Citigroup, Inc. C kicked off 2026 with a solid start. Its first-quarter 2026 earnings and revenues easily topped the Zacks Consensus Estimate. This reflects solid execution of its turnaround strategy. The bank posted its highest quarterly revenues in a decade, driven by growth across all five divisions. Trading and dealmaking businesses performed particularly well, benefiting from increased market volatility.

The market responded positively following the strong quarterly results. Shares of C climbed modestly and hit a 52-week high of $132.86 in yesterday’s trading session. Aided by its turnaround progress, the stock has emerged as a leading performer in the past year, outperforming industry and its close peers like Wells Fargo WFC and Bank of America BAC.

Price Performance

With such a strong rally, investors now face a familiar dilemma: is it time to lock in gains, or does the C stock still have room to run? Before addressing that question, it is worth taking a closer look at quarterly performance and the key drivers behind its recent strength.

Citigroup’s Standout Q1 Performance — A Closer Look

Net Interest Income (NII) & Non-Interest Revenues: NII rose 12% year over year in the first quarter 2026 to $15.7 billion, while non-interest revenues jumped 17% to $8.9 billion. Wells Fargo’s NII rose 5.2% year over year, while its non-interest income grew 8% in the first quarter. Conversely, Bank of America’s NII (fully taxable-equivalent basis) grew 9% year over year while non-interest income rose 5.2%.

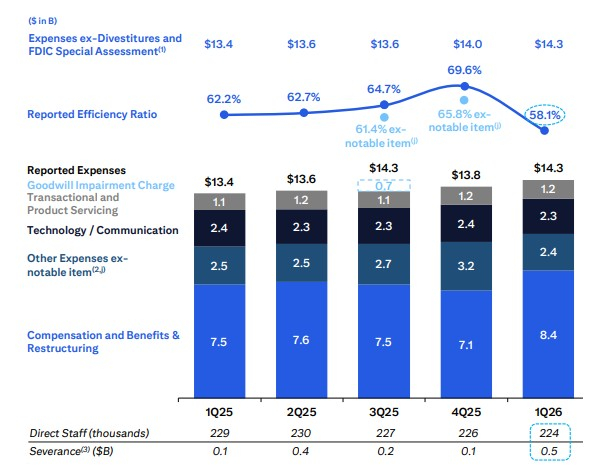

Expenses Rise, but Within Context: Citigroup’s operating expenses increased 7% year over year to $14.3 billion. The rise was primarily driven by higher compensation and benefits expenses, including severance, and the impacts of foreign exchange translation.

Markets & Investment Banking Lead the Charge: The bank’s markets division was a big driver of its solid first-quarter results. The Markets segment’s revenues increased 19% year over year to $7.2 billion, driven by growth in Fixed Income and Equity markets revenues. The company also registered increase of 19% in investment banking (IB) revenues, reflecting growth in Advisory and Equity Capital Markets. BAC’s IB fees (in the Global Banking division) increased 23.6% year over year in the first quarter of 2026.

Asset Quality Shows Signs of Pressure: Provisions for credit losses and benefits, and claims were $2.8 billion in the quarter, up 3% year over year. Total non-accrual loans increased 25% to $3.4 billion.

What's Ahead for Citigroup Stock?

Strategic Transformation Nearing Completion: CEO Jane Fraser continues to advance the company’s multi-year strategy to streamline operations and focus on its core businesses. Since announcing plans in April 2021 to exit consumer banking in 14 markets across Asia and EMEA. During the first quarter 2026 earnings call, management stated that the company has entered the final phase of its divestitures, and 90% of the transformation programs are now at or near the target.

In February 2026, Citigroup completed the sale of its Russia-based banking subsidiary, AO Citibank, to Renaissance Capital. The sale of AO Citibank strengthens the company’s capital position and streamlines its balance sheet. In the same month, C announced agreements with several investors for commitments to purchase an aggregate 24% equity stake in Grupo Financiero Banamex, S.A. de C.V (Banamex), following the divestiture of 25% stake in Banamex to a Mexican business leader in December 2025. The company is now preparing for a planned initial public offering (IPO) of its Mexican consumer, and small and middle-market banking units. Also, as part of its strategy, Citigroup continues to make progress with the wind-down of its Korea consumer banking operations.

These initiatives will free up capital and help the company pursue investments in wealth management and IB operations, which will stoke fee income growth. Supported by these initiatives, Citigroup expects revenues to see a 4-5% compound annual growth rate (CAGR) through 2026.

Improving Margins Through Cost Control: The company is executing on its plan to cut 20,000 jobs by 2026 and has already reduced headcount by more than 10,000 employees, while focusing on process streamlining and automation to reduce manual touchpoints. Citigroup is increasingly deploying artificial intelligence (AI) tools to support these efforts. During the first-quarter 2026 earnings update, management emphasized that AI tool adoption has increased to more than 80%.

Management also emphasized operating efficiency and cost control, even as it continues investing in growth. Expenses rose in the first quarter, but at a slower pace than revenues, improving the efficiency ratio to about 58.1%. The firm is actively reducing costs through restructuring and headcount reductions, while also reallocating resources into technology and AI to drive long-term productivity and revenue gains.

