Brinker International EAT continues to benefit from Chili's sustained momentum, supported by resilient traffic, industry-leading value, effective marketing and ongoing menu innovation. The company remains focused on enhancing food, service and atmosphere through operational improvements, technology investments and restaurant reimages, strengthening the guest experience and supporting long-term traffic growth. Strong cash generation continues to fund growth initiatives and shareholder returns, while disciplined execution positions the company to deliver sustainable earnings growth.

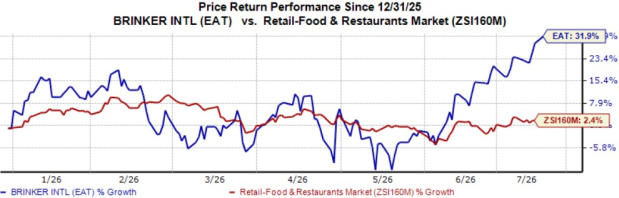

Shares of this casual dining chain have gained 31.9% in the year-to-date period, outperforming the Zacks Retail - Restaurants industry’s 2.4% rise. Its earnings topped the Zacks Consensus Estimate in each of the trailing four quarters, with an average being 6.8%.

Image Source: Zacks Investment Research

The fiscal 2026 earnings estimate has edged up to $10.75 per share from $10.73 over the past 60 days. Although Brinker continues to face commodity inflation, higher operating costs and weak performance at Maggiano's, Chili's sustained sales momentum, disciplined cost management and continued operating leverage are expected to support solid earnings growth.

Brinker — a Zacks Rank #2 (Buy) stock — has a favorable VGM Score of A. Let’s delve into the major driving factors.

Factors Aiding EAT Stock

Resilient Chili’s Traffic: Chili’s traffic performance remained resilient despite severe weather, a holiday shift and an exceptionally difficult comparison. The brand delivered 4% same-store sales growth in the fiscal third quarter while lapping a 31.6% increase in the prior-year period, marking its 20th consecutive quarter of positive comparable sales growth. Chili’s also outpaced the casual dining industry by 420 basis points during the quarter.

This resilience reflects Chili’s focus on improving food, service and atmosphere while maintaining an industry-leading value proposition. Guest experience indicators continued to strengthen, with Guests With A Problem falling to 1.9%, food-grade scores reaching 75% and intent to return rising to a record 79%. New customers also began visiting at frequencies similar to existing guests, supporting more sustainable traffic growth. The early success of the new chicken sandwich platform, which generated 161% higher sandwich sales than before the launch, provided an additional traffic catalyst.

Effective Marketing and Menu Innovation: Brinker’s marketing and menu strategy supported fiscal third-quarter demand by reinforcing value, attracting new guests and improving loyalty. Management emphasized that continuous menu innovation, compelling media campaigns and a disciplined focus on food, service and atmosphere helped reinforce the company's value proposition and supported resilient guest demand despite weather-related disruptions and a challenging consumer environment.

At Chili’s, the new chicken sandwich platform and “Better Than Fast Food” campaign lifted sandwich sales 161% from pre-launch levels, while upgrades to ribs, queso, nachos and burgers strengthened value. Meanwhile, Maggiano's restored classic menu favorites, increased portion sizes and improved its family-style offerings as part of its ongoing turnaround strategy, helping improve customer value perception. Collectively, these marketing and menu initiatives supported traffic, strengthened brand relevance and positioned the company for sustainable long-term growth.

Operational Discipline Over Promotional Activity: Brinker continues to favor durable operational improvements over frequent, limited-time promotions. The company is investing in food quality, service, restaurant cleanliness and team training while simplifying restaurant processes to support repeat visits and sustainable traffic growth. This approach helped reduce Guests With A Problem to 1.9%, while food-grade scores reached 75%, and intent to return rose to a record 79%. Operational discipline also supports cost efficiency. Restaurant labor declined 60 basis points year over year to 31.4% of sales, as sales leverage offset wage inflation of approximately 3.4%, additional labor investments and higher health insurance costs. The company is now shifting its focus toward faster cycle times, better kitchen throughput and more efficient table turns through its North of 6 initiative, upgraded handheld devices, kitchen display systems and payment-process improvements.

Strong Free Cash Flow and Disciplined Capital Allocation: Brinker continues to generate robust cash flow, providing the financial flexibility to invest in growth while enhancing shareholder returns. During the first nine months of fiscal 2026, net cash from operating activities increased to $571.8 million from $493 million a year earlier. The company used this cash flow to fully repay outstanding borrowings under its revolving credit facility, repurchase $108 million of common stock during the fiscal third quarter ($343.4 million year to date) and fund strategic investments across the business. Brinker maintained a disciplined capital allocation strategy by investing in restaurant reimages, new unit development and guest-facing improvements while keeping leverage low. Management said its strong cash generation positions Brinker to continue funding growth initiatives and enhancing shareholder returns.

Other Key Picks

Some other top-ranked stocks from the Zacks Retail-Wholesale sector are:

Arcos Dorados Holdings Inc. ARCO presently sports a Zacks Rank #1 (Strong Buy). The company delivered a trailing four-quarter earnings surprise of 18.6%, on average. ARCO stock has gained 13% year to date. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Arco Dorados’ 2026 sales and earnings per share (EPS) indicates growth of 10% and 180.8%, respectively, from the year-ago period’s levels.

Five Below, Inc. FIVE presently sports a Zacks Rank of 1. The company delivered a trailing four-quarter earnings surprise of 70.1%, on average. FIVE stock has risen 1.7% year to date.

The Zacks Consensus Estimate for Five Below’s fiscal 2026 sales and EPS indicates growth of 14.7% and 35.1%, respectively, from the year-ago period’s levels.

Dillard's, Inc. DDS sports a Zacks Rank of 1 at present. The company delivered a trailing four-quarter earnings surprise of 27.9%, on average. DDS stock has declined 13.3% year to date.

The Zacks Consensus Estimate for Dillard’s fiscal 2026 sales and EPS indicates growth of 2.1% and 6.3%, respectively, from the prior-year levels.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Brinker International, Inc. (EAT): Free Stock Analysis Report

Dillard's, Inc. (DDS): Free Stock Analysis Report

Five Below, Inc. (FIVE): Free Stock Analysis Report

Arcos Dorados Holdings Inc. (ARCO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).