NeuroPace, Inc. NPCE is well-positioned for solid growth, driven by strong RNS adoption, expanding referral networks and AI-driven innovations that enhance efficiency and utilization. The potential IGE indication offers a long-term growth opportunity. However, near-term profitability may be pressured by higher investments and seasonality, while IGE contribution could be delayed due to approval uncertainty, payer coverage expansion and physician adoption, leaving the core business to drive growth.

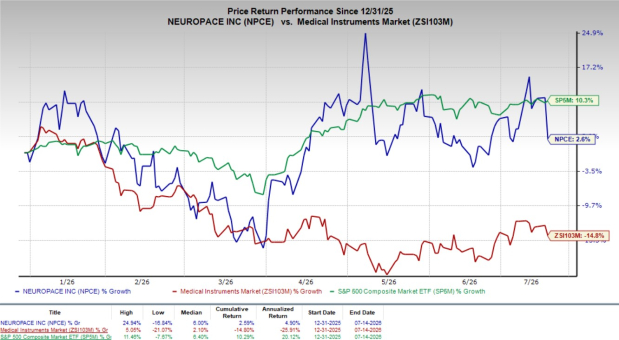

In the year-to-date period, this Zacks Rank #3 (Hold) company’s shares have gained 2.6% against the industry’s 14.8% decline. However, the S&P 500 has risen 10.3% in the same timeframe.

As a developer of neuromodulation technology for epilepsy, NeuroPace’s core product is the RNS System, a closed-loop, brain-responsive implant that monitors intracranial EEG, detects patient-specific abnormal electrical patterns and delivers targeted stimulation to help prevent seizures. It has a market capitalization of $583.7 million.

The company projects 100% growth for 2027 and expects to maintain its strong performance going forward. NeuroPace’s earnings surpassed the Zacks Consensus Estimate in three of the trailing four quarters and missed one, delivering an average surprise of 27.8%.

Image Source: Zacks Investment Research

Factors Favoring NPCE’s Growth

Strong Commercial Momentum Supports Sustainable Growth: NeuroPace's long-term growth outlook continues to be supported by strong commercial execution. Management highlighted record highs in active prescribers, customer accounts and patient pipeline, reflecting growing physician adoption and increasing referrals from both Level 4 epilepsy centers and community providers. The company is also strengthening its commercial organization through targeted sales force expansion, nurse navigator support and enhanced patient funnel management, which should improve patient conversion and support sustained procedure growth over time. Encouraged by these trends, NeuroPace raised its 2026 revenue guidance while excluding any contribution from a potential idiopathic generalized epilepsy (IGE) indication, demonstrating confidence in the strength of its core business.

Expanding Clinical Indications Could Increase the Addressable Market: Another growth catalyst is the potential expansion of the RNS System into new patient populations. The company's PMA supplement seeking FDA approval for treating IGE remains on track, with management describing constructive interactions with the FDA during the review process. Clinical data from the NAUTILUS study continue to demonstrate meaningful reductions in seizure frequency, injuries and rescue medication use, reinforcing confidence in the therapy's broader clinical value. NeuroPace recently showcased NAUTILUS data and the expanding role of responsive neuromodulation at the 2026 ASSFN Meeting, while also highlighting potential future applications in broader epilepsy populations, including Lennox-Gastaut syndrome.

AI Innovation and Robust Clinical Evidence Strengthen Competitive Position: NeuroPace continues to strengthen its competitive position through AI-driven innovation and its growing clinical evidence base. The recently FDA-approved ECoG Assistant is designed to streamline EEG data analysis, helping physicians manage patients more efficiently while lowering barriers for new RNS adopters. The company is leveraging its proprietary database of more than 26 million intracranial EEG recordings to develop advanced AI models that could further personalize therapy and improve clinical outcomes. Combined with long-term studies demonstrating durable seizure reduction, these technology investments reinforce the RNS platform's differentiation and support future adoption.

