Snap-on Inc. SNA reported solid first-quarter 2026 results, wherein the top and bottom lines surpassed the Zacks Consensus Estimate and grew year over year. Results showed ongoing momentum, along with the ability to effectively manage uncertainty and trade turbulence.

Snap-on’s earnings of $4.69 per share surpassed the Zacks Consensus Estimate of $4.68. The figure increased from adjusted earnings of $4.51 per share in the year-ago quarter.

SNA’s Quarterly Performance: Key Metrics & Insights

Net sales totaled $1.207 billion, up 5.8% from the prior year, and exceeded the Zacks Consensus Estimate of $1.177 billion. Organic sales' rise of 3.4% ($39.2 million) and $26.9 million of positive foreign currency fluctuation aided sales.

The gross profit of $608.3 million rose 5.2% year over year, whereas the gross margin contracted 30 basis points (bps) to 50.4%. Our model expected a gross margin of 50.6%, down 10 bps from the year-ago quarter.

Snap-on’s operating earnings before financial services totaled $250.8 million, up 3.2% year over year. As a percentage of sales, operating earnings before financial services decreased 50 bps to 20.8% in the first quarter.

Consolidated operating earnings (including financial services) were $318.8 million, up 1.7% year over year. As a percentage of revenues, operating earnings fell 80 bps year over year to 24.4%.

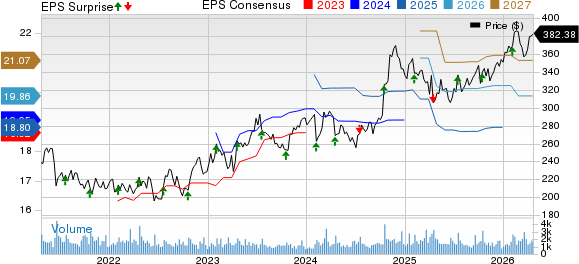

Snap-On Incorporated Price, Consensus and EPS Surprise

Snap-On Incorporated price-consensus-eps-surprise-chart | Snap-On Incorporated Quote

Snap-on’s Segmental Analysis

Sales in the Commercial & Industrial Group edged up 10.8% from the year-ago quarter to $381 million, due to an $11.9 million gain in favorable foreign currency translation and a $25.2 million or 7.1% organic sales rise. The organic rise is mainly owing to increased sales across each of the segment’s operations, driven by improved activity with customers in critical industries and in the specialty torque business. For the first quarter, we expected sales of $359.4 million for the segment.

The Tools Group segment’s sales increased 5% year over year to $486 million. We estimated sales of $462.9 million for the segment. The increase resulted from an organic sales rise of 3.4%, owing to an improvement in sales both in the United States and the segment’s international operations. Also, a $7.2 million benefit from foreign currency translation aided revenues.

The Repair Systems & Information Group segment sales were $485.3 million in the quarter compared with $475.9 million in 2025, primarily reflecting $9.1 million of favorable foreign currency translation. On an organic basis, increased sales of diagnostic and repair information products to independent repair shop owners and managers were offset by lower activity with OEM dealerships, while undercar equipment was essentially flat. We expected sales of $497.3 million for the segment.

Sales in Repair Systems & Information Group improved 2% year over year to $485.3 million, with organic sales growth and a $9.1 million boost from foreign currency translation. Organic sales grew due to increased sales of diagnostic and repair information products to independent repair shop owners and managers. These gains were offset by soft activity with OEM dealerships, while undercar equipment was almost flat. Our estimate for sales from this segment was $468 million.

The Financial Services business’ revenues dipped 1% year over year to $101.1 million. Our estimate for sales from this segment was $104.3 million.

SNA's Financial Snapshot

Snap-on ended the first quarter of 2026 with cash and cash equivalents of $1.75 billion, with shareholders’ equity (before non-controlling interest) of $5.96 billion. The company expects a capital expenditure of $100 million for 2026.

What’s Ahead for Snap-on?

Management expects SNA’s markets and operations to have considerable resilience against the uncertainties of the operating landscape. For 2026, the company expects to continue advancing its core growth strategies, leveraging strengths in automotive repair while expanding into adjacent markets, new geographies and other areas like critical industries. SNA expects an effective tax rate of 22-23% for 2026.

This Zacks Rank #3 (Hold) company’s shares have gained 12.3% over the past three months compared with the industry's 16.1% growth.

Key Picks in the Consumer Discretionary Space

Ralph Lauren Corporation RL, which is a designer and marketer of premium lifestyle products, currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

RL delivered a trailing four-quarter earnings surprise of 9.7%, on average. The Zacks Consensus Estimate for Ralph Lauren’s current financial-year sales indicates growth of 12.4% from the year-ago number.

Boyd Gaming BYD, which is a gaming company, currently carries a Zacks Rank #2 (Buy).

BYD delivered a trailing four-quarter earnings surprise of 11.4%, on average. The Zacks Consensus Estimate for BYD’s current financial-year EPS indicates growth of 2.2% from the year-ago number.

Columbia Sportswear Company COLM, which is a marketer and distributor of outdoor and active lifestyle apparel, footwear, accessories and equipment, currently carries a Zacks Rank of 2.

The Zacks Consensus Estimate for COLM’s current financial-year sales is expected to rise 2% from the corresponding year-ago reported figure. COLM delivered a trailing four-quarter earnings surprise of 25.2%, on average.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Snap-On Incorporated (SNA): Free Stock Analysis Report

Columbia Sportswear Company (COLM): Free Stock Analysis Report

Ralph Lauren Corporation (RL): Free Stock Analysis Report

Boyd Gaming Corporation (BYD): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).