PepsiCo, Inc. PEP has reported strong second-quarter 2026 results, wherein revenues and earnings per share (EPS) beat the Zacks Consensus Estimate and improved year over year. Results have reflected organic revenue growth, favorable foreign currency translation, and a net benefit from acquisitions and divestitures.

PEP’s second-quarter core EPS of $2.20 beat the Zacks Consensus Estimate of $2.19 by 0.5% and improved 4% year over year. The company’s core constant-currency EPS increased 1%. Foreign currency aided EPS by 3%. Reported earnings were $2.18 per share versus 92 cents in the year-ago quarter.

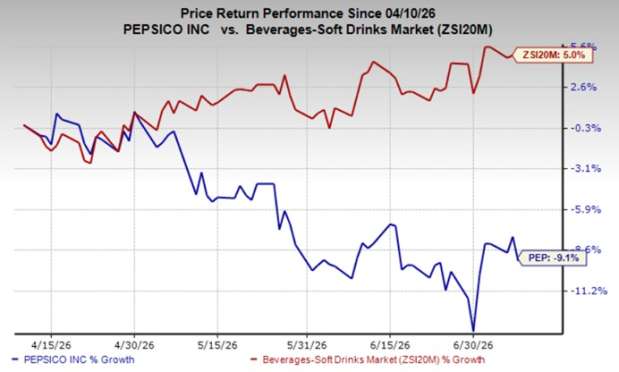

Shares of the Zacks Rank #4 (Sell) company have lost 9.1% in the past three months against the industry’s 5% growth.

Image Source: Zacks Investment Research

Peek Into PEP’s Q2 Details

Net revenues rose 6.4% to $24.18 billion and surpassed the Zacks Consensus Estimate of $23.87 billion by 1.3%. Organic revenues increased 2.4%, with global convenient foods organic volume up 3% and global beverages organic volume up 2%.

PepsiCo’s net revenue growth included a 2.2-percentage-point benefit from foreign exchange translation and a 1.8-percentage-point net benefit from acquisitions and divestitures. Organic revenue growth reflected effective net pricing and a contribution from organic volume growth.

Our model predicted year-over-year organic revenue growth of 2.6% for the second quarter, with a 2.5% gain from the price/mix and a 0.1% rise in volume.

On a consolidated basis, the reported gross profit rose 5.5% year over year to $13.11 billion. The core gross profit increased 4.7% year over year to $13.12 billion. The reported gross margin contracted 50 bps to 54.2%, whereas the core gross margin fell 80 bps year over year to 54.3%, reflecting the continued impacts of cost pressures and business investments.

We anticipated the core gross margin to decline 40 bps year over year to 54.7% in the second quarter. In dollar terms, core gross profit was expected to increase 4.1% year over year.

PepsiCo, Inc. Price, Consensus and EPS Surprise

PepsiCo, Inc. price-consensus-eps-surprise-chart | PepsiCo, Inc. Quote

PepsiCo’s operating profit surged 125% to $4.02 billion in the second quarter of 2026, while core operating profit increased 4% to $4.07 billion. The sharp reported operating profit increase reflected prior-year impairment charges related to the Rockstar and Be & Cheery brands, lower restructuring charges and a favorable net impact of acquisition and divestiture-related charges and credits.

The reported operating margin expanded 875 bps to 16.6%. The core operating margin contracted 40 basis points to 16.8%, as productivity savings and effective net pricing were partly offset by certain operating cost increases.

Our model predicted core SG&A expenses of $8.9 billion, which indicated year-over-year growth of 3.3%. As a percentage of revenues, core SG&A expenses were anticipated to be 37.4%, suggesting a 50-bps decline from the prior-year quarter.

We expected a core operating margin of 17.4%, implying a 20-bps increase from the year-ago quarter’s actual.

PEP’s Segment Trends

PepsiCo Foods North America delivered net revenues of $6.37 billion, down 2% year over year. Organic revenues also declined 2% due to lower effective net pricing. The segment continued to gain volume share in North America, aided by innovation and affordability initiatives. Management noted improvements in household penetration and volume share across the U.S. savory and salty categories.

