Headquartered in Frisco, Texas, Public Storage (PSA) has built a business around life’s extra baggage and turned it into a real estate empire worth roughly $53.6 billion. The company owns and operates more than 3,500 self-storage facilities across 40 U.S. states, offering month-to-month rentals for personal and business customers who need extra breathing room.

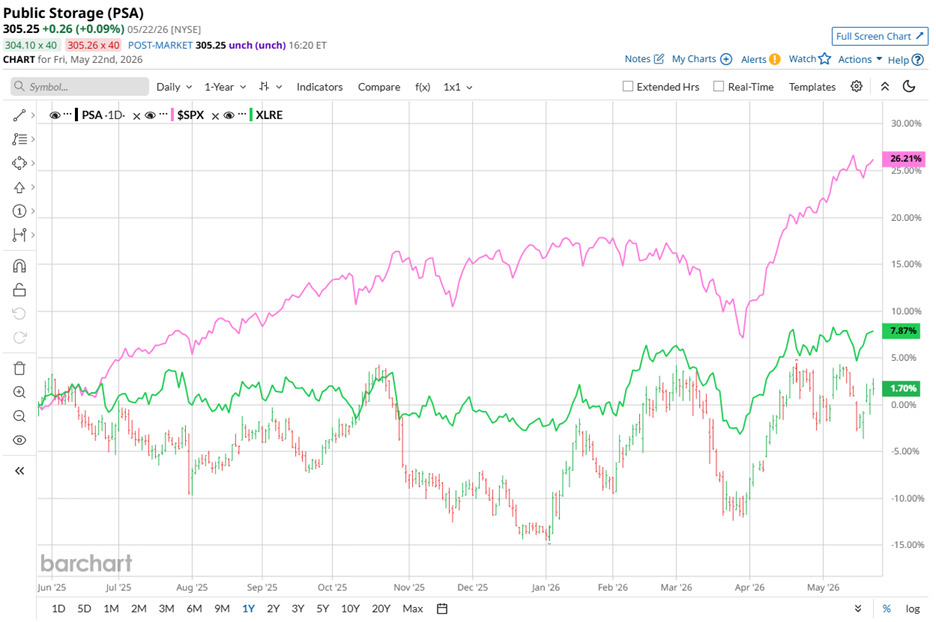

Despite its massive footprint, the roughly $53.6 billion market cap company spent much of the past year moving at its own pace while the broader market ran like a horse. Over the last 52 weeks, PSA stock gained 3.2%, which looks modest beside the 27.9% rally delivered by the S&P 500 Index ($SPX) during the same stretch

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

This year, however, the script flipped in Public Storage’s favor. Its shares climbed 17.6% year-to-date (YTD) while the broader index advanced 9.2%, suggesting the stock has started finding firmer ground as investors circle back toward defensive real estate plays.

The broader property sector has also regained traction. The State Street Real Estate Select Sector SPDR ETF (XLRE) advanced 9.7% over the past 52 weeks and added another 10.4% on a YTD basis. Even against the improving sector backdrop, PSA’s YTD rally stands out, highlighting the stock’s stronger recent performance within the real estate space.

www.barchart.com

www.barchart.com The improving sentiment received another boost on May 6 after Public Storage announced a regular quarterly common dividend of $3 per common share. The board also approved dividends tied to several preferred share series, with all payments scheduled for June 30, for shareholders on record as of June 15.

Investors wasted little time reacting because PSA stock rose 3.4% the same day, proving that dependable payouts still speak louder than fancy headlines when markets grow uneasy.

Public Storage currently pays an annual dividend of $12 per share, giving the stock a healthy 3.93% yield that continues attracting income focused investors looking for steadier ground in a market that often changes direction at the drop of a hat.

Turning to earnings, analysts expect Public Storage’s fiscal year 2026 diluted EPS, ending in December, to decline marginally year over year to $16.89. Even so, the company has continued outperforming expectations with notable consistency. It surpassed consensus EPS estimates in each of the past four quarters.

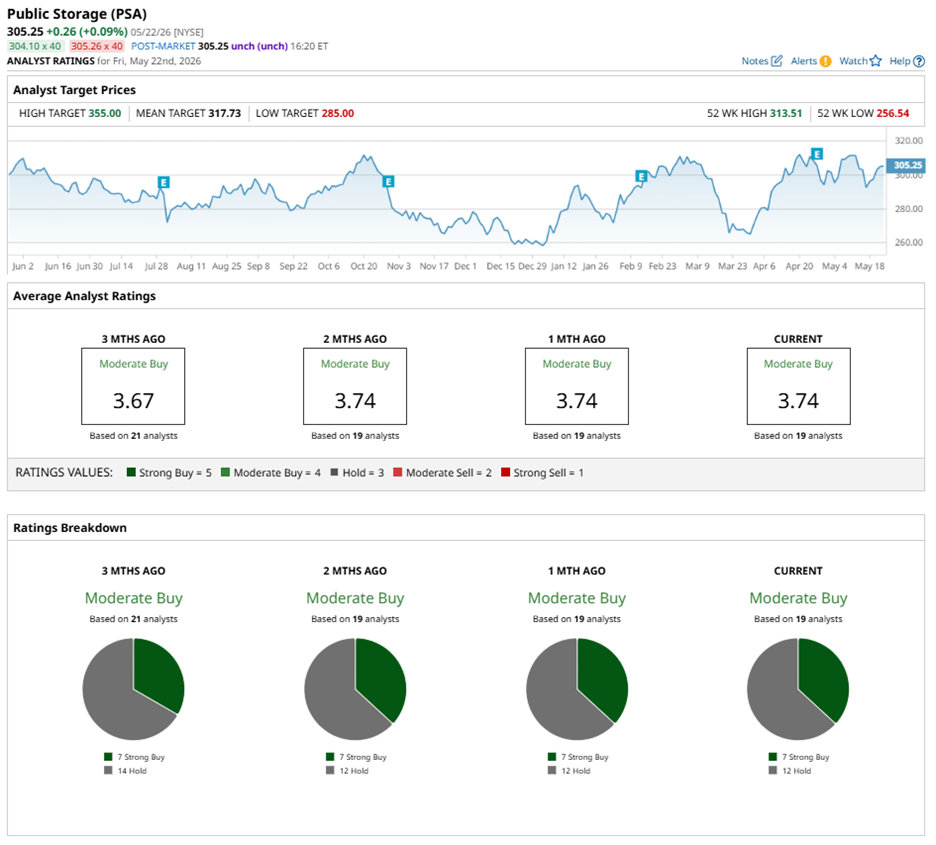

Wall Street currently assigns PSA stock an overall “Moderate Buy” rating. Among the 19 analysts covering the shares, seven recommend “Strong Buy,” while the remaining 12 maintain “Hold” ratings.

www.barchart.com

www.barchart.com The current analyst sentiment has remained unchanged from three months ago, when seven analysts also rated the stock a “Strong Buy.”

Meanwhile, Barclays analyst Brendan Lynch trimmed PSA’s price target to $349 from $352 on May 7 while maintaining an “Overweight” rating on the shares.

Even with the slight reduction, analysts still see meaningful upside ahead. The mean price target of $317.73 implies potential upside of 4.1%, while the Street-high target of $355 represents a gain of 16.3% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Qualcomm Stock Is the Sleeping Giant of the AI Revolution. It’s Starting to Wake Up. Wall Street Is Warming Back Up to CoreWeave Stock. Long-Term Demand Is Helping. Palantir’s AI Surge Meets Market Correction. Buy the PLTR Stock Dip Now. 1 Outstanding AI Stock You’ll Regret Ignoring 10 Years From Now