Airline stocks have been under pressure since March 2026 as jet fuel prices have surged and investors have reassessed how much margin strain carriers can absorb. Geopolitical conflict and production cuts have pushed jet fuel roughly 130% higher year-over-year (YOY), raising costs across the industry and pressuring names from American Airlines (AAL) to United Airlines (UAL). The U.S. Global Jets ETF (JETS) and most major airline stocks have moved lower as a result.

Delta Air Lines (DAL) has not been immune to the selloff, but it stands out for a few reasons. Demand remains solid, its loyalty program continues to be a powerful profit engine, and the company’s premium-focused strategy gives it more pricing power than many rivals.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

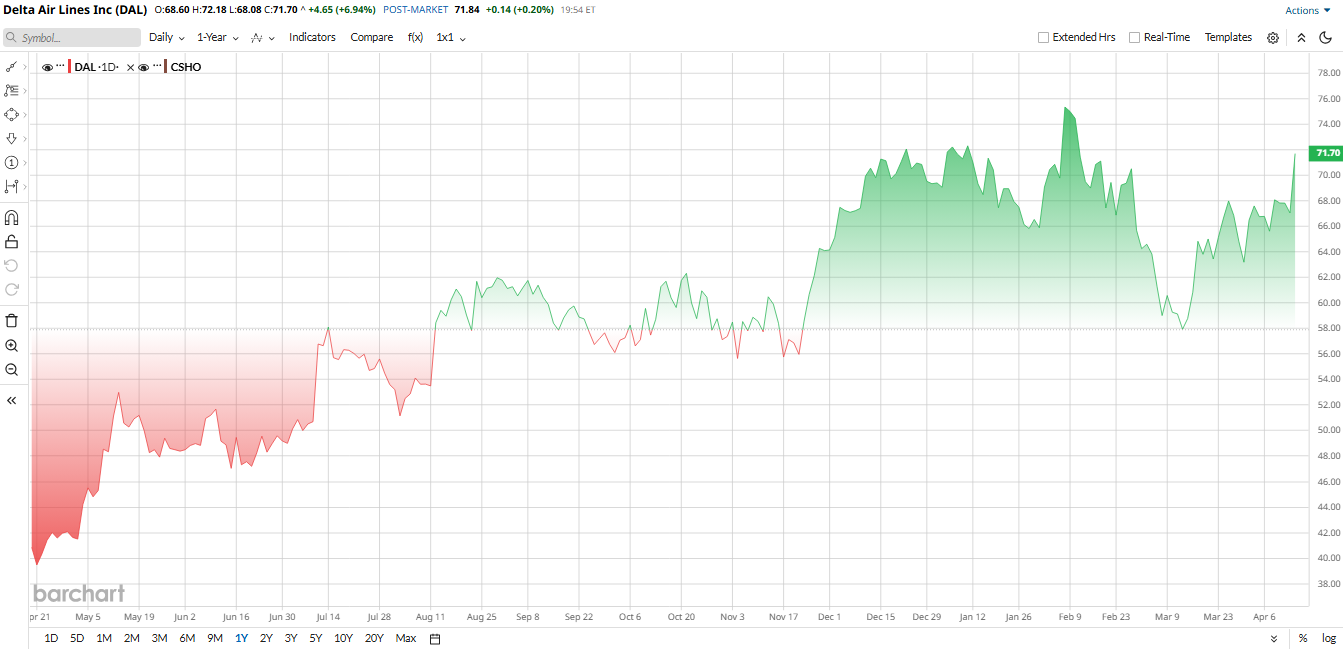

Delta ranks as a top-rated stock in the S&P 500 Industrials, and after the company’s solid first-quarter results, DAL stock has started to look more like a pullback than a breakdown. Shares have rallied 72% over the past year, yet have risen less than 1% year-to-date (YTD). Technically, DAL stock is hovering near its 50-day moving average and well above its 200-day line, which suggests the recent weakness may be more about sector-wide fuel fears than a real deterioration in the underlying business.

www.barchart.com

www.barchart.com Fuel Costs Sparked the Recent Selloff

The biggest pressure point in April has been jet fuel. A sharp rise in crude oil sent aviation fuel costs soaring, with industry estimates showing a roughly 130% YOY increase. For airlines, that is a major problem because fuel is one of the largest and most unpredictable expense lines.

Delta said the spike added about $400 million in Q1 costs, and management has already responded by adjusting fees and reducing unprofitable capacity where possible. Still, the market reacted first and asked questions later. Airline exchnage-traded funds (ETFs) fell, several carriers sold off, and Delta briefly dropped before stabilizing as oil prices eased.

CEO Ed Bastian has emphasized that Delta’s refinery gives it a unique advantage, but even that does not eliminate the pain of a sharp fuel move. The good news is that Delta’s broader revenue mix has been strong enough to absorb much of the pressure so far.