PepsiCo Beverages North America generated net revenues of $7.24 billion, up 7% year over year. Organic revenues grew 1%, while acquisitions, net of divestitures, contributed 6 percentage points to reported revenue growth. However, the organic volume declined 4%, including a 0.5-percentage-point headwind tied to the case pack water business transition to a third-party partner. Functional hydration and zero-sugar offerings remained bright spots.

International results were the strongest part of the quarter. International organic revenues increased 7%, marking the 21st consecutive quarter of at least mid-single-digit organic revenue growth.

Within the international business, International Beverage (IB) Franchise revenues rose 11% to $1.52 billion, with organic revenues up 9%. The organic volume increased 5% in the segment, which represents more than 60% of global beverage volume. The international convenient foods organic volume increased 4%, which represents 70% of the global convenient foods volume.

Europe, Middle East and Africa revenues increased 10% year over year to $4.98 billion, with organic revenues up 6%. Latin America Foods’ revenues rose 15% to $2.94 billion, while organic revenues increased 4%. Asia Pacific Foods’ revenues advanced 12% to $1.12 billion. Organic revenues grew 9%, supported by a 10% organic volume increase, the strongest volume performance among the reported segments.

Financials of PepsiCo Show Stability

PEP ended second-quarter 2026 with improved liquidity, as cash and cash equivalents of $10.25 billion as of June 13, 2026, increased from $9.16 billion at the end of fiscal 2025. Short-term debt obligations were $10.6 billion, while long-term debt obligations were $42.61 billion.

Net cash provided by operating activities was $2.37 billion as of the end of second-quarter 2026 compared with $996 million in the year-ago period. Capital spending totaled $1.27 billion.

The company paid out cash dividends of $3.91 billion and repurchased $479 million of shares in the first half of 2026.

PEP’s Outlook for 2026

PepsiCo has reaffirmed its outlook for 2026. The company expects organic revenue growth of 2-4% and net revenue growth of 4-6% on a reported basis.

Core constant-currency EPS is anticipated to increase 4-6%, with core EPS growth of 5-7%. Based on current rates, foreign exchange translation is expected to provide a 1-percentage-point benefit to reported net revenue and core earnings growth. Acquisitions, net of divestitures, are expected to contribute 1 percentage point to reported revenue growth. The company expects a core effective tax rate of 22% for 2026.

The company expects capital spending to remain below 5% of net revenues, while targeting a free cash flow conversion ratio of at least 80%.

PEP has been committed to rewarding its shareholders through dividends and share buybacks. It expects to return total cash of $8.9 billion to shareholders in 2026, including $7.9 billion in dividends and $1 billion in share repurchases.

Don’t Miss These Better-Ranked Stocks

Fomento Economico Mexicano S.A.B. de C.V. FMX, alias FEMSA, is a leading Latin American consumer company with operations spanning retail, beverage bottling and logistics, serving millions of customers across multiple markets. The company currently flaunts a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for FEMSA’s 2026 sales and earnings implies growth of 17.3% and 131%, respectively, from the previous year’s reported numbers. FMX delivered a trailing four-quarter negative earnings surprise of 17%, on average.

The Coca-Cola Company KO is the world's largest non-alcoholic beverage company, marketing a broad portfolio of sparkling soft drinks, water, juice, coffee, tea and sports beverages. It currently carries a Zacks Rank #2 (Buy).

The Zacks Consensus Estimate for Coca-Cola’s 2026 sales and earnings indicates growth of 3% and 8.7%, respectively, from the prior-year reported levels. KO delivered a trailing four-quarter earnings surprise of 4.5%, on average.

Ambev S.A. ABEV is a leading beverage company in Latin America, producing, distributing and selling beer, soft drinks and other non-alcoholic beverages across multiple markets in the region. It carries a Zacks Rank #2 at present.

The Zacks Consensus Estimate for Ambev’s 2026 sales and earnings implies increases of 16.7% and 16.6%, respectively, from the prior-year reported levels.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

CocaCola Company (The) (KO): Free Stock Analysis Report

Fomento Economico Mexicano S.A.B. de C.V. (FMX): Free Stock Analysis Report

PepsiCo, Inc. (PEP): Free Stock Analysis Report

Ambev S.A. (ABEV): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).