ICON plc ICLR sits where several healthcare investment themes meet. Sponsor demand for outsourced clinical development, biotech funding, artificial intelligence and broader site access all support the company’s long-term positioning.

The issue is timing. Bookings have improved, but the earnings recovery remains uneven as revenue pressure and margin resets still weigh on near-term results.

ICON Rides a Growing CRO Market

The contract research organization market remains a favorable backdrop for ICON. Technavio analysis expects the global CRO market to expand by $85.3 billion between 2024 and 2029, reflecting a 14.6% compound annual growth rate.

That demand base is supported by continued large pharma investment in clinical pipelines and constructive biotech funding. ICON’s first-quarter 2026 net business wins were $2.88 billion, gross bookings were $3.26 billion and net book-to-bill was 1.42X.

IQVIA Holdings Inc. IQV remains a relevant peer because it also serves life sciences customers across research, technology and data-led clinical development. Charles River Laboratories International, Inc. CRL provides another comparison point, particularly in early development and drug discovery services.

ICLR Leans Into AI and Automation

ICON is positioning artificial intelligence as a productivity tool, not as a stand-alone growth slogan. Management is using the technology to improve decision speed, automate repeatable processes and reduce friction across the trial lifecycle.

The company is building an intelligence layer that powers Orbis, its agentic AI platform. It is also deploying Microsoft Copilot across key workflows and plans to embed domain-specific agents directly into clinical development work by combining Microsoft tools with access to frontier models from other providers.

ICON Expands Access to Trial Capacity

Clinical trial execution depends on patient access, site readiness and reliable early-stage capacity. ICON has expanded its U.S. early-phase capabilities with a purpose-built Phase I clinic in San Antonio, TX, with more than 130 beds.

The company also added outpatient centers in Houston, TX, and Lawrence, KS, supporting first-in-human studies as well as trials involving healthy volunteers and patient cohorts. These assets align with sponsor demand for faster start-up timelines and more predictable recruitment.

The Accellacare footprint and Advarra partnership add another layer to that strategy by supporting research-ready site access. ICON is also investing in lab automation and more than 100 biomarker assays, broadening support for biomarker-driven research.

In the past year, ICLR shares have gained 12.1% compared with the S&P 500 composite’s 24.1% growth.

Image Source: Zacks Investment Research

ICLR Still Faces a Margin Reality Check

The growth narrative has not yet repaired ICON’s earnings profile. First-quarter 2026 revenues were $2.03 billion, up 0.9% year over year on a reported basis but down 1.9% at constant currency.

Adjusted EBITDA declined 20.2% year over year, while adjusted EBITDA margin fell to 15.6% from 19.8% in the prior-year period. Adjusted earnings were $2.50 per share, down from $3.27 a year earlier.

Management attributed the margin reset to organic revenue decline, mix shifts toward functional service work versus full-service revenues, foreign exchange and prior pricing dynamics. Full-year 2026 revenues are expected between $7.85 billion and $8.15 billion, below the $8.25 billion generated in 2025.

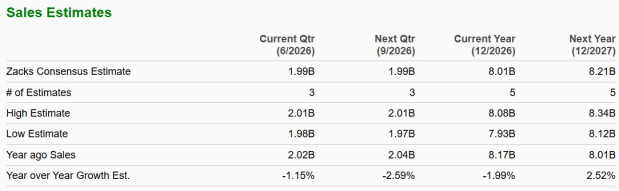

Per the Zacks Consensus Estimate, 2026 revenues are pegged at $8.01 billion.

Image Source: Zacks Investment Research

What ICON Ratings Say About the Trend Trade

The bottom line is that ICON has exposure to favorable CRO, technology and trial-access trends, but the stock’s earnings profile has not fully caught up with those themes. Backlog rose 4.0% sequentially to $22.7 billion, yet management expects the benefit of recent wins to matter more in 2027 than in 2026.

ICLR currently carries a Zacks Rank #5 (Strong Sell). The rank is tied to earnings estimate revision trends over a one- to three-month horizon, so it keeps the stock in a cautious category despite improving order flow.

The Style Scores show a split setup. ICON has a Value Score of D, Growth Score of F, Momentum Score of A and VGM Score of D. The Momentum Score points to better recent price action, including a 62.03% 12-week price change, but the weak Value and Growth scores limit the broader style profile.

For investors watching the trend trade, the message is mixed. CRO demand, AI-enabled workflows and expanded trial capacity support the longer-term case, but the Zacks Rank and weak growth score argue for patience until earnings visibility improves.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

ICON PLC (ICLR): Free Stock Analysis Report

Charles River Laboratories International, Inc. (CRL): Free Stock Analysis Report

IQVIA Holdings Inc. (IQV): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).