The most interesting thing is that, after the haircut, DAL stock's valuation looks appealing. Its price-to-sales (P/S) ratio is at 0.74 times and its price-to-book ratio is at 2.31 times, both significantly lower than the sector medians of 1.9 times and 3.2 times, respectively. This suggests that DAL stock is relatively undervalued compared to its peers.

That is why some investors see the recent pullback as a buying opportunity.

Q1 2026 Showed Real Operating Strength

Delta’s March-quarter results were better than the stock action might suggest. Total revenue reached a record $14.2 billion, up 9.4% from a year earlier, driven by strong premium and loyalty sales.

Premium fares grew about 14% YOY, while loyalty and related revenue rose about 13%. That mix is important because it shows Delta is not relying only on basic passenger demand. It is monetizing higher-value travelers and recurring brand loyalty, which gives the company more durability when fuel prices rise.

On a GAAP basis, the quarter included a sizable investment loss that pushed Delta to a reported net loss of $289 million, or $0.44 per share. But the adjusted picture was much stronger. Adjusted EPS came in at $0.64, up 44% YOY, while pre-tax income reached $532 million for a 3.7% margin.

Cash generation was healthy as well. Delta produced $2.4 billion in operating cash flow and $1.2 billion in free cash flow during the quarter. The firm ended March with about $5.05 billion in cash and equivalents and reduced net debt to roughly $13.5 billion, which leaves the balance sheet in better shape than it was before the pandemic.

Management’s guidance for the second quarter was cautious but constructive. Delta expects low-teens revenue growth YOY on flat capacity, with operating margins in the 6% to 8% range and EPS of $1 to $1.50, assuming fuel prices around $4.30 per gallon. That is not a blowout forecast, but it does suggest the business is still running well despite the fuel backdrop.

Why Delta Still Looks Different From the Pack

Delta has been busy making tactical moves to support the network. Recent route additions include daily service from Austin to Phoenix and Bozeman, expanded winter service from Los Angeles to Florida, and a “new nonstop service between New York-JFK and John Wayne Orange County (SNA)" starting this May.

Delta also highlighted its employee profit-sharing program, which reached about $1.3 billion for 2025 results, one of the largest payouts in the industry. That kind of spending speaks to management’s confidence in the business and helps support employee retention in a labor-intensive industry.

The market is focusing on fuel, while Delta is still delivering revenue growth, margin resilience, and balance-sheet improvement.

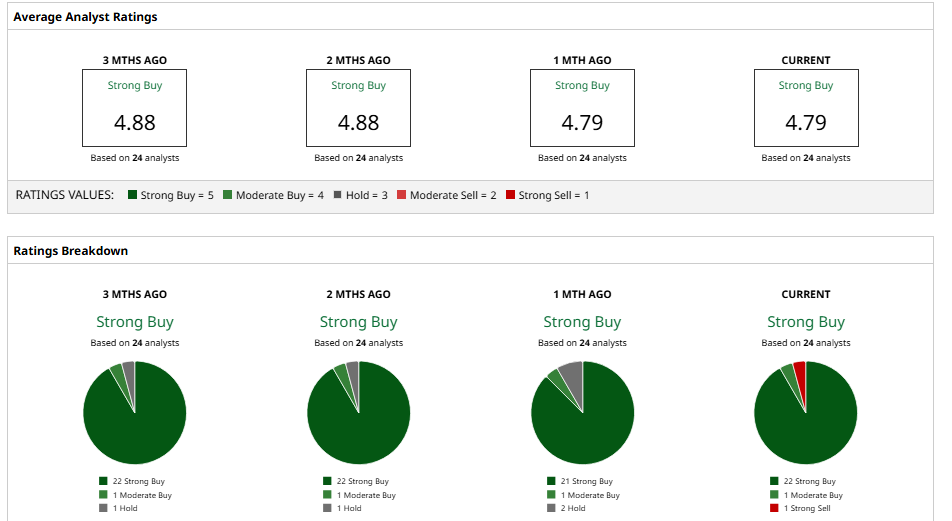

What Do Analysts Think of Delta Stock?

Morgan Stanley recently put DAL stock at the top of its airline list with a $90 price target, while Goldman Sachs raised its target to $77 and kept a “Buy” rating. Likewise, BMO Capital labeled the stock as an “Outperform” with an $80 target. In March, Wells Fargo kept an “Overweight” rating on DAL but lowered its target to $75 from $87.

Wall Street remains mostly bullish on Delta with a consensus “Strong Buy” rating. The average 12-month price target is $81.22, implying roughly 16% potential upside from current levels. With the stock trading at a modest earnings multiple and the business still performing well, many on the Street see the recent weakness as more of an entry point than a warning sign.

www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Is Bloom Energy Stock a Buy, Sell, or Hold at New All-Time Highs? Does the QQQ ETF Have a Bad Case of Premature Accumulation? Is the Software Apocalypse Real? Piper Sandler Just Slashed Its Price Target on Salesforce Stock. As Airline Stocks Sell Off on Jet Fuel Prices, Delta Is the Top-Rated Stock to Buy on the Dip