Veeva Systems Inc. VEEV is well-poised for growth in the coming quarters, courtesy of its strong product portfolio. The optimism, led by a solid first-quarter fiscal 2027 performance and CRM migrations, is expected to contribute further. However, market saturation remains a cause for concern.

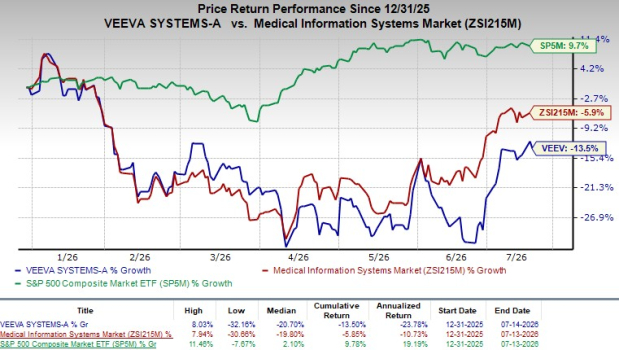

This Zacks Rank #3 (Hold) company’s shares have lost 13.5% in the year-to-date period compared with the 5.9% decline of the industry. The S&P 500 composite has increased 9.7% during the said time frame.

The renowned provider of cloud-based software applications and data solutions for the life sciences industry has a market capitalization of $31.97 billion. The company anticipates 35% growth for the next five years and expects to maintain its strong performance in the future. It delivered a trailing four-quarter average earnings surprise of 5.5%.

Image Source: Zacks Investment Research

Reasons Favoring VEEV’s Growth

Diversified Platform Driving Durable Growth:Veeva Systems’ long-term growth story is increasingly tied to its position at the center of life sciences digital transformation. The company operates across a broad set of markets spanning clinical development, quality management, regulatory operations, safety, commercial engagement and data analytics. Veeva Systems’ Development Cloud portfolio is particularly well-positioned as pharmaceutical companies seek integrated platforms that connect clinical data, trial operations, quality processes and regulatory functions within a unified ecosystem.

Growth is being fueled by newer product areas that remain in the early stages of penetration, including clinical data management, randomization and trial supply management, drug safety and laboratory information management systems. Management believes these businesses have a significant runway as customers increasingly favor end-to-end platforms over fragmented point solutions.

Enterprise CRM Migrations Expanding Account Footprint: Vault CRM adoption continues to build as large customers move off legacy CRM deployments and standardize commercial workflows. Management highlighted recent global selections from Teva and Merck KGaA and noted that Veeva Systems has secured 10 wins compared with six for Salesforce, within its defined top 20 cohort, with four decisions still pending.

The company also cited an overall Vault CRM win rate above 80% and more than 150 customers live, supported by over 40 completed migrations. This installed base creates a multi-year services and subscription runway and should support the attachment of adjacent commercial applications.

Strong Q1 Results: Veeva Systems exited the first quarter of fiscal 2027 with better-than-expected results, wherein both earnings and revenues beat the Zacks Consensus Estimate. The uptick in both top and bottom lines and robust performance by the Subscription services segment during the quarter were impressive. The uptick in Professional services and others’ revenues also bodes well.

Veeva Systems continues to strengthen its position in life sciences software through rapid innovation in artificial intelligence and expanding customer adoption. During the fiscal first quarter, the company significantly advanced its industry-specific AI strategy. Ostro, acquired in March, is now delivering compliant conversational AI for more than 50 brands, while Vault AI remains on track for deployment across all Vault applications in August.

Factor That May Offset VEEV’s Gains

Market Saturation: The life sciences industry, Veeva Systems' primary market for its CRM solutions, is facing increasing saturation as digital transformation and CRM adoption have become widespread across pharmaceutical and biotech companies. Many large enterprises have already implemented Veeva Systems' CRM software or similar solutions, leaving fewer untapped opportunities for new customer acquisition.

Additionally, as smaller biotech firms and generics manufacturers enter the market, they may seek more cost-effective or niche CRM alternatives rather than Veeva Systems' premium offerings. This saturation, combined with heightened competition from both traditional CRM providers and emerging AI-powered platforms, could limit Veeva Systems' ability to maintain its historical CRM sales growth rates.

Estimate Trend

Veeva Systems is witnessing a stable estimate revision trend for fiscal 2027. In the past 30 days, the Zacks Consensus Estimate for fiscal 2027 earnings per share (EPS) has remained stable at $9.05.

The Zacks Consensus Estimate for second-quarter fiscal 2027 revenues is pegged at $904.1 million, indicating a 14.6% improvement from the year-ago quarter’s reported number. The EPS estimate for the second quarter of fiscal 2027 is pinned at $2.22, implying a 11.6% improvement year over year.

Key Picks

Some better-ranked stocks from the broader medical space are West Pharmaceutical WST, Intuitive Surgical ISRG and Cardinal Health CAH, each carrying a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

West Pharmaceutical reported first-quarter 2026 earnings per share of $2.13, which beat the Zacks Consensus Estimate by 26.8%. Revenues of $844.9 million surpassed the Zacks Consensus Estimate by 8.5%.

West Pharmaceutical has an estimated long-term earnings growth rate of 13.9%. WST’s earnings surpassed estimates in the trailing four quarters, the average surprise being 19.4%.

Intuitive Surgical reported first-quarter 2026 adjusted EPS of $2.50, which beat the Zacks Consensus Estimate by 20.2%. Revenues of $2.77 billion surpassed the Zacks Consensus Estimate by 6.2%.

Intuitive Surgical has an estimated long-term earnings growth rate of 14.3%. ISRG’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 16.8%.

Cardinal Health reported a third-quarter fiscal 2026 adjusted EPS of $3.17, which beat the Zacks Consensus Estimate by 13.2%. Revenues of $60.94 billion missed the Zacks Consensus Estimate by 2.3%.

Cardinal Health has an estimated long-term earnings growth rate of 17%. CAH’s earnings surpassed estimates in the trailing four quarters, the average surprise being 10.3%.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Veeva Systems Inc. (VEEV): Free Stock Analysis Report

Intuitive Surgical, Inc. (ISRG): Free Stock Analysis Report

Cardinal Health, Inc. (CAH): Free Stock Analysis Report

West Pharmaceutical Services, Inc. (WST): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).