Commodity complex bears were in control of the various market sectors overnight through early Friday morning.

The Livestock sector doesn't trade overnight, with the spotlight on both cattle markets Friday given expanded daily trade limits.

Don’t Miss a Day: From crude oil to coffee, sign up free for Barchart’s best-in-class commodity analysis.

The Grains sector was also in the red on the first day of the latest Goldman Roll, moving weather forecasts and new-crop markets to center stage.

Morning Summary: There wasn’t a lot of green in the commodity complex early Friday morning with the Barchart Futures Market Heat Map (slide 2) showing only 2 sectors now donning some shade of red. Financials (US Treasury futures) were showing a fractional gain, to go along with lower US Treasury yields and Livestock don’t trade overnight so the sector still reflected Thursday’s 0.6% rally. Speaking of activity out in the Barn, it will be interesting to see what happens with both cattle markets given today’s expanded limits of $16 in feeders and $12.75 in live. Cash cattle have been volatile so far this week with initial reports of $255 trading, down $2 from last week, before $256 being passed by sellers at midweek. It should be noted the June issue (LEM26) closed Thursday at $249.175 meaning national average basis is roughly $8 over this week. While this sounds strong, it’s near the previous 5-year average for this week. As for feeders, my friend in the industry has been reporting lower cash markets throughout the week, putting the spotlight on this morning’s numbers following yesterday’s limit up close in the futures market. As I discussed with him Thursday, both cattle markets are bearish technically but bullish fundamentally. Will Market Rule #6 (Fundamentals win in the end) come into play to close out the week?