Factors That May Offset the Gains for NPCE

IGE Commercialization Could Take Longer Than Expected: While the potential approval of the RNS System for IGE represents NeuroPace's biggest growth opportunity, its commercial impact may not be immediate. The FDA review remains ongoing and management reiterated that its 2026 guidance excludes any contribution from the IGE indication. Even if approval is secured around midyear, the company expects reimbursement expansion, physician training and payer coverage to take time before meaningful revenues are generated. Since most patients are covered by private insurers, coverage expansion is likely to occur gradually, making the revenue contribution more back-end loaded. Any regulatory delay or slower-than-expected reimbursement rollout could postpone this growth catalyst and leave the company reliant on its core adult focal epilepsy business for the remainder of 2026.

Commercial Expansion Strategy Faces Execution Risk: NeuroPace continues to expand beyond traditional Level 4 epilepsy centers by strengthening community referral networks and investing in its commercial infrastructure. Converting a larger patient pipeline into implant procedures requires seamless coordination among referring physicians, epilepsy centers and implanting hospitals. The company is adding sales representatives, expanding patient navigation resources and refining referral management to improve conversion rates. If these initiatives fail to generate the expected productivity improvements or patient conversions take longer than anticipated, revenue growth could fall short of management's expectations.

Continued Investments May Delay Margin Expansion: NeuroPace is making significant investments in AI-enabled products, cloud infrastructure and next-generation neuromodulation technologies to support long-term growth. While these initiatives strengthen the company's competitive position, they also require sustained R&D and commercial spending before meaningful returns are realized. Management expects adjusted EBITDA to remain negative in 2026 as it continues investing for future growth. If AI product adoption, cloud migration or commercial productivity progress more slowly than anticipated, operating leverage and profitability could take longer to materialize.

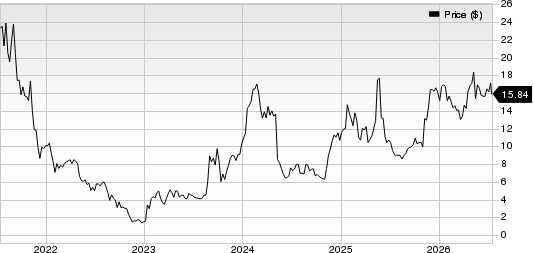

NeuroPace, Inc. Price

NeuroPace, Inc. price | NeuroPace, Inc. Quote

Estimate Trend

NeuroPace has been witnessing a positive estimate revision trend for 2026. Over the past 60 days, the Zacks Consensus Estimate for its loss has narrowed by 1 cent to 54 cents per share.

The Zacks Consensus Estimate for 2026 revenues is pegged at $100.2 million, indicating a 0.2% increase from the year-ago reported numbers.

Key Picks

Some better-ranked stocks from the broader medical space are West Pharmaceutical WST, Intuitive Surgical ISRG and Cardinal Health CAH, each carrying a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

West Pharmaceutical reported first-quarter 2026 earnings per share (EPS) of $2.13, which beat the Zacks Consensus Estimate by 26.8%. Revenues of $844.9 million surpassed the Zacks Consensus Estimate by 8.5%.

West Pharmaceutical has an estimated long-term earnings growth rate of 13.9%. WST’s earnings surpassed estimates in the trailing four quarters, the average surprise being 19.4%.

Intuitive Surgical reported first-quarter 2026 adjusted EPS of $2.50, which beat the Zacks Consensus Estimate by 20.2%. Revenues of $2.77 billion surpassed the Zacks Consensus Estimate by 6.2%.

Intuitive Surgical has an estimated long-term earnings growth rate of 14.3%. ISRG’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 16.8%.

Cardinal Health reported a third-quarter fiscal 2026 adjusted EPS of $3.17, which beat the Zacks Consensus Estimate by 13.2%. Revenues of $60.94 billion missed the Zacks Consensus Estimate by 2.3%.

Cardinal Health has an estimated long-term earnings growth rate of 17%. CAH’s earnings surpassed estimates in the trailing four quarters, the average surprise being 10.3%.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

NeuroPace, Inc. (NPCE): Free Stock Analysis Report

Intuitive Surgical, Inc. (ISRG): Free Stock Analysis Report

Cardinal Health, Inc. (CAH): Free Stock Analysis Report

West Pharmaceutical Services, Inc. (WST): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).