Tempus AI, Inc. TEM is expected to report first-quarter 2026 results on May 5, after market close.

In the last reported quarter, the company’s adjusted loss of 4 cents per share was broader than the Zacks Consensus Estimate of a loss of 2 cents. Tempus went public in June 2024. Its earnings beat on estimates in three of the trailing four quarters and missed in one, the average negative surprise being 13.32%.

The Zacks Consensus Estimate for revenues is currently pegged at $345.5 million for the first quarter, implying a 35.1% improvement over the year-ago period.

The consensus estimate for loss per share has remained unchanged at 21 cents over the past 30 days.

TEM's Earnings Estimate Revision Trend

Image Source: Zacks Investment Research

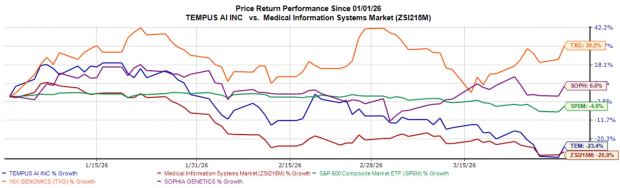

During the first quarter, Tempus’ share price experienced a 23.4% decline, mainly due to macroeconomic challenges, including escalating trade tensions that broadly impacted the healthcare technology sector. The company witnessed strong momentum, primarily driven by a series of strategic acquisitions and partnerships in the field of AI-driven precision medicine, as well as a slew of product launches.

The Zacks Medical Info Systems industry and the S&P 500 benchmark index lost 25.9% and 4.9%, respectively, over the same time period. Other industry players, such as 10x Genomics TXG and SOPHiA GENETICS SOPH, gained 30.2% and 6.0%, respectively.

TEM's Q1 Price Performance Comparison

Image Source: Zacks Investment Research

Let’s see how things might have shaped up for TEM prior to the announcement:

Key Factors to Note Prior to Tempus' Q1 Earnings

In January, Tempus entered a multi-year partnership with NYU Langone Health to advance cancer care using molecular profiling and data-driven insights. This was followed by an expanded collaboration with Merck (MSD outside the United States and Canada) in March to accelerate biomarker discovery and support oncology and broader therapeutic development. Tempus also partnered with Daiichi Sankyo to advance and differentiate an antibody drug conjugate program in oncology. These developments might have helped Tempus establish a strong footprint in oncology with an industry-leading technology portfolio.

In the first quarter, we expect Tempus’ Diagnostics segment’s sales to have experienced an improvement from accelerating volume growth in oncology testing and sustained strength in hereditary sequencing. The Data and Applications business is likely to have experienced strong demand for Tempus’ proprietary data licensing and AI solutions.

As of Dec. 31, 2025, Tempus reported Total Contract Value exceeding $1.1 billion, the highest in its history, supported by data agreements with more than 70 large and mid-sized pharma customers. The company also achieved strong momentum with net revenue retention of approximately 126% in 2025. We expect this trend to have persisted in the to-be-reported quarter.

From an R&D perspective, in the first quarter of 2026, Tempus introduced Paige Predict, a suite of advanced digital pathology applications that analyze hematoxylin and eosin whole-slide images to guide testing decisions. The company also launched its HRD-RNA algorithm, an AI-driven 1,660-gene logistic regression model designed to identify patients most likely to benefit from platinum-based chemotherapy or PARP inhibitors. We expect that these developments are likely to have boosted the company’s top-line growth.

Tempus’ fourth-quarter gross profit saw 94.7% year-over-year improvement, while adjusted EBITDA was positive, bringing it within the reach of profitability. It expects positive adjusted EBITDA of $65 million in 2026. We expect the company to have progressed meaningfully in the to-be-reported quarter.

Investments tied to these updates, including product development, regulatory efforts and marketing, are likely to have pushed operating expenses higher in the first quarter, putting some pressure on short-term profitability. Broader macroeconomic factors, like tariffs, hospital budget constraints and biotech funding trends, might have also affected adoption rates.

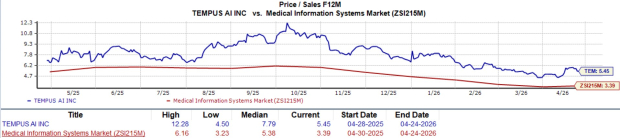

Expensive Valuation

Tempus stock is currently overvalued compared with its industry, as shown in the chart below.

TEM is currently trading at a forward 12-month price-to-sales (P/S) ratio of 5.45X, a premium to the broader industry's median of 5.38X.

Image Source: Zacks Investment Research

Our Take

Despite Tempus’ strong strategic momentum, expanding collaborations and continued innovation in AI-driven precision medicine, the near-term risk-reward profile appears less favorable for investors. While robust contract value, high customer retention and progress toward profitability support its growth outlook, potential industry-wide pressures may temper upside in the near term.

The negative earnings estimate trend reinforces the outlook of continued near-term challenges. With limited visibility into sustained earnings improvement, the current valuation leaves little room for execution missteps. As a result, investors may consider booking profits and reallocating capital to better-positioned opportunities for this Zacks Rank #4 (Sell) stock now.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

10x Genomics (TXG): Free Stock Analysis Report

SOPHiA GENETICS SA (SOPH): Free Stock Analysis Report

Tempus AI, Inc. (TEM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).