For all the attention on electric vehicles (EVs), Tesla (TSLA) has always been chasing the bigger goal of autonomy. Under Elon Musk, that vision now stretches beyond cars, with AI, robotaxis, and humanoid robots like Optimus coming together as part of a much larger play. Speaking on Tesla’s Q1 earnings call, Musk said the company is substantially increasing investments for the future, with a notable rise in capital expenditures to support expanded manufacturing and production. He added that Tesla will continue spending heavily on autonomy, Optimus, and new vehicle ramps.

Robotics is quickly becoming part of everyday tech, and Tesla wants a front-row seat. Its Optimus V3 humanoid robot is designed to handle repetitive, real-world tasks, like factory work, logistics and even basic household support. Musk also laid out the clearest timeline yet, saying the company is pushing toward actually releasing Optimus, with the goal of making it useful outside the company as early as next year.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Behind the scenes, production is already ramping. Tesla plans to start building units in Fremont around July or August after rapidly reworking existing Model S and Model X lines – something Musk says happened at an unusually fast pace. Still, he is keeping expectations in check.

Early output will be limited, and scaling a brand-new product with thousands of parts is unpredictable. At the same time, competitors like Boston Dynamics , Figure AI, and Agility Robotics are already testing their own humanoid robots in real-world settings, adding pressure.

If Tesla gets this right, Optimus could be the moment its autonomy story truly comes to life, while offering a timely tailwind to lift sentiment around TSLA stock after its recent weakness.

About Tesla Stock

Tesla has grown into one of the most talked-about companies, now sitting comfortably above a $1.4 trillion market cap. Headquartered in Austin, Texas, and founded in 2003, the company has steadily outgrown its identity as just an EV maker.

While its vehicles still bring in the bulk of revenue, the real story is shifting. Tesla is leaning deeper into autonomy, robotics, and AI infrastructure, building what looks more like a full-scale tech ecosystem. With Gigafactories ramping production and projects like robotaxis and Optimus taking shape, the company is positioning itself as a platform for the future. Under Elon Musk, Tesla continues to influence how the world thinks about mobility, energy, and intelligent machines.

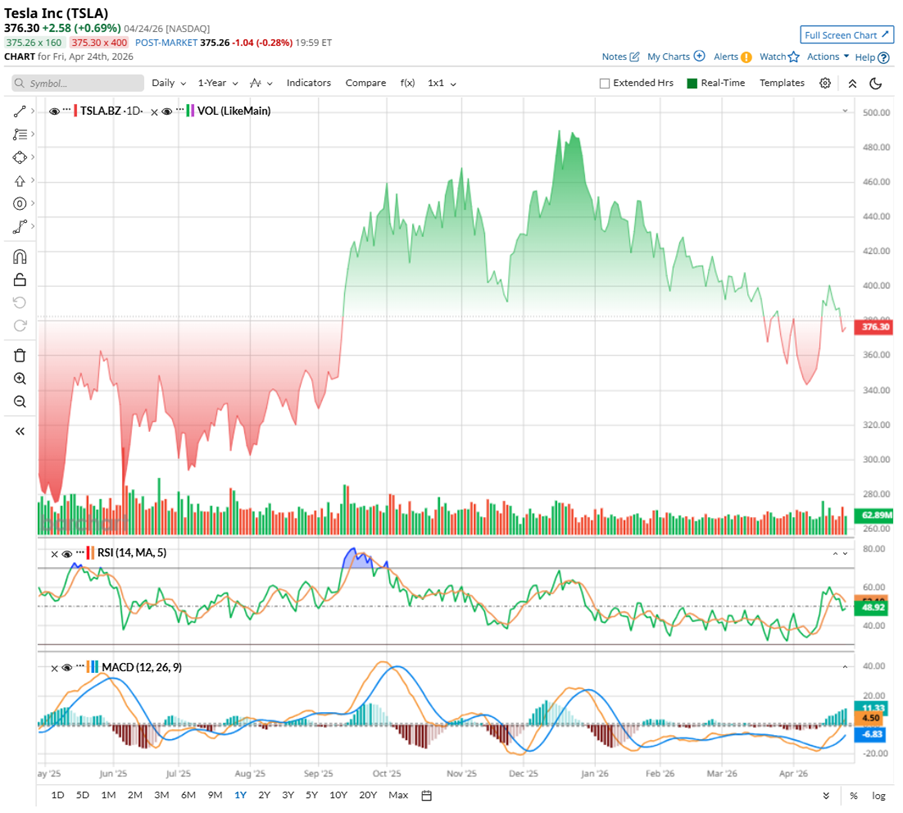

TSLA has not had an easy stretch from 2025 into 2026. It came into last year strong, even touching a high of $498.83 in December. But since then, the stock has cooled off, slipping to around $376 by late April, down 25.5% from the peak and 18.12% year-to-date (YTD).

