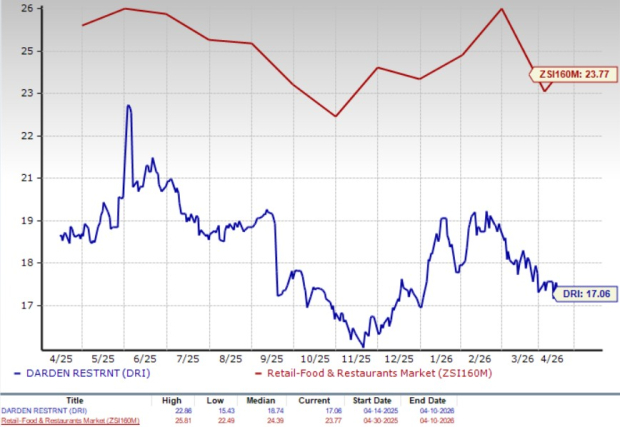

Darden Restaurants, Inc. DRI is trading at a valuation that may catch investors’ attention. The stock currently carries a forward 12-month price-to-earnings (P/E) ratio of 17.06, notably below the restaurant industry average of 23.77. This discount suggests that the market is taking a measured view of the company, despite its strong brand portfolio and scale.

P/E (F12M)

Image Source: Zacks Investment Research

Looking at performance, Darden’s shares have shown relative resilience. Over the past six months, the stock has gained 2.9%, slightly trailing the broader restaurant industry’s 3.1% increase. It has also lagged the S&P 500’s 3.7% rally, indicating that investors have been favoring higher-growth opportunities.

Within the peer group, performance has been mixed. Domino's Pizza, Inc. DPZ and Chipotle Mexican Grill CMG have seen their shares decline 13.7% and 19%, respectively, while Restaurant Brands International QSR has posted a gain of 11.2%. Against this backdrop, Darden’s steadier performance highlights its defensive appeal, even as the stock remains modestly undervalued.

Price Performance

Image Source: Zacks Investment Research

Factors Supporting Darden Stock

Darden’s recent performance highlights strong underlying momentum, driven primarily by consistent same-restaurant sales growth and clear outperformance compared with the broader industry. The company delivered 4.2% comps, significantly ahead of industry benchmarks, with all major segments contributing positively. This strength reflects solid execution across brands, supported by improved guest satisfaction and steady traffic trends. Importantly, both increased customer frequency and new guest additions are contributing to growth, indicating that demand is broad-based rather than dependent on a single lever.

Another key tailwind is Darden’s focus on value-driven innovation and operational discipline. Initiatives like Olive Garden’s lighter portion menu and promotional offerings are resonating well with customers, driving higher visit frequency and improved value perception. At the same time, brands like LongHorn Steakhouse continue to benefit from strong positioning around quality and affordability, especially as consumers seek better value compared with grocery alternatives. These efforts, combined with effective marketing and menu optimization, are helping the company maintain traffic even in a competitive environment.

Additionally, Darden’s operational efficiency and cost management provide a strong foundation for earnings growth. Labor productivity is improving due to lower employee turnover and better retention, which reduces hiring and training costs while enhancing service quality. The company is also benefiting from scale advantages, supply-chain capabilities and disciplined capital allocation, including steady shareholder returns through dividends and buybacks. With pricing flexibility still available after years of underpricing inflation, Darden is well positioned to protect margins while continuing to invest in growth.

Factors Weighing on Darden Stock

On the flip side, margin pressures remain a concern. Elevated commodity costs, particularly beef inflation, have increased food and beverage expenses, while pricing has lagged inflation for much of the year. This mismatch has weighed on restaurant-level margins, even as the company continues to invest in value offerings and marketing. Although pricing is expected to catch up, near-term profitability remains exposed to cost volatility.

Additionally, external factors and operational disruptions pose risks. Weather-related impacts temporarily affected sales and broader macro uncertainty has led management to maintain a cautious outlook. The company is also rationalizing underperforming brands, including closing and converting Bahama Breeze locations, which highlights portfolio challenges. While these actions may strengthen the business long term, they reflect near-term headwinds that could limit upside despite strong operating fundamentals.

DRI’s Growth Projection Encourages

Over the past 30 days, the Zacks Consensus Estimate for earnings per share for fiscal 2026 and 2027 has increased 3 cents to $10.61 and decreased 3 cents to $11.38, respectively. The Zacks Consensus Estimate for DRI’s fiscal 2026 and 2027 earnings per share indicates year-over-year increases of 11.1% and 7.3%, respectively.

Image Source: Zacks Investment Research

The consensus estimate for revenues is pegged at $13.21 billion and $13.69 billion for fiscal 2026 and 2027, respectively, implying year-over-year improvements of 9.4% and 3.7%.

Wrapping up

Darden remains a stable and well-executed business, supported by steady demand, strong brand positioning and effective cost management, making it suitable for investors to hold. The company continues to benefit from consistent traffic, value-driven offerings and operational efficiency.

However, despite its discounted valuation, near-term margin pressures from higher input costs and some macro uncertainty limit upside potential. As a result, existing investors can stay invested for steady growth and returns, while new investors may wait for a more attractive entry point.

DRI currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Quantum Computing Stocks Set To Soar

Artificial intelligence has already reshaped the investment landscape, and its convergence with quantum computing could lead to the most significant wealth-building opportunities of our time.

Today, you have a chance to position your portfolio at the forefront of this technological revolution. In our urgent special report, Beyond AI: The Quantum Leap in Computing Power , you'll discover the little-known stocks we believe will win the quantum computing race and deliver massive gains to early investors.

Access the Report Free Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Chipotle Mexican Grill, Inc. (CMG): Free Stock Analysis Report

Domino's Pizza Inc (DPZ): Free Stock Analysis Report

Darden Restaurants, Inc. (DRI): Free Stock Analysis Report

Restaurant Brands International Inc. (QSR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).