Roku ROKU is a leading connected TV platform that generates revenues primarily through advertising and content distribution on its operating system. Alphabet GOOGL dominates digital ads globally, with YouTube emerging as a major force in streaming and connected TV advertising.

Both companies are deeply tied to the rise of ad-supported streaming, benefiting from the rapid shift of viewers and advertisers toward connected TV. Roku monetizes engagement through its platform and The Roku Channel, while Alphabet capitalizes on YouTube’s massive global reach and sophisticated ad ecosystem.

This positions both players in direct competition to capture a larger share of the expanding streaming advertising market, projected to grow at a 21.5% CAGR through 2030, per the industry report. The massive opportunity bodes well for both Roku and Alphabet.

Let us delve deeper to determine which is a better investment now.

The Case for ROKU Stock

Roku’s streaming advertising business remains its primary growth engine, driven by scale, first-party data and platform monetization. The company’s Platform revenues grew 18% year over year to $4.145 billion in 2025, supported by strong video advertising demand and streaming distribution, and are expected to grow another 18% to $4.89 billion, with first-quarter growth projected to exceed 21%.

This growth is increasingly profitable, with gross margins expected to remain robust at 51%-52% in 2026, underscoring the scalability of Roku’s ad-driven model. With 145.6 billion streaming hours, the company continues to generate substantial ad inventory, reinforcing its leadership in connected TV (CTV).

Roku benefits from its massive reach with more than 90 million streaming households globally and first-party data, enabling targeted advertising and superior monetization. Its open ad ecosystem, integrated with platforms like The Trade Desk and Amazon DSP, enhances demand access and pricing flexibility. The Roku Channel’s position as a leading free ad-supported streaming TV (FAST) platform further strengthens engagement and ad supply.

The shift from linear TV to CTV, particularly among SMBs (a $600B opportunity), remains a key tailwind. Roku Ads Manager and AI-driven tools are lowering entry barriers, while international markets (Mexico, Canada and Brazil) provide incremental upside. Expanding programmatic capabilities should further improve fill rates and yields. Strategic moves like the Frndly TV acquisition support a hybrid subscription-ad model, enhancing engagement and monetization depth.

The Case for GOOGL Stock

Alphabet’s streaming advertising exposure is primarily driven by YouTube’s ad-supported ecosystem, which remains a major contributor to its broader advertising business.

YouTube continues to scale as a dominant streaming platform, generating over $60 billion in combined ads and subscription revenues in 2025, reflecting strong monetization and user engagement. Ad revenues alone grew 9% year over year in the fourth quarter of 2025, highlighting resilient demand for video advertising. The platform benefits from Alphabet’s advanced AI-driven ad targeting and measurement capabilities, improving advertiser ROI and campaign effectiveness. Also, YouTube’s leadership in living-room streaming and rising engagement (e.g., podcasts, live events) strengthens its position in connected TV advertising.

Growth in connected TV and ad-supported streaming presents a significant tailwind. Increasing consumption of long-form content on TVs and the expansion of YouTube TV and NFL Sunday Ticket offerings provide incremental ad inventory and monetization avenues.

Alphabet remains highly dependent on advertising, which accounted for over 70% of total revenues in 2025, exposing it to macroeconomic cycles and fluctuations in advertising spending. Heavy investments in AI infrastructure and content ecosystems support long-term ad monetization but increase costs and execution risks.

ROKU Shares Outperform GOOGL

Performance metrics reinforce Roku’s strength, with its shares outperforming Alphabet over the past month — rising 8.6% compared with Alphabet’s 5.1% gain — highlighting stronger near-term investor confidence in Roku’s growth trajectory.

Roku’s recent outperformance over Alphabet is supported by strengthening fundamentals. The company is benefiting from robust ad-driven Platform growth, faster expansion in video advertising than the broader market and rising user engagement. In contrast, Alphabet’s performance has been relatively muted, with slower YouTube ad growth, declining Network ad revenues and AI monetization still in its early stages.

ROKU and GOOGL Stock’s Performance

Image Source: Zacks Investment Research

Valuation: ROKU Is Cheaper Than GOOGL

From a valuation standpoint, ROKU looks more attractively valued, trading at a forward Price/Sales ratio of 2.67X compared with GOOGL at 9.06X, which appears relatively expensive. Further, Roku and Alphabet are trading at a premium, as suggested by their Value Score of F and D, respectively. ROKU’s lower valuation offers investors a more reasonable entry point, making it a more appealing option at current levels, supported by its faster-growing, high-margin Platform segment.

ROKU and GOOGL Valuation

Image Source: Zacks Investment Research

Roku Leads Alphabet in Earnings Growth Outlook

Roku’s earnings outlook appears significantly stronger compared to Alphabet’s relatively modest growth.

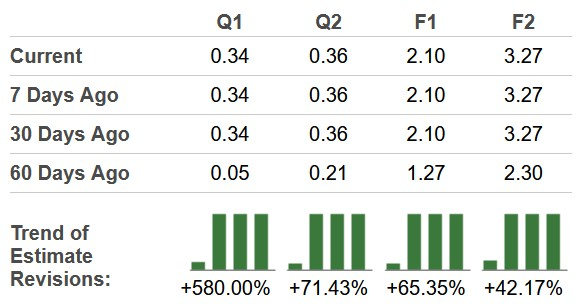

The Zacks Consensus Estimate for Roku’s 2026 earnings is pegged at $2.10 per share, unchanged over the past 30 days, indicating robust growth of 255.93% over its 2025 reported figure.

Image Source: Zacks Investment Research

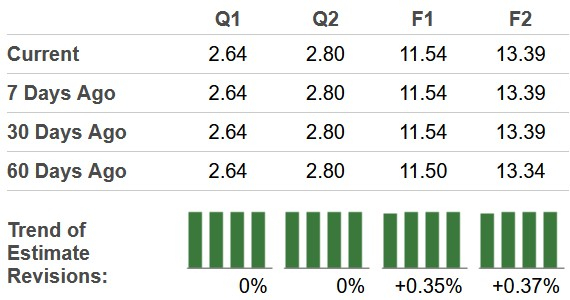

In contrast, the consensus mark for Alphabet’s 2026 earnings stands at $11.54 per share, stable over the past 30 days, suggesting a comparatively moderate growth of 6.75% over 2025.

Image Source: Zacks Investment Research

Both ROKU and GOOGL’s earnings beat the Zacks Consensus Estimate in all the trailing four quarters. However, Roku’s higher average earnings surprise of 97.81%, compared to Alphabet’s 20.82%, underscores the superiority and consistency of its earnings outperformance.

Conclusion: ROKU Is the Better Investment Right Now

Roku emerges as the better investment right now, supported by superior growth prospects, expanding platform monetization and a cheaper valuation. While Alphabet offers stability, Roku’s accelerating CTV ad momentum and earnings trajectory make it the more compelling, growth-driven pick.

Currently, ROKU sports a Zacks Rank #1 (Strong Buy), while GOOGL carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

SeeWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Alphabet Inc. (GOOGL): Free Stock Analysis Report

Roku, Inc. (ROKU): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).