A few situations have been dragging it down. EV demand is not as strong as before, costs are rising, and the company’s big spending plans have made investors a bit cautious. For months, the stock traded mostly sideways, without a clear trend. It’s also worth noting that TSLA stock is currently the weakest performer among the “Magnificent Seven” this year, which shows how quickly sentiment has shifted.

Still, it’s not all bad. Over the past year, the stock is up 29%, so the longer-term trend still holds.

From a technical standpoint, things look fairly balanced for TSLA right now. Trading volumes have been a bit light, though recent sessions are showing some buying interest with a few green bars. The 14-day RSI sits at 45.43, which suggests the stock is neither overbought or oversold, but in neutral territory. Meanwhile, the MACD oscillator signals improving sentiments, with the MACD line crossing above the signal line and the histogram printing green bars, hinting that momentum could slowly be shifting upward.

www.barchart.com

www.barchart.com Valuation-wise, TSLA trades at a premium even after the pullback. It is priced at 179.3 times forward adjusted earnings and 13.85 times sales – above the sector averages and historical medians. That kind of premium already bakes in big wins ahead, meaning expectations are sky-high, and even small stumbles could quickly test investor patience.

A Snapshot of Tesla’s Q1 Earnings Report

Tesla dropped its fiscal Q1 2026 results on April 22, and both its top and bottom lines beat projections. Revenue climbed 16% year-over-year (YOY) to $22.4 billion, while adjusted EPS landed at $0.41, jumping 52% annually.

Tesla’s core EV engine is still doing the heavy lifting. Automotive revenue rose roughly 16% YOY to $16.2 billion, continuing to anchor the business. Margins, too, showed real muscle, with total GAAP gross margin expanding to 21.1% from 16.3% a year ago. Excluding regulatory credits, automotive gross margin still improved to 19.2%. Even adjusted EBITDA margin ticked up to 16.4%. That is the operational discipline showing up clearly.

On the balance sheet side, Tesla still looks like a fortress. It ended the quarter with $44.7 billion in cash, equivalents, and short-term investments. That pile was supported by $1.4 billion in free cash flow and another $1.2 billion from financing activities, although a $2 billion investment in SpaceX took a bite out of the total.

On paper, that’s the kind of growth story investors usually applaud. But the market was not in the mood to clap. The stock slipped about 3.6% in the next trading session, almost as if investors were reading between the lines rather than just the numbers.

Beneath all of that strength, Tesla’s management itself is signaling a shift, and maybe a bit of discomfort. They openly acknowledged rising competitive pressure and an aging vehicle lineup. That’s not trivial when players like BYD Company (BYDDY) and Xiaomi (XIACY) are flooding the market with newer, cheaper, and increasingly feature-packed EVs.

But here’s where the story takes a sharp turn.

Tesla is no longer just an EV company trying to optimize margins – it is trying to reinvent itself. Management has dialed up its 2026 capital expenditure guidance to over $25 billion, a massive leap from $8.6 billion in 2025. That spending is aimed at AI infrastructure, new product pipelines, and scaling manufacturing capacity. The company’s “Physical AI” vision, like autonomous systems, robotics, and beyond, is now front and center.

And that ambition comes at a cost. Tesla warned that this surge in spending, especially around AI training clusters and the Cybercab supply chain, could push free cash flow into negative territory for the rest of the year.

Interestingly, Tesla is not chasing reckless expansion. Instead, it is squeezing more out of what it already has, prioritizing efficiency at existing factories before committing to new ones. Meanwhile, its next-gen lineup of Cybercab, Semi, and Megapack 3 remains on track for volume production in 2026.

Early Optimus assembly lines are quietly coming together, signaling that Tesla is thinking far beyond cars. The first-generation setup, built to handle up to 1 million robots annually, is set to take over the Model S and Model X lines in Fremont. And that’s just phase one. Over in Texas, Gigafactory Texas is being prepped for a second-generation line designed with a far more ambitious goal, scaling toward 10 million robots a year over the long run.

Analysts tracking Tesla predict the EV company’s EPS for fiscal 2026 growing 23.9% YOY to $1.35, and then rise by another 37.8% annually, pushing EPS to around $1.86 in fiscal 2027.

What Do Analysts Expect for Tesla Stock?

Wall Street didn’t exactly panic after Tesla’s Q1 earnings call, but nobody was popping champagne either. A lot of analysts came away thinking this quarter was not about what Tesla just delivered, but was about what it is about to spend. And that’s where things start to feel a bit heavier.

Goldman Sachs analyst Mark Delaney kept a “Neutral” rating and a $375 price target, and gave Tesla credit where it’s due. He acknowledged improving margins, and rising FSD subscriptions. But when it comes to robotaxis, he does not expect a sudden breakout. In his view, the rollout is going to be slow and steady, and fully unsupervised FSD for consumers might not even show up until late 2026. On top of that, he sees all this heavy investment dragging FCF into the red through 2026 and 2027, with a potential turnaround only by 2028.

