Valued at $412.3 billion by market cap, Intel Corporation (INTC) is one of the world’s most influential semiconductor companies, historically synonymous with the rise of personal computing. Founded in 1968 and headquartered in Santa Clara, California, Intel designs and manufactures microprocessors, chipsets, and a broad range of computing and connectivity solutions.

INTC has soared 323.9% over this time frame, well ahead of the broader S&P 500 Index ($SPX), which has rallied 29.8%. In 2026, INTC’s stock popped 130.3% compared to the SPX’s 4.8% rise on a YTD basis.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Intel’s strength is also notable against industry peers. The SPDR S&P Semiconductor ETF (XSD) has gained 138.6% over the past year and 44.5% on a YTD, trailing INTC’s impressive gains over the same time frames.

www.barchart.com

www.barchart.com Intel’s sharp outperformance in 2026 is being driven by a combination of earnings momentum, AI exposure, and improving execution, which has triggered a meaningful re-rating in the stock. A key catalyst is Intel’s increasing participation in AI-driven demand cycles. AI-related businesses now account for a significant portion of revenue and are growing rapidly, with strength concentrated in the Data Center and AI segment. Rising demand for CPUs, custom silicon (ASICs), and AI infrastructure signals that Intel is finally capturing share in the same secular trends that have powered peers.

On Apr. 23, Intel delivered a strong first quarter for 2026, signaling a clear improvement in operating momentum. Revenue came in at $13.6 billion, up 7% year over year, driven by healthier demand conditions, improved supply, and a more favorable product mix. The company also benefited from better pricing, which, alongside cost discipline, supported a recovery in profitability. Its non-GAAP EPS rose 123% year over year to $0.29.

The standout driver was Intel’s Data Center and AI segment, which posted robust growth on the back of rising demand for AI infrastructure. Strength in server CPUs and custom silicon reflects increasing enterprise and cloud investment as AI workloads evolve. At the same time, the Client Computing segment remained resilient, with demand for AI-enabled PCs gaining traction despite broader industry headwinds. The results were well received by the market, with the stock rising 23.6% in the following session after the earnings release.

For the current fiscal year, ending in December, analysts expect INTC’s profit per share to rise 241.7% to $0.17 on a diluted basis. The company’s earnings surprise history is mixed. It beat the consensus estimates in three of the last four quarters while missing the forecast on one occasion.

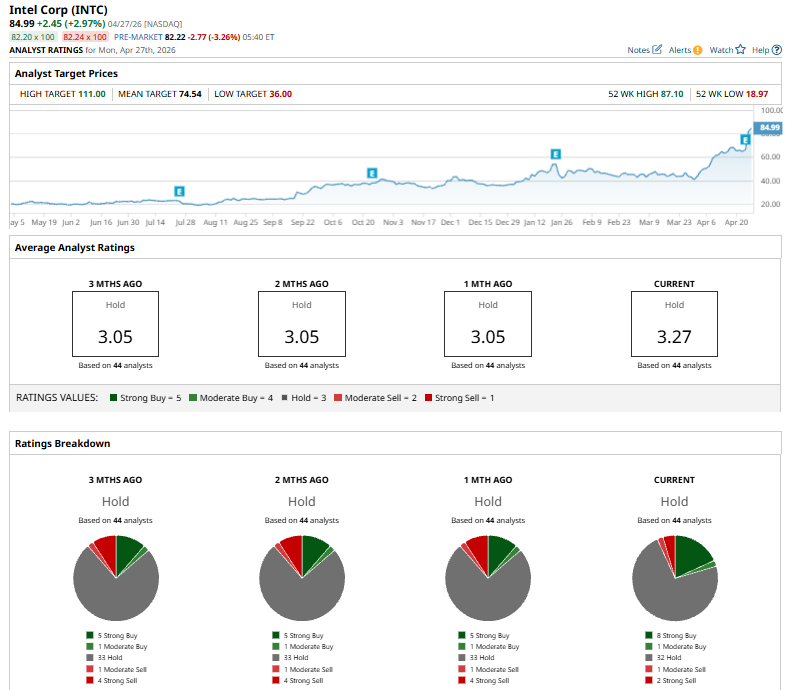

Among the 44 analysts covering INTC stock, the consensus is a “Hold.” That’s based on eight “Strong Buy” ratings, one “Moderate Buy,” 32 “Holds,” one “Moderate Sell,” and two “Strong Sells.”

www.barchart.com

www.barchart.com On Apr. 27, Barclays analyst Tom O’Malley reiterated an “Equal-Weight” rating on Intel and raised the price target to $65 from $45.

While the stock currently trades above its mean price target of $75.54, the Street-high price target of $111 suggests an ambitious upside potential of 30.6%.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

As SOX Crosses 10,000 for the First Time, Atomera and GCT Semiconductor Are the 2 Top-Rated Chip Stocks to Buy Now AMD Earnings Bull Put Spread has a High Probability of Success Nasdaq Futures Plunge as AI Concerns Resurface, FOMC Meeting and Earnings in Focus Newmont Is Golden: Why Record Gold Prices Make It a Must-Buy Dividend Stock Now