Taiwan Semiconductor TSM or TSMC is scheduled to report its second-quarter 2026 results on July 16, before market opens. The results are expected to reflect continued strength in its High-Performance Computing (HPC) platform, driven by robust AI chip demand from hyperscalers and leading semiconductor customers.

The company's advanced process technologies, particularly the 3nm family and growing demand for advanced packaging solutions are also expected to support another quarter of solid growth. Meanwhile, the smartphone business is likely to remain healthy on seasonal demand, though AI-related HPC is expected to remain the primary growth engine.

Check out our analysis to determine whether TSM stock is worth buying ahead of its second-quarter earnings.

Q2 Expectation for HPC

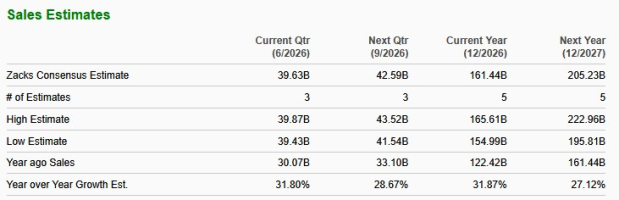

During its first-quarter 2026 announcement, TSMC provided guidance for its second-quarter revenues in the band of $39.0-$40.2 billion, implying roughly 10% sequential growth at the midpoint, supported by continued strength in leading-edge process technologies. The Zacks Consensus Estimate for second-quarter revenues is pegged at $39.63 billion. Management also projected gross margin of 65.5%-67.5% and operating margin of 56.5%-58.5%, reflecting sustained high-capacity utilization and ongoing cost-improvement initiatives despite dilution from overseas fabs.

Image Source: Zacks Investment Research

The biggest driver is expected to remain the HPC platform, which has emerged as TSMC's largest business. In the first quarter, HPC revenues climbed 20% sequentially and accounted for 61% of total revenues, far surpassing smartphones at 26%. The company attributed the momentum to robust AI-related demand, noting that the shift from generative AI toward agentic AI is increasing token consumption and computational requirements, thereby boosting demand for leading-edge silicon. The company also emphasized that cloud service providers continue to provide a strong demand outlook. With trends remaining the same, we expect HPC once again to be the top performer in the second quarter of 2026.

Importantly, TSMC indicated that AI- and HPC-related demand remains supply-constrained rather than demand-constrained. During the first-quarter announcement, the company repeatedly stated that demand for HPC AI applications continues to exceed available capacity, prompting the company to raise its 2026 capital spending outlook toward the upper end of its $52-$56 billion range. TSM also announced an expanded global 3-nanometer capacity plan, including additional capacity in Taiwan, Arizona and Japan, while continuing to convert 5-nanometer tools to support N3 production. The company said these investments are primarily intended to meet robust demand from HPC AI customers. This should get reflected through the second-quarter results.

TSMC's monthly revenue updates from April to June pointed to sustained demand for advanced process technologies, while management's second-quarter guidance called for sequential revenue growth. Particularly, the company reported strong June 2026 monthly revenues, resulting in record second-quarter revenues on a monthly-sales basis and indicating that demand for advanced process technologies remained robust. This should get reflected through in the second-quarter numbers.

Earnings Whispers for TSM Stock

Per our proven model, stocks with a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold), along with a positive Earnings ESP, have a higher chance of beating estimates, which is not the case here:

TSM’s Earnings ESP: TSMC has an Earnings ESP of 0.00%. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

TSM’s Zacks Rank: TSMC currently carries a Zacks Rank #2. You can see the complete list of today’s Zacks #1 Rank stocks here.

Taiwan Semiconductor Manufacturing Company Ltd. Price and EPS Surprise

Taiwan Semiconductor Manufacturing Company Ltd. price-eps-surprise | Taiwan Semiconductor Manufacturing Company Ltd. Quote

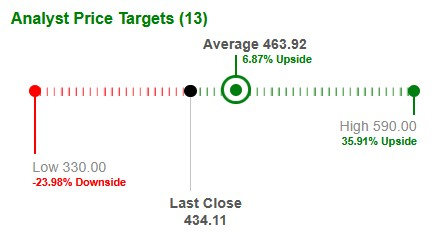

TSMC Price Target

Based on short-term price targets offered by 13 analysts, the average price target for TSMC comes to $463.92. This represents an increase of 6.87% from the last closing price.

Image Source: Zacks Investment Research

Competitive Positioning

Intel INTC: Intel is scheduled to report second-quarter 2026 results on July 23. Demand across its Client Computing and Data Center & AI businesses is expected to have remained supportive in the second quarter, while Intel Foundry is anticipated to benefit from a higher EUV wafer mix and continued customer engagement. However, heavy investments in leading-edge manufacturing, process technology development and global fab expansion are likely to continue to weigh on near-term profitability. The stock carries a Zacks Rank #1 with an Earnings ESP of 0.00%

Broadcom AVGO: Its third-quarter fiscal 2026 results are expected to benefit from sustained demand for custom AI accelerators and AI networking products, supported by ongoing hyperscaler investments in AI infrastructure. Growth in AI semiconductor revenues is likely to remain the primary catalyst, while performance across its non-AI semiconductor and infrastructure software segments could influence the pace of overall revenue and earnings growth. The company carries a Zacks Rank #2 and has an Earnings ESP of 0.00%.

Final Take

TSMC remains well-positioned ahead of its second-quarter results, supported by resilient AI-driven HPC demand, industry-leading advanced process technologies and expectations of record quarterly revenues. While the lack of a positive ESP tempers near-term earnings beat expectations, long-term fundamentals remain compelling. Investors may consider buying the stock with a measured approach ahead of the earnings release.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Taiwan Semiconductor Manufacturing Company Ltd. (TSM): Free Stock Analysis Report

Intel Corporation (INTC): Free Stock Analysis Report

Broadcom Inc. (AVGO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).