Acuity Brands, Inc. AYI is scheduled to announce second-quarter fiscal 2026 results on April 2, before the opening bell.

In the last reported quarter, the company’s adjusted earnings and revenues surpassed the Zacks Consensus Estimate by 3.8% and 0.5%, respectively, and increased from the prior-year quarter by 20% and 18%.

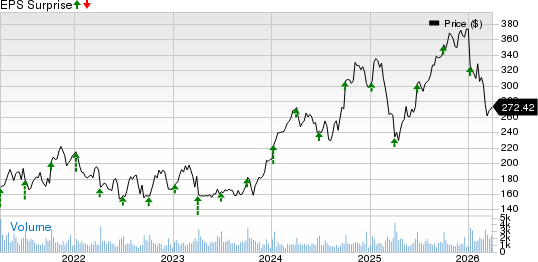

Acuity Brands beat earnings estimates in the trailing 22 quarters, with the last four quarters’ average surprise being 8%.

How Are Estimates Placed for AYI Stock?

For the quarter to be reported, the Zacks Consensus Estimate for earnings per share (EPS) has remained unchanged at $4.11 in the past 60 days. However, the estimated figure indicates an increase of 10.2% from $3.73 per share reported in the year-ago quarter.

Acuity, Inc. Price and EPS Surprise

Acuity, Inc. price-eps-surprise | Acuity, Inc. Quote

The consensus mark for revenues is pegged at $1.09 billion, indicating an 8.7% increase from the year-ago reported figure.

Factors to Shape AYI’s Q2 Results

Revenues

Acuity Brands is expected to report year-over-year growth in revenues for the fiscal second quarter, primarily fueled by the continued expansion of its Acuity Intelligent Spaces (AIS) segment. This growth is heavily supported by the integration of the acquired QSC, LLC and sustained mid-teens organic growth from the Atrius and Distech businesses. In contrast, the Acuity Brands Lighting (ABL) segment is expected to deliver modest growth, aided by backlog execution and resilience in the independent sales network, despite operating in a subdued demand environment.

The company’s ongoing focus on innovation and product development remains a key growth lever. Recent launches, including the EAX Area Luminaire product family by Lithonia, alongside continued traction in integrated lighting and electronics solutions, are helping ABL expand into new markets. Additionally, recognition of its Nightingale brand for patient-centric design underscores the strength of its differentiated product portfolio.

Segment-wise, for the to-be-reported quarter, our model predicts total ABL segment (contributed 78.3% to the first quarter of fiscal 2026 net sales) revenues to increase 1.9% year over year to $856.7 million. Within the ABL segment, we expect Independent Sales Network and Retail revenues to increase 3.4% and 1.3%, while Corporate Account, Direct Sales Network and Other revenues are anticipated to decrease 6.4%, 1.1% and 3.6%, respectively, year over year.

Our model predicts the AIS segment’s (contributed 22.5% to the first quarter of fiscal 2026 net sales) revenues in the fiscal second quarter to surge 45.8% year over year to $250 million. Management has highlighted the strength of the AIS portfolio, particularly its ability to deliver integrated, cross-sell solutions, such as combining Distech’s sensing technologies with the Q-SYS platform to enable autonomous, intelligent space environments.

Although AIS may also experience some seasonal moderation in the second quarter due to backlog normalization, the segment remains well-positioned to outgrow the market and gain share, supported by its disruptive capabilities and expanding capabilities.

Margins

The bottom line is likely to have been supported by continued cost discipline, productivity improvements and a favorable business mix, with the higher-margin AIS segment contributing meaningfully to overall profitability. Strategic pricing actions and ongoing operational efficiencies are likely to have helped mitigate external pressures, including tariffs, while strong cash flow generation and disciplined capital allocation should further support earnings growth.

However, these tailwinds are expected to be partially offset by persistent softness in the lighting market, tariff-related cost volatility and the normalization of previously elevated backlog levels, which may weigh on near-term growth momentum.

We expect the company’s adjusted EBITDA to increase 9.9% year over year in the fiscal second quarter to $194 million. Adjusted operating margin is projected to remain stable at 16.2% year over year, while total expenses are anticipated to decline to $7 billion from $7.9 billion in the prior-year quarter.

What Our Model Indicates for AYI Stock

Our proven model does not conclusively predict an earnings beat for Acuity Brands this time around. The company does not have the right combination of the two key ingredients, a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold), to increase the odds of an earnings beat.

AYI’s Earnings ESP: The company has an earnings ESP of 0.00%. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

AYI’s Zacks Rank: The stock currently has a Zacks Rank #3. You can see the complete list of today’s Zacks #1 Rank stocks here.

Stocks With the Favorable Combination

Here are some companies in the Zacks Business Services sector that, according to our model, have the right combination of elements to post earnings beats in the quarter to be reported.

Coherent Corp. COHR has an Earnings ESP of +2.70% and currently carries a Zacks Rank of 2.

COHR’s earnings beat estimates in each of the trailing four quarters, with the average surprise being 7.7%. Coherent’s earnings for the third quarter of 2026 are expected to increase 53.9%.

ESCO Technologies Inc. ESE presently has an Earnings ESP of +2.81% and a Zacks Rank of 2.

ESE’s earnings beat estimates in each of the trailing four quarters, with an average surprise being 24.2%. ESCO’s earnings for the second quarter of 2026 are expected to increase 28.9%.

APi Group Corporation APG currently has an Earnings ESP of +0.88% and a Zacks Rank of 3.

APG’s earnings beat estimates in each of the trailing four quarters, with the average surprise being 6.6%. APi Group’s earnings for the first quarter of 2026 are expected to increase 20%.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

ESCO Technologies Inc. (ESE): Free Stock Analysis Report

Coherent Corp. (COHR): Free Stock Analysis Report

Acuity, Inc. (AYI): Free Stock Analysis Report

APi Group Corporation (APG): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).