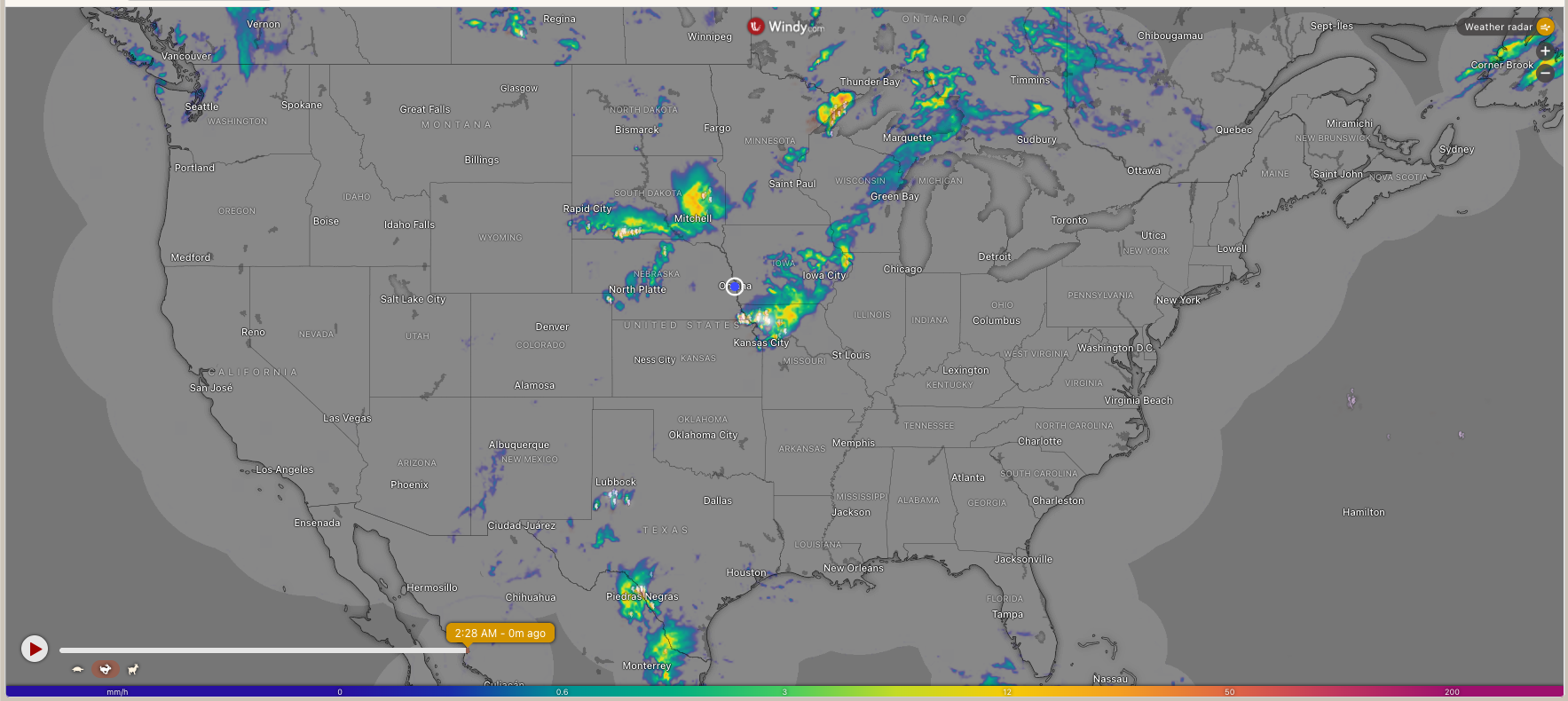

Corn: The corn market was lower pre-dawn Friday, the first day of the latest round of the Goldman Roll. Someone smarter than I will likely know if long-only funds have to be in the nearby futures contract, and if so, this is an awkward time of year for corn (and the oilseed sub-sector) given the first deferred issue is the hybrid – part old-crop, part new-crop – September. July (ZCN26) was down 2.5 cents at this writing after slipping as much as 4.0 cents overnight on light trade volume of 20,000 contracts. Recall July closed 7.0 cents lower Thursday, after losing as much as 10.0 cents, followed by the National Corn Index coming in 6.75 cents lower for the day. This put national average basis at 34.75 cents under July futures as compared to the previous 5-year low weekly close for this week of 39.75 cents under July. As for new-crop, December (ZCZ26) dropped as much as 3.75 cents overnight while registering 16,000 contracts changing hands and was down 2.25 cents at this writing. A look at early morning radar (slide 3) shows a rain system stretching across Iowa, with another following in its tracks. The bottom line is weather, both current and forecast, looks favorable for the weekend.

Soybeans: The oilseed sub-sector was – well – interesting early Friday morning, for lack of a better word. After screaming higher at midweek, both canola and soybeans oil were under continued pressure pre-dawn with the July canola contract down $12.50 (1.6%) at this writing. Meanwhile, new-crop November was off $10 to start the day. Over in bean oil we see July down 0.4 cent (0.5%) while the December issue, the next contract with the most open interest, was down 0.25 cent (0.3%). Given this, one might jump to the conclusion diesel fuel was hit hard overnight, but that isn’t the case. A look at the quote screen shows the spot-month distillates contract down 1.8 cents (0.5%) after sliding as much as 4.1 cents. Over in soybeans we see July (ZSN26) down 1.0 cent after losing as much as 34.0 cents Thursday before closing 24.5 cents lower for the day. Last night saw the National Soybean Index come in at $10.70, down about 24.0 cents from Wednesday, putting national average basis at 55.0 cents under July futures with the previous 10-year average weekly close for this week at 57.0 cents under July. Despite Watson being fed the same extended forecast, the new-crop November soybean contract (ZSX26) was up 1.5 cents.

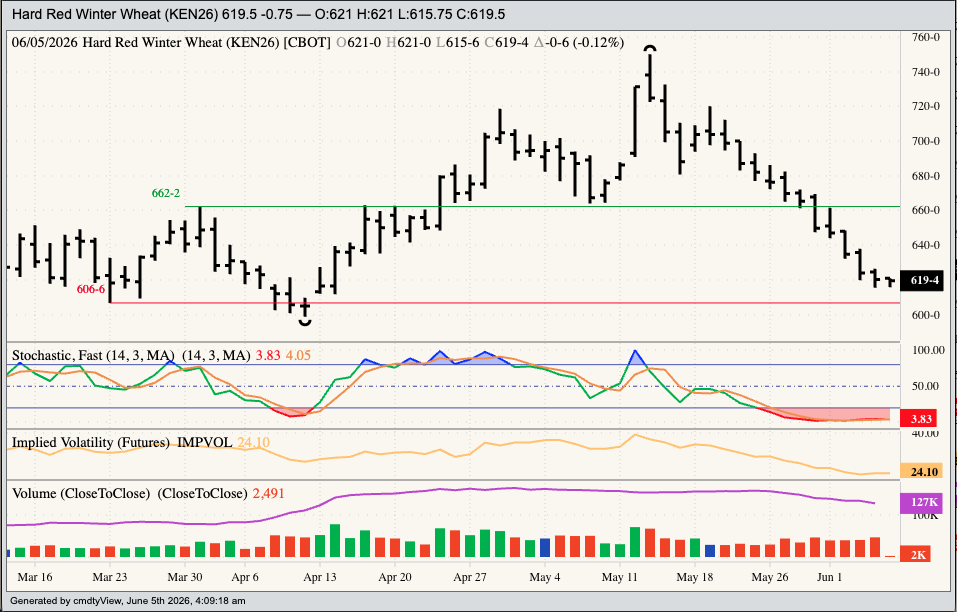

Wheat: And then there’s the wheat sub-sector. With HRW harvest still struggling to make its way north out of Texas due to wet weather across parts of the US Southern Plains growing area, the July HRW issue (KEN26) is on a string of 11 straight lower daily closes. Early Friday morning finds July down 2.75 cents after sliding as much as 4.5 cents overnight on light trade volume of about 2,500 contracts. It would not be surprising to see July break its string heading into the weekend, particularly with daily stochastics (a technical momentum indicator) running in the low single digits indicating the issue is sharply oversold. But that and a crisp $5 bill might buy you a small black coffee from your local barista. The meltdown in HRW has been spectacular, putting the spotlight on Friday afternoon’s Commitments of Traders report that is expected to show the net-short futures position increased dramatically. The same could be said for SRW, though the July issue (ZWN26) ticked back into the green as I was writing this segment. Overnight trade saw July lose as much as 3.5 cents before uncovering a light round of short covering. Heading into Friday’s session the September-December futures spread covered a bearish 77% calculated full commercial carry.

On the date of publication, Darin Newsom did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Why Was the Commodity Sector Seeing Red Early Friday Morning? Bulls Are Losing Their Grip as Cattle Collapses. What to Watch. Cattle Collapsed on Thursday. More Pain Could Be in Store. Grains, Livestock, and Geopolitics: How to Read What the Ag Markets Are Actually Telling Us