Celestica, Inc. CLS and Sanmina Corporation SANM are two prominent players in the electronics manufacturing services industry. Celestica is one of the largest electronics manufacturing services companies in the world, primarily serving original equipment manufacturers, cloud-based and other service providers and enterprises from several industries.

Sanmina emphasizes engineering and fabricating complex components and also providing complete end-to-end supply chain solutions to Original Equipment Manufacturers across various end markets.

With domain-specific expertise in core areas, both Celestica and Sanmina are strategically positioned in the EMS landscape and have the wherewithal to cater to the evolving demands of business enterprises. Let us delve a little deeper into the companies’ competitive dynamics to understand which of the two is relatively better placed in the industry.

The Case for Sanmina

The company is benefiting from healthy traction in the Integrated Manufacturing Solutions segment. In the first quarter of 2026, the segment generated $2.79 billion in revenues, up 72.2% year over year. IMS’ growth is directly tied to the AI data center capex cycle. Hyperscalers and enterprises continue expanding data center capacity to support growing AI workloads. This trend is driving strong demand for enterprise storage and high-performance switches. The company has also highlighted growing momentum in advanced optical packaging. This is an area becoming increasingly important as AI data centers require faster and more efficient data transmission between servers, processors and networking equipment.

However, intensifying competition in the electronics manufacturing services can impact Sanmina’s net sales. The company has multiple competitors, including Foxconn, Jabil, Celestica and Flex, and some of them have significantly greater resources.

The company’s strength lies in its disciplined capital allocation and efficient operations, supported by strong cost control, stable margins and focus on higher-margin programs. This helps to generate a steady cash flow, supports growth investments and enhances long-term shareholder value.

In the first quarter of fiscal 2026, Sanmina generated $178.7 million of net cash from operating activities compared with $63.9 million in the year-ago quarter. As of Dec. 27, 2025, the company had $1.42 billion in cash and cash equivalents and $ 2 billion in long-term debt. During the quarter, the company repurchased 0.5 million shares for $79 million. SANM’s current ratio (a measure of liquidity) stood at 1.70 at the end of the first quarter of fiscal 2026. A current ratio of more than 1 suggests the company is well-positioned to pay off its short-term debt obligations.

Power systems supporting AI data centers and other complex hardware ecosystems are also a major growth driver for the company. It is expanding its manufacturing capabilities in Houston, TX, to develop a comprehensive range of leading-edge energy products to support the growing demand. Such a strategic approach bodes well for long-term growth.

The Case for Celestica

Celestica boasts a robust portfolio of enterprise-level data communications and information processing infrastructure products, such as routers, switches, data center interconnects, edge solutions and servers. Such a comprehensive product suite, combined with a strong focus on innovation, is allowing Celestica to tap into the expanding AI infrastructure market. The company is actively collaborating with other industry leaders such as AMD and Broadcom to further augment its portfolio offerings.

In the fourth quarter of 2025, Celestica generated $250.6 million in cash from operations compared with $143.4 million in the year-ago quarter. Free cash flow was $155.9 million, up 62.7% year over year. This accentuates efficient capital management and implies that the company is well-positioned to invest in growth initiatives, as well as pay debt and dividends.

As of Dec. 31, 2025, the company had $595.6 million in cash and cash equivalents, with the long-term portion of borrowings under the credit facility and finance lease obligations of $750.5 million. Celestica’s strong liquidity better positions it to navigate economic downturns and capitalize on emerging growth opportunities in the electronics manufacturing service industry.

However, Celestica is exposed to significant customer concentration risk. The company’s largest 10 customers generated approximately 79% of total revenues in fiscal 2025. It faces stiff competition in the EMS industry from other major players such as Jabil, Inc. JBL and Flex Ltd. FLEX. Flex is aggressively moving into the high-growth data center market. For the third quarter of fiscal 2026, Flex reported continued strong growth in its data center business, driven by rapidly expanding compute and AI workloads. Jabil is also expanding into the AI infrastructure market. Such growing competition in the market poses a threat to Celestica’s AI data center expansion initiatives.

How Do Zacks Estimates Compare for CLS & SANM?

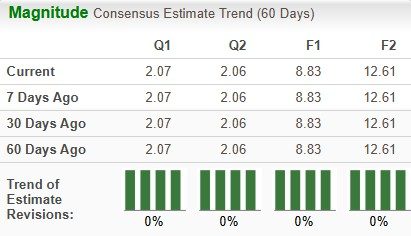

The Zacks Consensus Estimate for Celestica’s full-year sales implies year-over-year growth of 37.42%, while that of EPS suggests growth of 45.95%. The EPS estimates have remained unchanged for 60 days.

Image Source: Zacks Investment Research

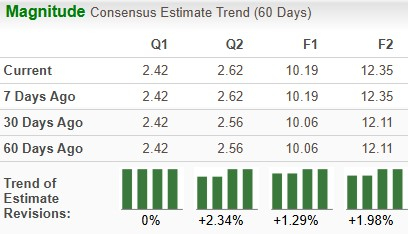

The Zacks Consensus Estimate for Sanmina’s 2025 sales and EPS implies year-over-year growth of 68.89% and 68.71%, respectively. The EPS estimates have increased over the past 60 days.

Image Source: Zacks Investment Research

Price Performance & Valuation of CLS & SANM

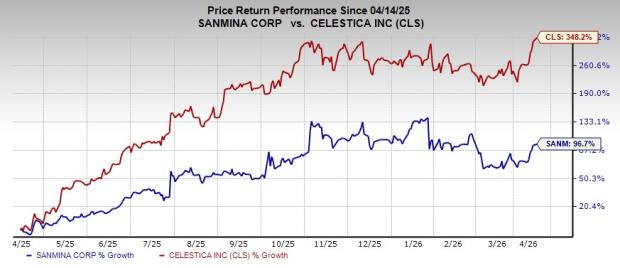

Over the past year, Celestica has gained 348.2%, while SANM has gained 96.7% over the same period.

Image Source: Zacks Investment Research

SANM looks more attractive than Celestica from a valuation standpoint. Going by the price/earnings ratio, Sanmina’s shares currently trade at 13.03 forward earnings, lower than 35.5 for Celestica.

Image Source: Zacks Investment Research

CLS or SANM: Which is a Better Pick?

Celestica and Sanmina carry a Zacks Rank #3 (Hold) each. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Both companies are witnessing solid momentum across several verticals. Robust portfolio offerings and solid cash flow growth are major tailwinds for both companies. Celestica and Sanmina are expected to improve revenue in the upcoming quarters; however, revenue growth expectations of SANM far outpace the expectations of Celestica. Sanmina also shows a stronger upward estimate revision. With an attractive valuation, Sanmina seems to be a better investment option at the moment.

Quantum Computing Stocks Set To Soar

Artificial intelligence has already reshaped the investment landscape, and its convergence with quantum computing could lead to the most significant wealth-building opportunities of our time.

Today, you have a chance to position your portfolio at the forefront of this technological revolution. In our urgent special report, Beyond AI: The Quantum Leap in Computing Power , you'll discover the little-known stocks we believe will win the quantum computing race and deliver massive gains to early investors.

Access the Report Free Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Jabil, Inc. (JBL): Free Stock Analysis Report

Flex Ltd. (FLEX): Free Stock Analysis Report

Celestica, Inc. (CLS): Free Stock Analysis Report

Sanmina Corporation (SANM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).