Efficiency Ratio Trend

Given such efforts, the company expects to achieve $2-2.5 billion in annualized run rate savings by 2026. Management continues to target an efficiency ratio of 60% and another year of positive operating leverage in 2026.

Interest Rate Outlook Remains Supportive: NII has been a key contributor to Citigroup’s earnings power, and management expects growth to continue despite a shifting rate environment. Following the initial easing in 2024 and three subsequent rate cuts in 2025, the Federal Reserve has kept interest rates steady so far in 2026. Also, the Fed has indicated one additional rate cut this year. Hence, Citigroup’s NII will continue to grow, given stabilizing funding/deposit costs and improved loan demand.

In first-quarter 2026, NII increased 12% year over year, while NII, excluding Markets, rose 7%. Management continues to expect NII, excluding Markets, to increase 5-6% in 2026.

Liquidity Cushion Powers Shareholder Payouts: C enjoys a strong liquidity position. As of March 31, 2026, Citigroup’s cash and due from banks and total investments aggregated to $467.8 billion, while its total debt (short-term and long-term borrowing) was $379.6 billion.

In 2025, the company hiked its dividend 7.1% to 60 cents per share. In the past five years, it has raised its dividends three times. It has a payout ratio of 30%. It has a dividend yield of 1.9%. Wells Fargo has raised its dividend six times in the past five years, while Bank of America has increased its dividend five times in the past five years.

In January 2025, Citigroup's board of directors approved a $20-billion common stock repurchase program with no expiration date. As of March 31, 2026, $0.5 billion worth of authorization remained available. Supported by a strong capital and liquidity position, its capital distribution activities seem sustainable.

Deteriorating Asset Quality Raises Concerns: Citigroup’s asset quality has been deteriorating. While the company recorded negative provisions in 2021, a substantial jump in provisions was recorded in the years after that because of the worsening macroeconomic outlook. The metric saw a CAGR of 24.5% from 2022 to 2025. C’s asset quality is less likely to improve much in the near term as the impacts of geopolitical pressure, especially in the Middle East, and persistent inflation are likely to put pressure on consumer spending, leading to higher delinquencies.

For 2026, U.S Cards net credit loss (NCL) as a percentage of average loans is expected to be 4-4.5%. U.S. Cards NCL was 3.38% in 2025 and 4.1% in the first quarter of 2026.

C’s Solid Growth Forecast With Attractive Valuation

The Zacks Consensus Estimate for Citigroup’s 2026 and 2027 earnings implies year-over-year rallies of 30.4% and 17.5%, respectively. The estimate for 2026 and 2027 has been revised upward over the past month.

Estimate Revision Trend

Image Source: Zacks Investment Research

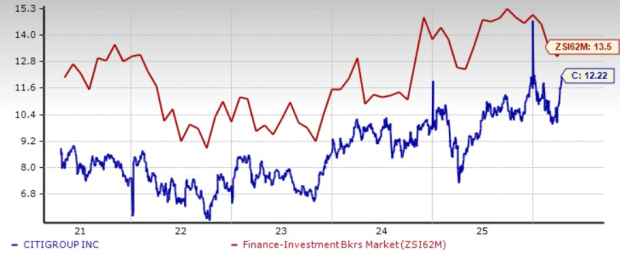

From a valuation standpoint, C trades at a forward price-to-earnings (P/E) ratio of 12.22X, below the industry’s average of 13.5X. Its peers Bank of America and Wells Fargo trade at a forward P/E of 12.02X and 11.21X, respectively.

Price-to-Earnings F12M

Image Source: Zacks Investment Research

Final View on C: Transformation on Track, But Watch the Risks

Citigroup’s recent performance reinforces the view that the turnaround is gaining traction and transformation efforts are beginning to translate into stronger financial performance. The company is also making meaningful progress in simplifying its business model through international divestitures, balance-sheet optimization and continued investment in higher-return areas such as wealth management, technology and IB. These actions should position Citigroup for steadier earnings growth over time and improve its overall competitive position. Another encouraging factor is the company’s solid capital and liquidity profile, which provides flexibility for both business investment and shareholder returns.

That said, the story is not without risks. Asset quality remains an area of concern, as rising non-accrual loans and higher credit costs indicate that pockets of stress persist. Macroeconomic uncertainty, geopolitical tensions and the possibility of weaker consumer health could keep pressure on credit performance in the coming quarters. Hence, investors should exercise caution while initiating new positions on C stock at the current level.

Still, when balancing the positives against the risks, Citigroup appears to remain in a favorable spot. Its strong earnings momentum, disciplined execution, improving efficiency and still-reasonable valuation support the case for patience. For investors who already own the stock, the best approach may be to hold on to C for now, as the company’s restructuring story is still unfolding and further upside could emerge if business momentum and strategic execution remain intact over the next few quarters.

Citigroup currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Picks Stock Most Likely to "At Least Double"

Our experts have revealed their Top 5 recommendations with money-doubling potential – and Director of Research Sheraz Mian believes one is superior to the others. Of course, all our picks aren’t winners but this one could far surpass earlier recommendations like Hims & Hers Health, which shot up +209%.

See Our Top Stock to Double (Plus 4 Runners Up) >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Bank of America Corporation (BAC): Free Stock Analysis Report

Wells Fargo & Company (WFC): Free Stock Analysis Report

Citigroup Inc. (C): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).