Meanwhile, Barclays' Dan Levy reiterated an “Equal Weight” rating and $360 target. He believes that Tesla is entering what he called its “most consequential period of investment ever.” He pointed out that both robotaxis and Optimus still need to show real-world traction, and even flagged that older hardware could slow down how quickly people adopt FSD.

Andrew Percoco of Morgan Stanley is cautious as well. He maintained an “Equal Weight” rating and $415 target, noting that robotaxi miles have more than doubled since December, which sounds impressive, but added that near-term upside still looks limited. That’s because the big “physical AI” bets are moving slower than investors were hoping, all while spending and cash burn keep climbing.

Jefferies’ Philippe Houchois was a bit more upbeat than the rest. He highlighted that demand actually looks solid, with Tesla’s order backlog at its highest level in two years. But even he zeroed in on Optimus as the real wildcard. With production expected to kick off in a couple of months, that timeline is now something everyone’s watching closely.

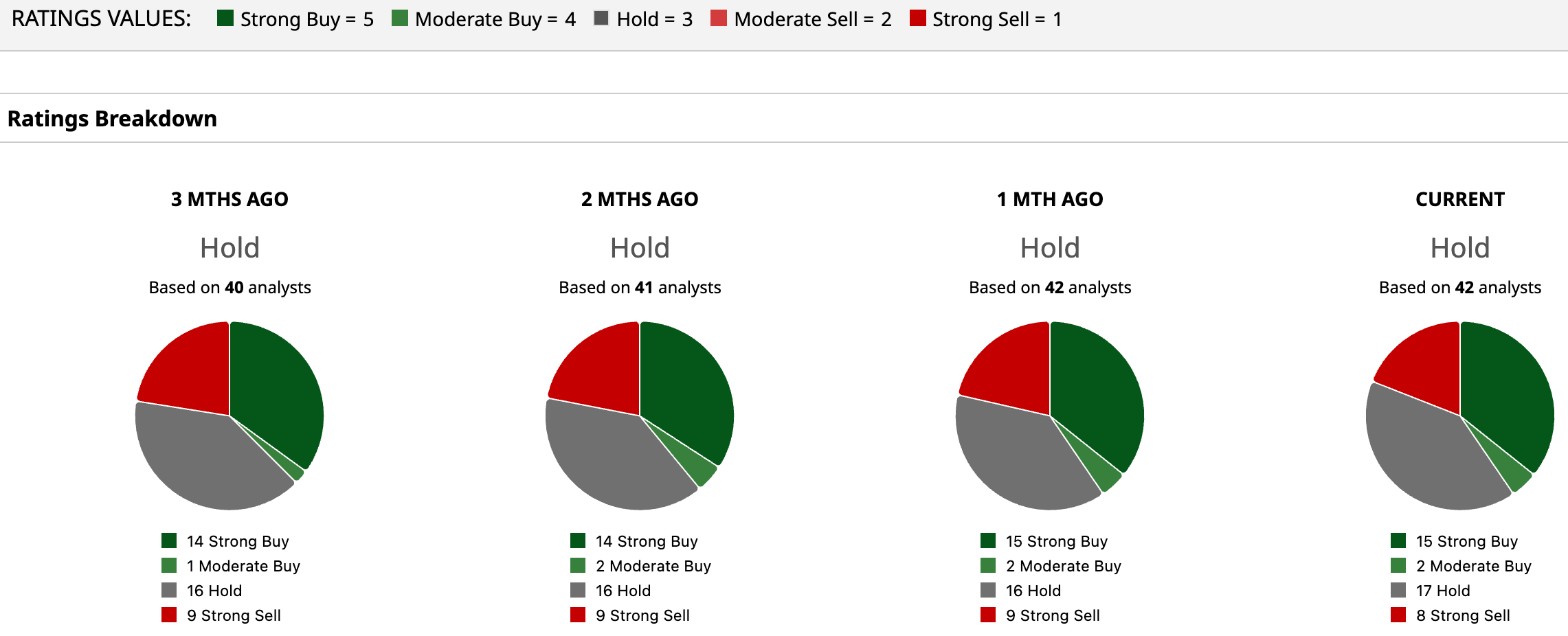

Analysts remain sharply divided on Tesla. The stock has a “Hold” rating overall. Of the 42 analysts covering the stock, 15 recommend a “Strong Buy,” two have a “Moderate Buy,” 17 suggest a “Hold,” and the remaining eight have a “Strong Sell” rating.

The mean price target of $405.08 suggest the EV stock has potential upside of 8.65% from the current levels. Wedbush’s Street-high of $600 implies TSLA could rise as much as 60.9% from here.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Here's Why Wall Street Thinks Micron Stock Can Touch $852 The $100 Million Man: What the ‘Richest Ever’ Fed Chair Nominee Kevin Warsh, With Investments in Elon Musk’s SpaceX, Means for Your Portfolio The Biggest Catalyst for Tesla Stock in History Could Trigger in Just 3 Months The 3 Dividend Aristocrats Wall Street Calls a ‘Strong Buy’ With Up to 46% Upside