applied Materials. At present, FormFactor, Lam Research and Applied Materials have P/S multiples of 11.69X, 20.38X and 16.60X, respectively.

Key Technical Indicator Signals Bullish Trend for ASX

ASX shares are trading above their 50-day & 200-day moving averages, a bullish technical signal that indicates the potential for continued upward momentum in the near term.

ASX 50-Day & 200-day Simple Moving Average

Image Source: Zacks Investment Research

Conclusion: Buy ASX Stock Right Now

ASE Technology continues to benefit from strong demand for AI chip packaging, supported by strong demand from AI and high-performance computing. The company is also expanding capacity to meet growing customer demand, while a higher mix of LEAP services and better factory utilization are helping expand margins. These factors support the outlook for continued growth.

Further, the company’s reasonable valuation offers downside protection as well, making the stock an attractive buy for investors looking for stability and steady upside. Currently, ASE Technology sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

ASE Technology Holding Co., Ltd. (ASX): Free Stock Analysis Report

Lam Research Corporation (LRCX): Free Stock Analysis Report

FormFactor, Inc. (FORM): Free Stock Analysis Report

Applied Materials, Inc. (AMAT): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).