Badger Meter, Inc. BMI reported earnings per share (EPS) of 93 cents for first-quarter 2026, which missed the Zacks Consensus Estimate by 22.5%. The bottom line compared unfavorably with the year-ago quarter’s EPS of $1.30.

Quarterly net sales were $202.3 million, down 9% from $222.2 million in the year-ago quarter due to delayed project deployments and weaker-than-expected short-cycle order activity. The Zacks Consensus Estimate was pegged at $230.1 million.

Management highlighted that the year-over-year decline in revenue and the associated operating leverage primarily stemmed from fluctuations in project timing and short-cycle customer ordering patterns, rather than any deterioration in underlying demand, competitive positioning, or long-term market drivers. The company maintains confidence in its outlook, supported by a solid pipeline of awarded projects set to commence in the second half of 2026 and a robust multi-year opportunity funnel.

Amid this near-term variability, the company remains focused on executing its long-term strategy. As part of this effort, it has announced a definitive agreement to acquire UDlive, a U.K.-based provider of hardware-enabled software solutions for sewer line monitoring. The addition of UDlive enhances the SmartCover platform by broadening sewer line monitoring capabilities across diverse use cases, network conditions and geographies. These solutions strengthen the company’s leadership in a growing global market driven by aging infrastructure, evolving regulatory requirements and climate-related challenges.

Furthermore, UDlive bolsters the BlueEdge suite, enabling utilities to gain deeper, actionable insights across the water cycle, while expanding the company’s presence and supporting the growth of higher-margin, recurring software revenue over time.

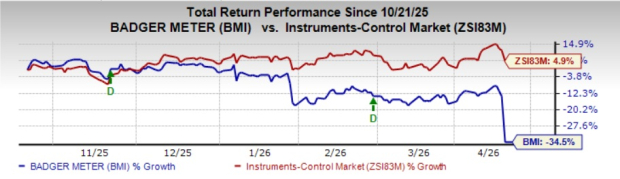

Image Source: Zacks Investment Research

BMI’s shares fell 24% on Friday, closing at $115.54 in response to the weaker-than-expected results. In the past six months, shares have lost 34.5% against the Zacks Instruments-Control industry’s growth of 4.9%.

Segmental Performance

In the quarter under review, utility water sales decreased 10% year over year. The decline was due to project timing variability and softer short-cycle municipal customer orders, partially offset by strength in SaaS, SmartCover, water quality and network monitoring solutions.

Flow instrumentation sales decreased 4% year over year, as modest growth in water-focused end markets was offset by declines in de-emphasized applications.

Other Details

In the first quarter, gross profit was $84.3 million, down from $95.4 million in the prior-year quarter. Gross margin was 41.7%, down 120 basis points (bps) year over year. Gross margin decreased due to product and project mix. Despite the year-over-year decline, margins remained strong and near the upper end of the normalized range, underscoring the resilience of pricing discipline and the benefits of a favorable structural mix.

Operating earnings decreased around 29% year over year to $35.2 million, while operating margin contracted 480 bps to 17.4% from 22.2%.

Selling, engineering and administration (SEA) expenses decreased sequentially but rose year over year by $3.1 million to $49.2 million, reflecting acquisition-related costs and an additional month of SmartCover SEA expenses. Overall, SEA as a percentage of sales rose to 24.3% from 20.7%.

Cash Flow & Liquidity

In the first quarter of 2026, Badger Meter generated $33.9 million of net cash from operating activities compared with $33 million a year ago.

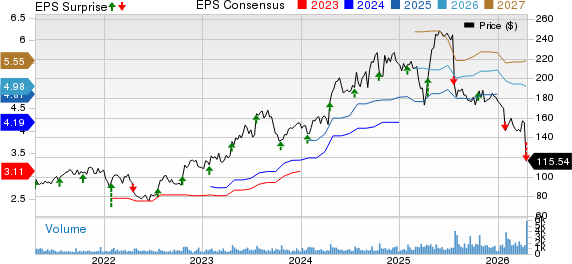

Badger Meter, Inc. Price, Consensus and EPS Surprise

Badger Meter, Inc. price-consensus-eps-surprise-chart | Badger Meter, Inc. Quote

As of March 31, 2026, the company had $205.5 million of cash and cash equivalents and $169.4 million of total current liabilities compared with the respective figures of $226 million and $150.7 million as of Dec. 31, 2025.

Outlook

Badger Meter remains focused on disciplined execution while advancing its long-term strategic priorities. Backed by a strong balance sheet, it is well-positioned to continue investing in the business, return cash to shareholders and pursue opportunities within its attractive M&A pipeline. This balanced approach is expected to help navigate near-term variability while building momentum over the course of the year and delivering sustained value to stakeholders.

Management highlighted that as awarded projects move into the deployment phase, revenue is expected to improve sequentially. Higher project activity and a more normalized mix should drive a stronger revenue run-rate toward the end of 2026, with full-year revenue, excluding acquisitions, projected to remain relatively flat compared with 2025. Despite variability in project timing and order patterns, the company maintains a positive long-term outlook, supported by solid demand and its competitive strengths in the North American smart water market.

BMI’s Zacks Rank

Badger Meter currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Recent Performance of Other Companies

Simulations Plus, Inc. SLP reported second-quarter fiscal 2026 adjusted earnings of 35 cents per share, surpassing the Zacks Consensus Estimate by 29%. The bottom line also compared favorably with the prior-year quarter’s 31 cents. Simulations Plus reported quarterly revenue of $24.3 million, marking an 8% year-over-year increase. This growth reflects continued demand for its core offerings, especially in drug discovery and development.

BlackBerry Limited BB reported fourth-quarter fiscal 2026 non-GAAP earnings per share (EPS) of 6 cents. The figure beat the company’s estimate of 3-5 cents. In the year-ago quarter, it reported a non-GAAP EPS of 3 cents. The Zacks Consensus Estimate was pegged at 5 cents per share.

BlackBerry reported quarterly revenue of $156 million, surpassing the top end of its guidance ($138-$148 million), driven by stronger-than-expected sales across both its QNX and Secure Communications divisions. Revenue also increased 10% year over year.

Guidewire Software, Inc. GWRE reported non-GAAP earnings per share of $1.17 for the second-quarter fiscal 2026 (ended Jan. 31, 2026) compared with 51 cents in the same period last year. Earnings surpassed the Zacks Consensus Estimate of 77 cents. The company reported revenues of $359.1 million, up 24% year over year. Revenues beat the Zacks Consensus Estimate by 4.8%. The figure also surpassed the company’s guided range of $339-$345 million. This uptick was driven by solid momentum across all business segments.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Badger Meter, Inc. (BMI): Free Stock Analysis Report

Simulations Plus, Inc. (SLP): Free Stock Analysis Report

Guidewire Software, Inc. (GWRE): Free Stock Analysis Report

BlackBerry Limited (BB): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).