PulteGroup PHM reported first-quarter 2026 results, with adjusted earnings missing the Zacks Consensus Estimate and revenues surpassing the same. Both metrics declined year over year amid continued affordability pressures and margin compression. Lower consumer confidence and higher incentive activity weighed on profitability, partially offset by stable order trends, higher community counts and disciplined capital deployment.

Following the earnings announcement, investor reaction was negative. Shares of the Atlanta-based homebuilder slipped 2% in today’s pre-market trading session, reflecting concerns around declining profitability and margin pressure.

Revenues & Earnings Performance

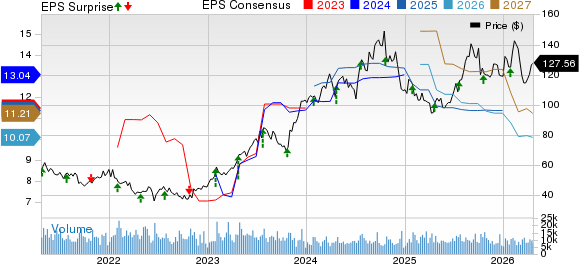

PulteGroup reported first-quarter 2026 earnings of $1.79 per share, missing the Zacks Consensus Estimate of $1.80 by 0.6%. The figure declined 30.4% from $2.57 per share in the year-ago quarter.

PulteGroup, Inc. Price, Consensus and EPS Surprise

PulteGroup, Inc. price-consensus-eps-surprise-chart | PulteGroup, Inc. Quote

Total revenues of $3.41 billion beat the Zacks Consensus Estimate of $3.38 billion by 0.9% and decreased 12.4% year over year. The top-line beat was supported by steady order growth despite lower closing volumes and pricing pressure.

PHM Revenues Reflect Lower Volumes and Pricing

PulteGroup’s home sale revenues totaled $3.3 billion in the first quarter of 2026, marking a 12% year-over-year decline. The decrease was caused by a 7% drop in closing volumes to 6,102 homes and a 5% reduction in average selling price to $542,000.

Land sales and other revenues also declined, contributing to overall top-line pressure. The company noted that affordability concerns and broader economic uncertainty continued to weigh on buyer behavior, impacting both pricing and conversion rates.

Despite these headwinds, management highlighted steady demand trends, supported by a growing community count and disciplined operational execution.

PHM Financial Services

PulteGroup’s financial services segment generated pre-tax income of $13 million, down from $36 million in the prior-year period. The decline reflects lower closing volumes and a slight decrease in the mortgage capture rate to 85%.

PulteGroup Margins Pressured by Incentives

Profitability weakened during the quarter as home sale gross margin declined to 24.4% from 27.5% in the prior-year period. The contraction reflects higher incentive activity used to stimulate demand and reduce excess inventory.

Selling, general and administrative expenses totaled $380 million, representing 11.5% of home sale revenues, up from 10.5% a year ago. This increase indicates rising cost pressures relative to declining revenues.

The combined effect of lower pricing, higher incentives and increased cost ratios contributed to the sharp decline in earnings compared with the prior year.

PHM Orders Growth Signals Demand Stability

A key positive in the quarter was the increase in net new orders. Orders rose 3% year over year to 8,034 homes, with total value reaching $4.6 billion.

The company operated from an average of 1,043 communities during the quarter, up 9% from the prior year. This expansion supported order growth despite ongoing affordability challenges.

Backlog stood at 10,427 homes valued at $6.5 billion at the quarter's end, providing visibility into future revenue streams. However, backlog levels declined compared with the prior year, reflecting slower conversion and market caution.

Management emphasized that while buyers remain sensitive to economic conditions, demand for homeownership persists, helping sustain order activity.

PulteGroup Balance Sheet and Capital Moves

PulteGroup maintained a strong balance sheet position with $1.8 billion in cash at the end of the quarter. The company’s debt-to-capital ratio was 12.3, indicating a relatively conservative leverage profile.

During the quarter, the company repurchased $308 million of its common shares, underscoring the commitment to returning capital to shareholders. Additionally, the board approved a $1.5 billion increase in share repurchase authorization.

Cash flow from operations totaled $159.8 million, reflecting disciplined capital management despite lower earnings. The company also invested significantly in land acquisition and development to support growth.

PHM’s Zacks Rank & Recent Construction Releases

PulteGroup currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

D.R. Horton DHI delivered second-quarter fiscal 2026 results with earnings beating the Zacks Consensus Estimate but revenues missing the same. The quarter was marked by an 11% jump in net sales orders and progress in tightening finished inventory, even as affordability constraints kept incentives elevated.

D.R. Horton updated fiscal 2026 consolidated revenue guidance to $33.5-$34.5 billion compared with the prior expectation of $33.5-$35 billion. This compares with $34.25 billion in fiscal 2025. D.R. Horton now expects homebuilding closings of 86,000-87,500 homes compared with the earlier guidance of 86,000-88,000. This compares with 84,863 in fiscal 2025.

KB Home KBH reported first-quarter fiscal 2026 results. The company’s quarterly earnings came in line with the Zacks Consensus Estimate, while total revenues missed the same. Both metrics decreased on a year-over-year basis.

For the second quarter of fiscal 2026, KB Home is expecting housing revenues to be in the $1.05-$1.15 billion band, down from $1.52 billion reported in the year-ago period. KB Home expects deliveries to be in the range of 2,250-2,450 homes compared with 3,120 homes delivered in the year-ago period.

Lennar Corporation LEN reported tepid results for the first quarter of fiscal 2026, wherein its adjusted earnings and total revenues missed the Zacks Consensus Estimate and declined year over year.

For the fiscal second quarter, Lennar expects deliveries to be in the range of 20,000-21,000 homes compared with 20,131 homes delivered in the year-ago period. Lennar expects the ASP of the delivered homes to be in the range of $370,000-$375,000, down from $389,000 reported a year ago.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

PulteGroup, Inc. (PHM): Free Stock Analysis Report

KB Home (KBH): Free Stock Analysis Report

Lennar Corporation (LEN): Free Stock Analysis Report

D.R. Horton, Inc. (DHI): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).