EQT Corporation EQT is set to report first-quarter 2026 results on April 21, after the closing bell.

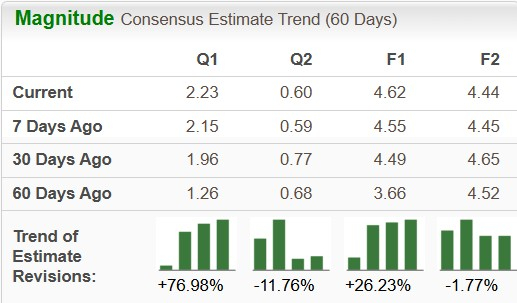

The Zacks Consensus Estimate for first-quarter earnings is pegged at $2.23 per share, implying an improvement of 89% from the year-ago reported number. It has witnessed one upward estimate revision in the past seven days. The Zacks Consensus Estimate for first-quarter revenues is currently pegged at $3.18 billion, suggesting a 47.8% improvement from the year-ago figure.

EQT beat on earnings in each of the trailing four quarters, delivering an average surprise of 12.97%. This is depicted in the graph below:

Q1 Earnings Whispers for EQT

Our proven model doesn’t predict an earnings beat for EQT this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy), or 3 (Hold) increases the chances of an earnings beat. That is just not the case here.

The leading upstream player has an Earnings ESP of 0.00% and a Zacks Rank #3. You can see the complete list of today’s Zacks #1 Rank stocks here.

You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

EQT: Factors to Note

To understand how natural gas prices behaved in the March quarter, let’s analyze commodity price data provided by the U.S. Energy Information Administration (“EIA”). The average Henry Hub Natural Gas Spot prices for January, February and March of this year were $7.72 per million Btu, $3.62 per million Btu and $3.04 per million Btu, respectively.

Commodity prices were $4.13 per million Btu, $4.19 per million Btu and $4.12 per million Btu in January, February and March of 2025, respectively, per EIA. The price of the commodity was significantly higher in January 2026, and we expect total sales volumes to have increased 4.7% year over year in the first quarter, which is likely to have aided its bottom line.

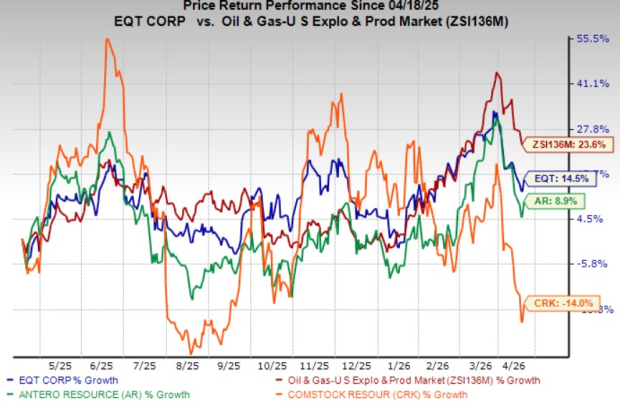

EQT’s Price Performance & Valuation

EQT stock has jumped 14.5% over the past year, underperforming the industry’s 23.6% growth. Comstock Resources, Inc. CRK, another natural gas producer, has plunged 14% over the same time frame, while Antero Resources AR has gained 8.9%.

One-Year Price Chart

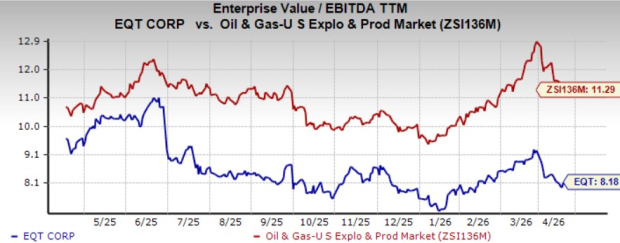

With EQT's prices underperforming the industry, the company appears relatively undervalued. The exploration and production player's current trailing 12-month enterprise value/earnings before interest, tax, depreciation and amortization (EV/EBITDA) ratio is 8.18, reflecting that it is trading at a discount compared with the industry average of 11.29. While CRK is valued lower at 7.48x, AR is valued higher at 8.84x.

Investment Thesis of EQT

EIA's short-term energy outlook projected the natural gas spot price at $3.67 per million BTU for this year, up from $3.53 last year. Mounting demand for clean energy has been driving up the price of the commodity. This trend is reflected in rising U.S. LNG exports over the years. Power-hungry data centers are also driving up natural gas prices. Being a leading explorer and producer of natural gas in the prolific Appalachian Basin, EQT is well-positioned to capitalize on robust clean energy demand. AR and CRK will also possibly gain from the commodity pricing environment.

EQT also has sufficient drilling locations to sustain its production for about three decades, reflecting a strong production outlook. However, although natural gas is a cleaner-burning fossil fuel, the world is gradually shifting toward renewable sources like wind and solar energy. This transition could reduce demand for natural gas over time, which may negatively impact EQT.

Last Word

Given the backdrop, it might not be wise for investors to bet on the stock right away despite its undervaluation. Those who have already invested may hold on to it.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Comstock Resources, Inc. (CRK): Free Stock Analysis Report

EQT Corporation (EQT): Free Stock Analysis Report

Antero Resources Corporation (AR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).