Digital payments continue to gain share globally as commerce shifts online and embedded finance expands across platforms, driving sustained transaction growth and innovation in payment infrastructure. Visa Inc. V and Block, Inc. XYZ represent two distinct approaches within this evolving landscape to capturing this opportunity, making them relevant comparables at a time when competitive dynamics and monetization models are shifting.

V operates a global card network built on scale, cross-border volumes and issuer partnerships, while Block focuses on a vertically integrated ecosystem spanning merchant services, peer-to-peer payments and financial tools. These structural differences shape their revenue models, margin profiles and exposure to end-market trends, particularly as competition intensifies across digital wallets, real-time payments and software-led financial services.

Let’s dive deep and closely compare the fundamentals of the two stocks to determine which one is a better bet now.

The Case for Visa

Visa’s investment case continues to be anchored in the scale and resilience of its global payments network. The company is delivering steady growth across payment volumes, processed transactions and cross-border flows, supported by consistent consumer spending trends. In the first quarter of fiscal 2026, payments volume rose 8% year over year, along with 12% and 9% growth in cross-border volume and processed transactions, respectively. This network effect, combined with broad acceptance and issuer relationships, underpins a highly scalable, asset-light model with strong operating leverage.

A key driver of incremental growth is Visa’s expansion beyond core transaction processing into value-added services. These offerings, including fraud prevention, data analytics, advisory and issuer solutions, are growing faster than the core business and contributing a rising share of total revenues. This shift enhances monetization per transaction while diversifying revenue streams and supporting margin durability. In the fiscal first quarter, value-added services revenues increased 28% year over year on a constant dollar basis. It beat earnings in each of the past four quarters with an average surprise of 2.1%.

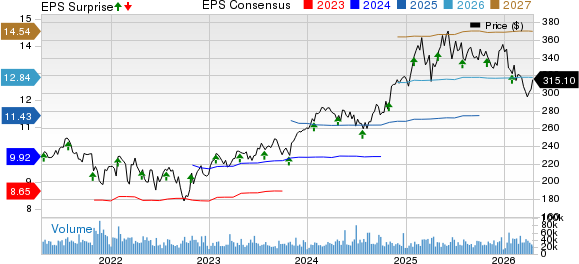

Visa Inc. Price, Consensus and EPS Surprise

Visa Inc. price-consensus-eps-surprise-chart | Visa Inc. Quote

At the same time, Visa is positioning itself as a foundational infrastructure layer for next-generation payments. Investments in tokenization, agentic commerce and stablecoin capabilities reflect a strategy centered on enabling ecosystem participants rather than owning the end customer. With billions of tokens already in circulation and increasing adoption of digital credentials, the company is reinforcing its relevance in an increasingly digital and automated payments landscape.

V’s strong cash position enables substantial share buybacks and dividend payouts and supports inorganic growth and financial stability. With $14.8 billion in cash, the company maintains a solid capital position. Its return on invested capital of 28.17X is higher than the industry’s average of 23.29X and XYZ’s 5.44X. Visa returned $3.8 billion to its shareholders through share repurchases in the fiscal first quarter.

However, escalating operating expenses and higher rebates and client incentives will likely impact its growth potential. In the first quarter of fiscal 2026, adjusted operating expenses rose 16% year over year due to higher marketing and general and administrative expenses.

The Case for Block

Block is benefiting from its vertically integrated ecosystem spanning sellers and consumers, allowing it to control both sides of the transaction. The combination of Square and Cash App enables the company to capture more value across the payment journey, with a focus on increasing engagement and monetization within its user base rather than relying solely on transaction scale. In the fourth quarter of 2025, the company’s total revenues rose 3.6% year over year.

A central pillar of this strategy is deepening customer relationships, particularly within Cash App. The company is seeing strong traction in higher-value users adopting banking-like features, lending products and card usage, which significantly increases revenue per user. This engagement-led model creates multiple monetization levers but also introduces greater exposure to consumer credit and spending behavior. In the fourth quarter of 2025, Cash App’s monthly transacting actives grew 3.5% year over year to 59 million.

Block is also undergoing a structural shift toward a more efficient operating model, leveraging AI and automation to improve productivity and accelerate product development. The updated organizational structure is aimed at enhancing efficiency and lowering expenses, supporting margin improvement as gross profit continues to scale. Cash App’s gross profit grew 33% year over year in the last reported quarter, while Square’s gross profit rose 7%. It missed earnings estimates twice in the past four quarters and beat on the other occasions.

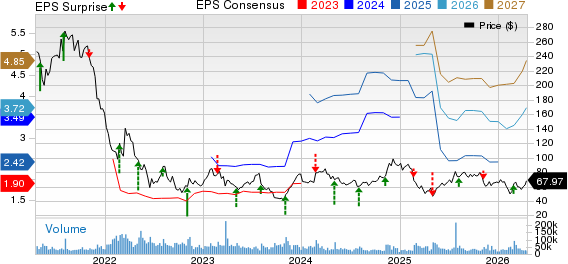

Block, Inc. Price, Consensus and EPS Surprise

Block, Inc. price-consensus-eps-surprise-chart | Block, Inc. Quote

Product development remains a core driver, with ongoing launches across lending, BNPL, payments and merchant tools. The company is prioritizing features that increase engagement, monetization and cross-sell across Cash App and Square while continuing to integrate its ecosystems to support more consistent growth in gross profit.

The company exited the fourth quarter of 2025 with cash and cash equivalents of $6.6 billion. It returned $790 million to its shareholders by repurchasing approximately 11.9 million shares of common stock in the fourth quarter. Its long-term debt-to-capital of 20.5% is lower than V’s 33.6%.

How Do Estimates Compare for V & XYZ?

The Zacks Consensus Estimate for XYZ's bottom line is comparably favorable at this stage. The consensus estimate for V’s fiscal 2026 earnings indicates an 11.9% increase from a year ago, while the same for revenues suggests 11.3% growth. On the other hand, the Zacks Consensus Estimate for XYZ's 2026 EPS indicates 57% year-over-year improvement, and the same for revenues signals an 11.1% rise.

Price Performance Comparison

Over the past year, V shares have lost 4.4%, while XYZ shares have gained 27.4%. The S&P 500 increased 37.3% during this time.

Price Performance – V, XYZ & S&P 500

Image Source: Zacks Investment Research

Valuation: V vs. XYZ

On a price-to-sales basis, Visa sits at 12.16X forward revenues, significantly above Block’s multiple of 1.48X. XYZ’s cheaper P/S multiple leaves room for significant growth as business expansion accelerates. Both companies currently carry a Value Score of D.

Image Source: Zacks Investment Research

Conclusion

Both Visa and Block offer distinct investment profiles within the payments space. Visa stands out for its scale, resilient transaction-driven model and high-margin growth supported by value-added services, while Block is more focused on ecosystem expansion, user engagement and product-led monetization.

At current levels, XYZ’s stronger earnings growth trajectory, improving cost structure and relatively lower valuation provide a more compelling setup. While execution risks remain higher, the company’s ability to scale gross profit and expand margins positions it as the more attractive pick for investors seeking growth.

While Block currently flaunts a Zacks Rank #1 (Strong Buy), Visa has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank stocks here.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Visa Inc. (V): Free Stock Analysis Report

Block, Inc. (XYZ): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).