Petróleo Brasileiro S.A. - Petrobras PBR has emerged as a standout energy play, rallying sharply as rising crude prices and global supply disruptions reshape the oil market. With prices hovering near $100 per barrel — well above its conservative planning assumptions — the company is poised to generate significantly higher free cash flow and boost shareholder returns. Petrobras benefits from limited exposure to Middle Eastern instability, allowing it to capitalize on favorable pricing without major operational risks. This unique combination of strong production growth, free cash flow generation and disciplined shareholder return positions the company as a compelling investment opportunity. For investors seeking energy exposure in 2026, this Brazilian giant is increasingly difficult to ignore.

Steady Pre-Salt-Driven Production Growth Through 2030

Petrobras’ production growth outlook reflects a combination of near-term acceleration and long-term resilience driven by its high-quality pre-salt portfolio and ongoing project ramp-ups. The company exited 2025 with total oil and gas production, including NGL, at around 2.99 million barrels of oil equivalent per day (BOE/d) and targets a steady increase toward 3.4 million BOE/d by 2028, before stabilizing near that level through 2030. This growth trajectory is underpinned by new FPSO deployments, improved operational efficiency and reservoir optimization initiatives, particularly in the Santos Basin. Natural gas production is also expected to rise steadily, adding diversification to the production mix. Overall, Petrobras’ production growth is characterized by disciplined capital allocation, low-cost assets and a focus on maximizing recovery, positioning it to deliver consistent volume expansion while maintaining industry-leading margins.

This gives Petrobras an edge over U.S. peers like Chevron Corporation CVX and Exxon Mobil Corporation XOM, which expect a fall in their first-quarter production. Chevron recently announced that it expects its first-quarter production to fall to 3.8-3.9 million boed from just more than 4 million boed in the previous quarter. The decline is mainly tied to downtime at the Tengizchevroil project in Kazakhstan and lower output from assets in Israel and the Saudi-Kuwaiti Partitioned Zone. ExxonMobil announced that disruptions to its operations in Qatar and the United Arab Emirates are expected to cut its global oil-equivalent output by 6% in the first quarter versus the prior quarter.

PBR’s Robust Free Cash Flow Backed by Low-Cost Asset Base

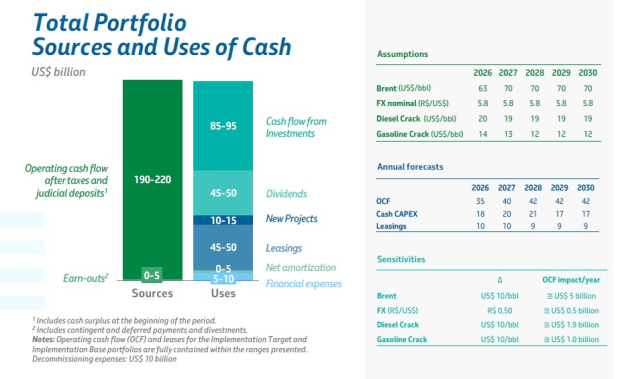

Petrobras generates robust free cash flow (FCF), supported by its low-cost upstream operations and disciplined capital spending framework. In 2025, the company reported free cash flow of $16.5 billion despite a weaker Brent price environment. This demonstrates the resilience of its asset base, particularly the pre-salt fields. Looking ahead, the 2026-2030 business plan projects annual operating cash flow (OCF) in the range of $35-$42 billion, with capital expenditures maintained at controlled levels of roughly $17-$21 billion per year, enabling sustained FCF generation. The company’s breakeven is estimated at around $59/bbl Brent, highlighting its ability to remain cash flow positive even in lower price scenarios. The sensitivity of cash flow to oil prices remains significant (e.g., a $10/bbl change in Brent impacts OCF by $5 billion). The latest bullish wave about Petrobras was triggered by Brent wobbling around $100 per barrel, well above its long-term planning assumption. That price environment would materially expand its FCF capacity.

Image Source: Petroleo Brasileiro S.A. - Petrobras

Disciplined Dividend Policy Anchored to Free Cash Flow

Petrobras’ dividend policy is closely tied to its free cash flow, positioning it among the most shareholder-focused oil majors. The company distributes around 45% of FCF to investors, provided debt stays within targeted levels and financial stability is maintained. In 2025, this resulted in about $7.5 billion in total shareholder payouts. Dividends are issued quarterly, ensuring consistency, with room for additional extraordinary payouts when cash flows exceed expectations. The framework also allows distributions in certain low-income periods, subject to financial and legal limits. Backed by disciplined spending and a flexible capital structure, Petrobras maintains dividend capacity even in volatile markets, offering a high-yield, performance-linked return profile.

PBR’s Strong Price Performance, Estimate Revisions & Valuations

Petrobrashas posted an impressive performance over the past year, with its shares surging 81.3%, outperforming the sub-industry’s 43.8% growth. Peer comparison further highlights the strength, as Petrobras conveniently outperformed its peers, Chevron and ExxonMobil, which gained 32.2% and 37%, respectively, during the same time period.

Image Source: Zacks Investment Research

Over the past 30 days, the Zacks Consensus Estimate for PBR’s earnings per share has moved higher for 2026 and 2027. The estimates have also been revised upward for CVX and XOM over the same period.

Image Source: Zacks Investment Research

From a valuation perspective — in terms of Enterprise Value to Earnings Before Interest, Taxes, Depreciation and Amortization (EV/EBITDA) ratio — Petrobras is trading at a discount compared with Chevron and ExxonMobil, making it attractive for investors.

Valuation Comparison

Image Source: Zacks Investment Research

Final Verdict on PBR Stock

Petrobras stands out as a high-conviction energy investment with a favorable balance of growth, income and valuation upside. Strong pre-salt production growth, a low-cost asset base and significant free cash flow leverage to higher oil prices underpin its fundamentals. The company’s disciplined, FCF-linked dividend policy enhances its appeal for income-focused investors, while discounted valuation versus global peers adds upside potential. However, policy risks tied to government influence remain key considerations. Overall, Petrobras, currently sporting a Zacks Rank #1 (Strong Buy), stands out as an attractive buy for investors seeking high yield and leverage to favorable crude dynamics, provided they can tolerate geopolitical and commodity-driven risks.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Chevron Corporation (CVX): Free Stock Analysis Report

Exxon Mobil Corporation (XOM): Free Stock Analysis Report

Petroleo Brasileiro S.A.- Petrobras (PBR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).